Aviva Investors’ David Cumming on the reasons to be cheerful about the UK’s underperforming equity stocks

WELCOME

In July 2018, Aviva Investors recruited a team of equity fund managers from Standard Life Aberdeen (SLA) as it opened an Edinburgh office for the firm. In this guide, David Cumming, a former SLA Head of Equities and now Aviva Investors’ Chief Investment Officer for Equities, discusses the group’s repositioned UK equity range, what sectors look attractive and how they have integrated ‘on trend’ ESG factors in their decision-making process.

No one could accuse David Cumming of failing to put his money where his mouth is. While UK equities took a pummelling from investors in 2018, he remains positive about the market in which he has a personal as well as a professional stake.

THE INTERVIEW

Keeping the faith: A bet on the UK bounceback

David Cumming, Chief Investment Officer

After leaving his previous role at SLA late last year, he says, “I sort of liquidated and put money back in the markets – not quite at the bottom, sadly. “So I’m quite comfortable that the UK market looks cheap and although there are risks, the risk-reward ratio is positive.” He cites supportive figures: current valuations, at around 11.5 P/E, are lower than the long-term average of 13 to 13.5, and certainly attractively cheap in comparison to bonds. Yields, meanwhile, stand relatively high at 4.7%. An upbeat perspective might be expected from a man who now leads an equity team benefiting from an injection of 15 additional fund managers, with a few more hires pending. But Cumming is not in denial about recent performance, which he acknowledges has been “a terrible market”, particularly for large cap stocks. Nor is he discounting the uncertainty over the nature of the UK’s imminent departure from the EU. Rather, he foresees a likely ‘Brexit bounce’ if the negotiations finally result in a deal that averts a disorderly exit. The issue has been the main drag on business confidence and on domestic stock performance, Cumming believes, as well as fostering a reluctance among overseas investors to back the UK. “The reason the market has lagged other markets is predominantly Brexit,” he says. “If we get some sort of deal, as opposed to no deal, I think the market will profit quite strongly because we’ve been held down. “So any sensible resolution will in my view be worth at least 500 or 600 points from where we are in the market – and that gets you back to normalisation.” Those low-rated large cap stocks would then see a lift, Cumming reasons. He foresees “a bit of a rebalancing” as the currency rallies, with house builders, domestic retail and leisure stocks all likely to improve as a result.

All this is predicated on politicians’ ultimate ability to side-step the risk of crashing out of the EU. Cumming is in no doubt about the gravity of a different result, which would see business retreating from the UK. “The closer you are to business, the more uncomfortable you are with no-deal as an outcome,” he declares. Even in this scenario, however, Cumming would steer his team to stay cool-headed and find the best advantage. That’s in line with Aviva Investors active investment philosophy, designed to generate portfolios that are dynamic in response to change. In a crisis, he notes, “people lose emotional control, so sometimes you get dislocation that provides opportunities. “You just have to stay flexible. Equities is not one of those markets where you can shut down risk and open it up again. We’re buying companies where you’re going to have to take risk positions.”

Besides Brexit, Cumming identifies two other major macroeconomic influencers. One is the US economy, which he believes is unlikely to slow sharply, despite the market panic at the end of 2018. Indeed, January saw US jobs grow for the 100th consecutive month. The other point of tension is China’s economy and the impact of its trade battle with the US. While he has no firm view on the outcome, Cumming points out that “Trump tends to do deals in the end – that’s what happened with Mexico and Canada.” He believes China still presents some long-term risk, though government measures – including higher public spending and tax cuts for small business – have secured stability for the short term. Back home, the economy may be sluggish, with the Bank of England forecasting growth of 1.2% for 2019 – the slowest in a decade. But Cumming sees no cause for deep concern. “There’s nothing that tells me the UK is going to fall into recession this year,” he concludes. “On that basis, I’m quite bullish about the markets.”

Finding opportunities in a crisis

*Source: Citi, October 2018.

Deal could restore normality

Anxieties from abroad

Aviva Investors' UK Equity Strategies

Introducing the repositioned fund range

FUND SNAPSHOT

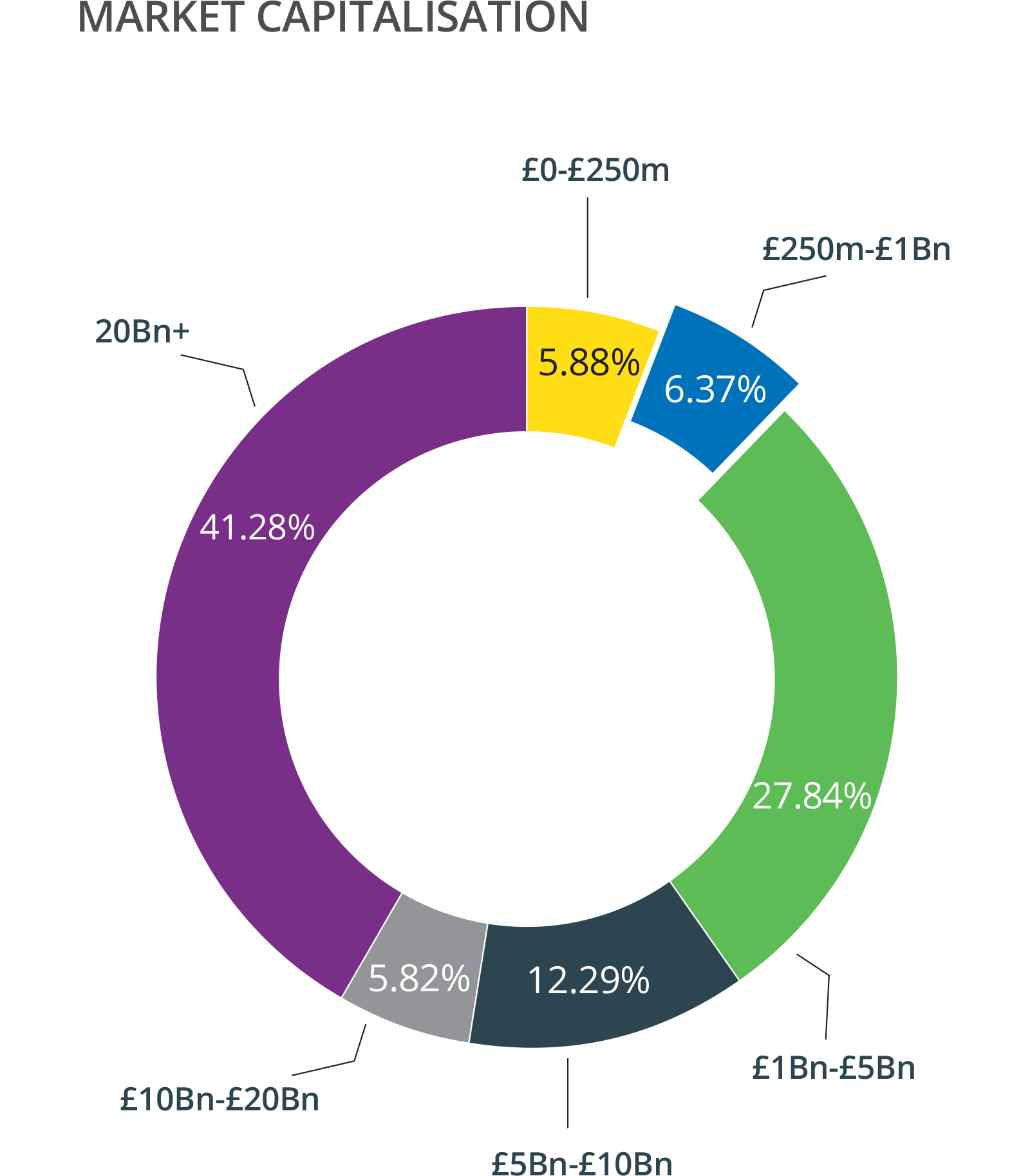

UK Equity Income Fund

Source: Aviva Investors/Aladdin as at 31 December 2018. Basis: Excludes cash & unassigned

Pillars of the investment process

UK Listed Equity Unconstrained Fund

Source: Aviva Investors/Aladdin as at 31 December 2018 Basis: Excludes cash & unassigned

FUND Q&A

"Our competitive advantage is at the micro end because we have good company access and our information flow is strong"

Yes we’ve renamed some of the portfolios and moved them into slightly clearer areas because before there was too much overlap. We’ve also strengthened our key regional teams. What we’re trying to do is ‘institutionalise’ our retail proposition. In other words making sure we have a common investment language, processes, and a clear proposition in terms of philosophy. So we now have an unconstrained fund, a small cap, a small/mid cap, an income fund and a high alpha fund which is benchmark sensitive. I manage the high alpha fund. As other capabilities are brought to bear, we’ll strengthen our products outside the UK as well.

You have recently overhauled your UK equity range. What are the new mandates designed to do?

Yes. When dealing against passive, you’ve got to make sure you’re taking bets. To that end we take the view that the future and the past are different so we believe in a high active share and future-focused approach. You can’t do that with passive ETFs because they’re all correlated to the past. Our competitive advantage is at the micro end because we have good company access and our information flow is strong. As well as being fundamental in approach our other investment style is ‘agnostic’ which means we’re not ‘style neutral’ but neither are we in the ‘always growth, always value’ camp. It depends on where we see the opportunities. One of the other things we’ve done in terms of restructuring our process is that we’re now all hybrid. Everyone covers the big sectors like materials, industrials and financials and we have clear lines of responsibility in each regional team.

Do you have a common investment philosophy across the range?

ESG is important. You’ve got regulation in financials, you’ve got labour issues in retail, you’ve got carbon footprint in oil, you’ve got extraction; there are ESG factors everywhere in the market. Aviva Investors has always had a good reputation at every level of ESG. Being involved in the UN Charter, we sponsored the recent change in terms of how Shell look at their remuneration, which was linked to their carbon footprint and climate change. So we’ve been active at that high level. I think if you do it well and you can integrate it into the investment decision-making process in terms of information flow, then it can improve stock selection.

How do you consider ESG factors as part of your decision-making?

We quite like commodities. Mining stocks such as Rio, BHP and Anglo have done well recently. They have de-geared, they’re more CapEx conscious and I think the market has underestimated the cash flow that’s coming out of these companies. The other area is banks. They’re still trading at a big discount to book, returns are improving and the balance sheets have been sorted out. Most of the regulatory risk is out of the way. Elsewhere? We like some of the consumer discretionaries. There are a lot of stocks in this sector, like Tesco, that just look too cheap. They’re throwing off a lot of cash, growing modestly, and the rating is not that high.

Which sectors look more attractive at the moment?

The key for us is to perform. Clearly the market is difficult but I think if Brexit does go the right way, then a lot of money could come into the UK market that has been sitting on the side-lines. I am confident we will deliver outperformance because we’ve done that historically. From my perspective, we want to win money in retail, we want to win money in institutional and we want Aviva to move from passive to active more, because we’ve got more capabilities there. On the retail side we have good fund managers and a good process. Our brand is being repositioned. So there are a lot of things to aim at. I’d be very disappointed if in the next few years we don’t see over £1 billion flow into these funds.

Do you have a five-year view in terms of what you’d like to achieve with incoming retail flows?

MEET THE TEAM

To learn more about Aviva Investors, please visit avivainvestors.com

Focus is an Incisive Works product. © 2019 Incisive Business Media (IP) Limited

For more information visit http://www.incisiveworks.com

Important information Past performance is not a guide to future performance. Except where stated as otherwise, the source of all information is Aviva Investors as at 28 February 2019. Unless stated otherwise any opinions expressed are those of Aviva Investors. They should not be viewed as indicating any guarantee of return from an investment managed by Aviva Investors nor as advice of any nature. For further information please read the latest Key Investor Information Document and Supplementary Information Document. The Prospectus and the annual and interim reports are also available free of charge from www.avivainvestors.com. Issued by Aviva Investors UK Fund Services Limited, the Authorised Fund Manager. Registered in England No. 1973412. Authorised and regulated by the Financial Conduct Authority. Firm Reference No. 119310. Registered address: St Helen’s, 1 Undershaft, London, EC3P 3DQ. An Aviva company. RA19/0267/01032020

Key Risks The value of an investment and any income from it can go down as well as up. Investors may not get back the original amount invested. Investments in small and mid-sized companies can be volatile and harder to sell than large companies. The Funds use derivatives, these can be complex and highly volatile. Derivatives may not perform as expected meaning the Funds may suffer significant losses. Certain assets held in the Funds could be hard to value or to sell at a desired time or at a price considered to be fair (especially in large quantities), and as a result their prices could be very volatile.

Henry Flockhart Fund Manager Henry manages the Aviva Investors Listed UK Equity Unconstrained strategy. Joined the industry: 2008 Joined Aviva Investors: 2018

Chris Murphy Senior Fund Manager Chris manages Aviva Investors’ UK Equity Income strategies. Joined the industry: 1988 Joined Aviva Investors: 2006

Adam McInally Fund Manager Adam co-manages the Aviva Investors Small and Mid-Cap Fund as well as another segregated mandate. Joined the industry: 2008 Joined Aviva Investors: 2018

Trevor Green Senior Fund Manager Trevor is responsible for the group’s UK institutional funds and the Aviva Investors UK Smaller Companies Fund. Joined the industry: 1990 Joined Aviva Investors: 2011

James Balfour Fund Manager James is co-Fund Manager of our UK Equity Income strategies alongside Chris Murphy. Joined the industry: 2012 Joined Aviva Investors: 2012

Charlotte Meyrick Fund Manager Charlotte co-manages the Aviva Investors Small and Mid-Cap Equity Fund. Joined the industry: 2012 Joined Aviva Investors: 2012

Tom Grant Analyst Tom has lead sector coverage for Diversified Financials and Insurance. He also assists with the day-to-day management of Aviva Investors UK equity funds. Joined the industry: 2015 Joined Aviva Investors: 2015

David Cumming, Chief Investment Officer, Equities David has oversight of the group’s Equities teams. Joined the industry: 1983 Joined Aviva Investors: 2018