Moz Afzal explains how the New Capital Strategic Portfolio UCITS Fund takes a diversified, best ideas approach to multi-asset investing

WELCOME

Moz Afzal, manager of the New Capital Strategic Portfolio UCITS Fund, presents a macro-driven asset allocation portfolio that seeks a target return of Libor +5% per annum with half the volatility of equity markets. Afzal and his co-managers, Sailesh Bhundia and Michalis Rikos, invest across global equities and bonds, commodities, real estate, and hedge funds, aiming to offer consistent risk-adjusted returns across different market conditions. The Fund is designed for clients looking for diversified asset allocation solutions. A well-diversified multi-asset approach, Afzal explains, can smooth returns and reduce volatility over a market cycle.

The benefits of asset allocation have certainly become clearer to many investors over the past ten to 20 years.

THE INTERVIEW

of asset allocation

Harnessing the power

Moz Afzal

CIO and Senior Portfolio Manager, New Capital – EFG Asset Management

Looking ahead

Investment areas

“Global investing gives us a much wider remit of investment types, economic cycles, currencies and valuation ranges. They’re all quite different. So for enhancing risk-adjusted returns, diversification is important. “But we shouldn’t forget that being overly diversified – taking all risk out of the portfolio – also means you take the returns out of the portfolio as well. “What we’ve seen over the last three years is that many multi-asset managers have not been able to make absolute or relative returns because they’ve been fixated on risk control. “Our philosophy has always been to try and make the best risk-adjusted returns in different market conditions.” When it comes to the risk landscape for asset allocation in 2018, what are the main themes for investment managers? According to Afzal, the tightening of interest rates which, together with the tapering (ECB) and unwinding (Federal Reserve) of quantitative easing, is likely to create headwinds for bonds. So central bank actions, in particular, will remain a big focus, he says. “What the central banks are reflecting through the unwinding of quantitative easing and the first few rate hikes is a recognition that they need some ammunition to fight deflation if it re-appears. “We think the Federal Reserve has achieved step one in that respect. And they are now more likely to act in accordance with economic conditions but still in a cautious way. They are not going to raise rates if they feel that inflation is well contained.” He continues: “We have had a bull market over the last eight years but we haven’t seen the greed factors that typically come through in investor attitudes after a bull market. And even though equity markets have seen a prolonged period of performance, people are still buying bonds.” Valuations are high relative to history but the macro environment is remarkably benign for financial markets and valuations should be judged in that context, Afzal says. “We are waiting for all of that monetary stimulus from the central banks to manifest itself into economic growth. “What we at New Capital are trying to do is find value across investment grade bonds in both developed and emerging markets and high yield. “There will always be opportunity. We tend to forget that even in 2008 the opportunity was in government bonds. “So our response in this setting has been to look across the different asset classes and position the portfolio according to the forecasted economic environment. That allows us to provide investors with a solid long-term return.”

Regulatory developments, along with the changes to pension freedoms and new hybrid products across equity, fixed income, and alternatives, have been pivotal in moving the focus for institutional fund management to multi-asset. Indeed, a multi-asset approach can smooth returns and reduce volatility over a market cycle, explains Moz Afzal, CIO and Senior portfolio Manager at New Capital. “From a UK perspective, new regulation stemming from the Retail Distribution Review has been a key driver behind the uptake in multi-asset investing,” he says. “Within the investment community, there is now more focus on costs to implement. In the past institutional managers had a lot of in-house capability, but the industry is recognising that for small and mid-size funds, having your own in-house team is quite expensive. And as a result the trend towards multi-asset investing has accelerated.” Afzal runs New Capital’s Strategic Portfolio UCITS Fund, which launched in December 2014 and encapsulates the group’s macro-driven asset allocation process. The Fund invests in global equities and bonds, commodities, real estate, and hedge funds, aiming to offer consistent risk-adjusted returns across different market conditions. New Capital’s approach to portfolio construction is rooted in a long-term strategic and macro view. Afzal and his co-managers, Sailesh Bhundia and Michalis Rikos, will look at the key factors of growth, inflation and interest rates but tactical tilts are also made – for example around Brexit or geopolitical risks related to North Korea and US trade relations. “The interest rate cycle is the dominant component of our portfolio construction process,” Afzal says. “And that is really driven by interest rate expectation, inflation expectation and how monetary policy moves or shifts around that.” He adds that the team blends the best ideas from New Capital’s teams from around the world to deliver inflation plus returns for investors, but with an eye on volatility. This allows them to capture individual potentially high-return investments sufficiently diversified to reduce the overall risk of the portfolio.

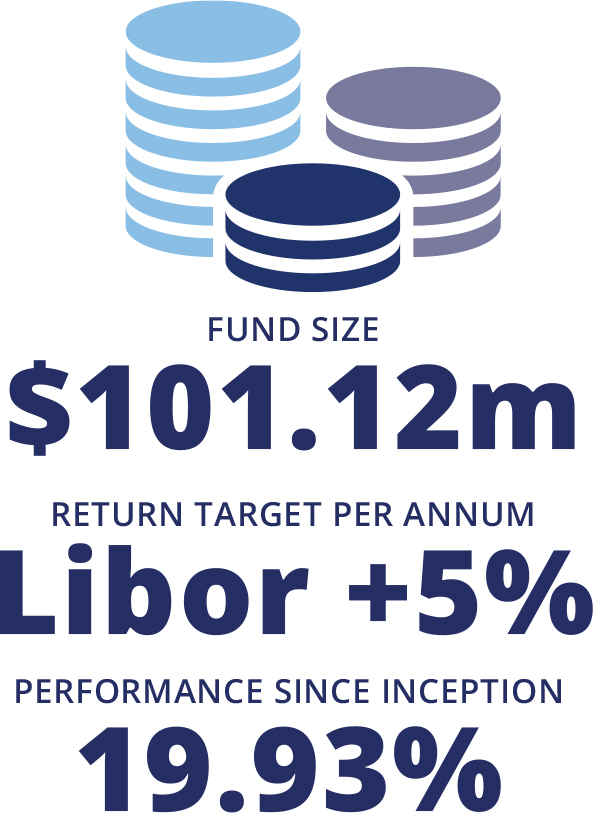

Fund Snapshot: New Capital Strategic Portfolio UCITS Fund

Source: FE. As at 31 December 2017. Past performance is no indicator of future performance. The manager track record is an equal weighted blended portfolio of all of the funds Moz Afzal has managed over this time period. The peer group composite is an equal weighted average of every manager’s track record with a fund in the same sector/asset class over that same time period.

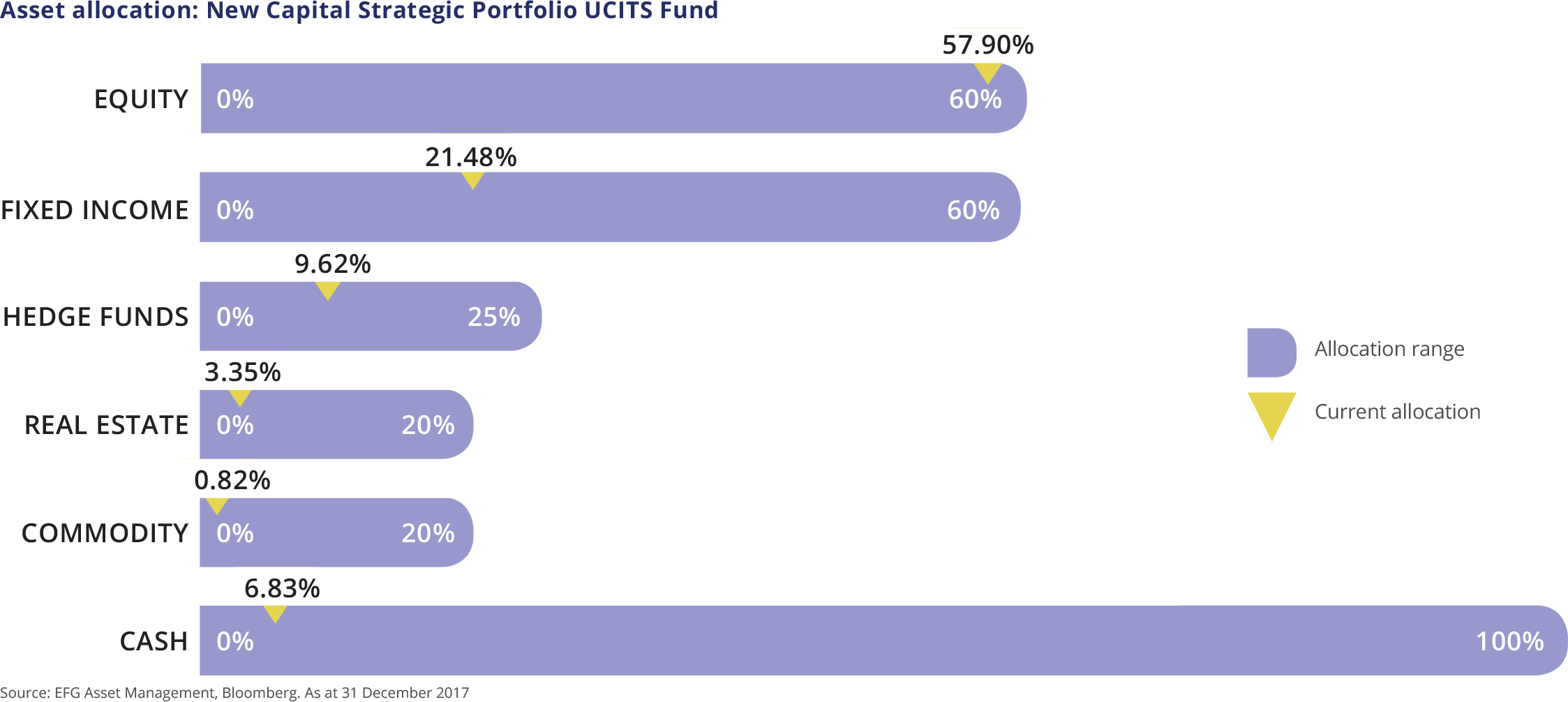

Source: EFG Asset Management, Bloomberg. As at 31 December 2017

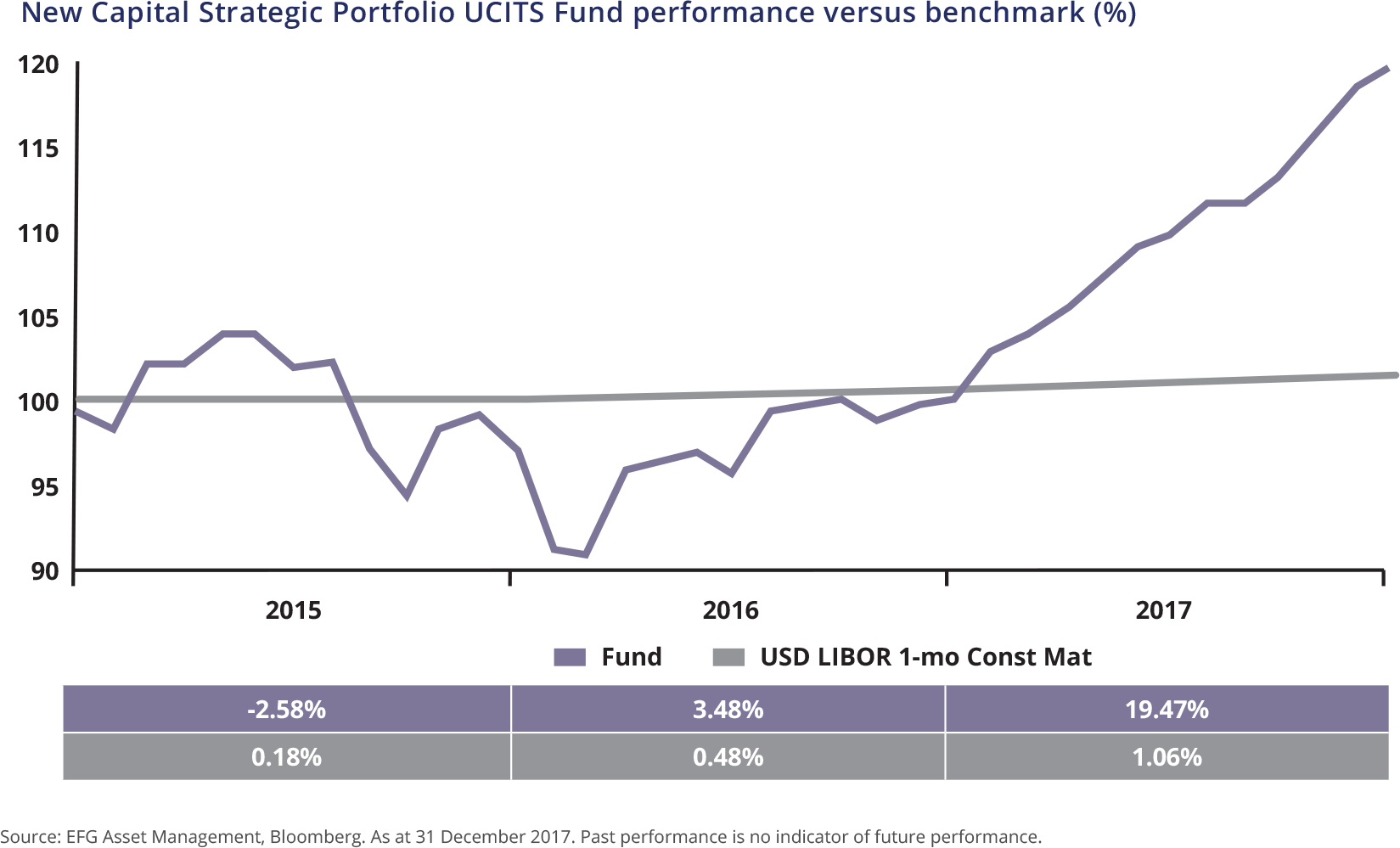

Source: EFG Asset Management, Bloomberg. As at 31 December 2017. Past performance is no indicator of future performance.

New Capital Strategic Portfolio UCITS Fund performance versus benchmark (%)

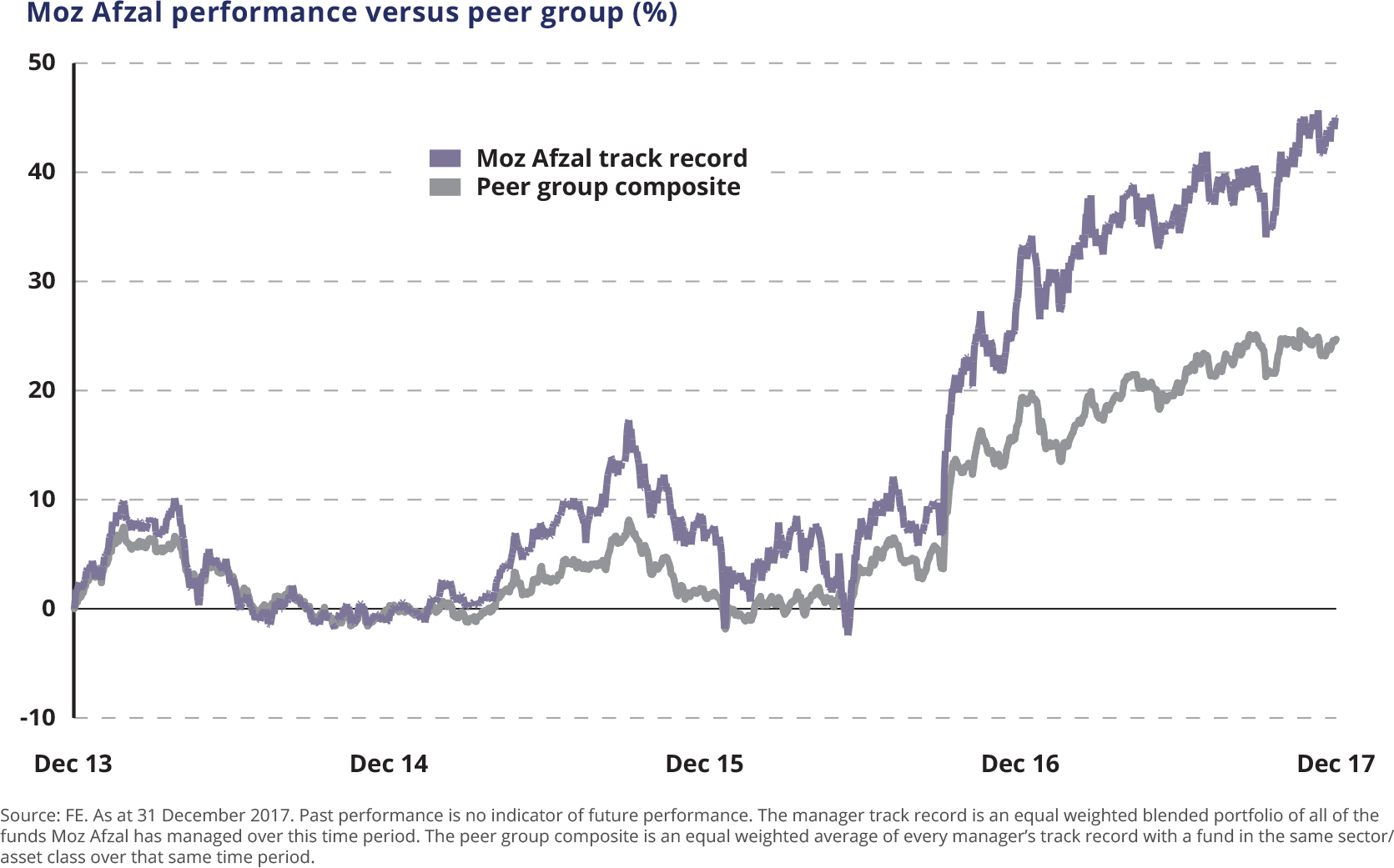

Moz Afzal performance versus peer group (%)

2017 proved to be a successful year for the Fund. The investment team produced positive returns across all four quarters and outperformed their absolute return cash benchmark. For the year the Fund returned 19.5%. This compared to a return for the MSCI ACWI in USD of 23%, meaning the Fund captured over 80% of world equity performance. Asset allocation on the portfolio reflects New Capital’s strategic macro and market views, with various tactical positions also in place.

Moz Afzal has consistently maintained an above average track record when running the New Capital Strategic Portfolio UCITS Fund in both rising and falling markets over the past three years. New Capital believes investors are best served by a macro-driven asset allocation process and Afzal’s high conviction strategy strongly reflects this with a cumulative performance of 19.93% since the fund’s inception. At a fund manager level, this hands-on active investing approach has materialised in Afzal returning 45% at an individual fund manager level over the past four years. This is significantly ahead of his peer group composite average of 25%.

Asset allocation: New Capital Strategic Portfolio UCITS Fund

Valuation is key to what we do. ESG considerations are integrated into the investment process and diversification across sectors and regions is extremely important to us as well.

What is the fund designed to do?

The New Capital Strategic Portfolio UCITS Fund launched in December 2014 and encapsulates our macro-driven asset allocation process as well as bottom-up input from the New Capital global research teams. The Fund is designed to offer a diversified asset allocation solution and we do this by investing across global equities and bonds, commodities, real estate, and hedge funds. We believe asset allocation is integral both to portfolio construction and overall investment performance. A well-diversified multi-asset approach can smooth returns and reduce volatility over a market cycle.Our long-term goal over an economic cycle is to achieve USD LIBOR 1-mo Constant Maturity plus 5%. To meet this return objective we have to take some risk. Therefore we have a reference benchmark that is 40% in bonds, 45% in equities and 15% in alternatives and cash.

Which instruments are displaying the best opportunities at the moment?

The companies that we have been focusing on, certainly over the last 12 to 18 months and going forward, have been very much around artificial intelligence: companies like Nvidia who make chips at the centre of artificial intelligence enablement. We’ve also invested in Facebook, Amazon and Netflix within the disruption of television and traditional advertising. We also like Umicore who are focussed on cobalt which is a key ingredient for batteries. Then there’s Glencore who provide the copper and commodities that broadly go into electric vehicles. So within each of the disruptive trends, we’ve identified those companies and been able to build positions and monetise the themes.

What key risk parameters do you identify and how are you mitigating them?

What we’re looking for is volatility in the 7-11% range so we’re definitely in the medium risk category. Equities would typically have 15-17% over a cycle in terms of volatility; fixed income is more in the range of 3-5%. Clearly over the last 12 to 18 months, volatility has been a lot lower than our target range and as such our volatility has been closer to 4-5%. But I would say these conditions are relatively unusual. The overall market volatility from equities to bonds to commodities and even hedge funds has been relatively low.

What is your level of exposure to certain investment themes and regions – and why?

One of the key themes we’ve been focusing on is technology disruption. We’ve seen this happen in the industrial space for some time but over the next five to ten years we think the services sector will be disrupted in a similar way. This theme will be key for any portfolio construction going forward. The other theme we’ve been looking at is electric vehicles and how they are impacting the commodities industry and the traditional manufacturing model for cars. It’s a game changer when it comes to manufacturing. What’s more, the historical method of selling cars through dealerships and the financing model for electric vehicles also looks set to be disrupted. We think direct to consumer is another key theme when it comes to electric vehicles and we’re starting to see some changes there, led by Tesla who have a stronger affinity with its audience than say BMW or Audi or the other traditional car companies. Ultimately, our key interest is in disruption as a broad theme: from electric vehicles to block chain to how we consume media and digital products.

FUND Q&A

"The other theme we’ve been looking at is electric vehicles and how they are impacting the commodities industry and the traditional manufacturing model for cars"

For more information visit http://www.incisiveworks.com

Sailesh is a Senior Director within the Portfolio Management team at EFGAM, and is a member of the EFGAM Asset Allocation Committee. Sailesh has 18 years of investment experience and joined EFGAM in 2000. He previously worked at Credit Suisse First Boston where he held various positions within the international and emerging markets trading division. Sailesh holds a BSc Honours in Economics from City University and a MA in Economics from Leicester University. He is a holder of the Chartered FCSI and a member of the Chartered Institute for Securities and Investment.

Sailesh Bhundia, Senior Director – Portfolio Management

Michalis joined EFGAM in 2010 and is a Portfolio Manager with a focus on multi-asset discretionary and managed advisory portfolios. Michalis has previously worked in the Hedge Fund industry as an Assistant Portfolio Manager. He has a BA degree in Banking and Financial Management from University of Piraeus and a MSc Honours degree in Finance and Accounting from Athens University of Economics and Business. He is also a holder of the Investment Management Certificate (IMC) and a CFA charterholder.

Michalis Rikos, Portfolio Manager

Moz is lead manager on the New Capital Strategic Portfolio UCITS Fund. He has also headed up the original Cayman-domiciled product since its launch in 2009. He is chairman of the EFGAM Asset Allocation Committee and has overall responsibility for our investment process. He joined EFG Private Bank in 1994 and was appointed director and chief investment officer in March 2003, and as director of asset management in January 2000. He previously ran fixed income funds and multi-asset portfolios, and has held supervisory roles in multimanager long-only and hedge fund investments. Prior to joining EFG, he was an investment analyst in the Macroeconomic Policy Division at HM Treasury.

Moz Afzal, CIO and Senior Portfolio Manager

CONTACT US

Find out more at www.newcapitalfunds.com

Focus is an Incisive Media product. © 2018 Incisive Business Media (IP) Limited

Issued by EFG Asset Management (UK) Limited which is authorised and regulated by the Financial Conduct Authority (FCA Registration No. 536771). Registered No: 7389746. Registered address: Leconfield House, Curzon Street, London W1J 5JB. Telephone: +44 (0)20 7491 9111. This document is not intended as a recommendation to buy, sell or take any other action in relation to any security mentioned herein. To the extent that this document contains non-independent research, this document should be considered a marketing communication. Such research has not been prepared in accordance with legal requirements designed to promote the independence of investment research and it is not subject to any prohibition on dealing ahead of the dissemination of investment research. This document does not constitute and shall not be construed as a prospectus, public offering or placement of, nor a recommendation to buy, sell, hold or solicit, any investment, security, other financial instrument or other product or service. It is not intended to be a final representation of the terms and conditions of any product or service. The investments mentioned in this document may not be suitable for all recipients and you should seek professional advice if you are in doubt. Clients should obtain legal/taxation advice suitable to their particular circumstances. This document may not be reproduced or disclosed (in whole or in part) to any other person without our prior written permission. Although information in this document has been obtained from sources believed to be reliable, EFGAM does not represent or warrant its accuracy, and such information may be incomplete or condensed. All estimates and opinions in this document constitute our judgment as of the date of the document and may be subject to change without notice. EFGAM will not be responsible for the consequences of reliance upon any opinion or statement contained herein, and expressly disclaims any liability, including incidental or consequential damages, arising from any errors or omissions. Performance results shown are net of applicable fees and expenses. The value of investments and the income derived from them can fall as well as rise, and you may not get back the amount originally invested. Past performance is no indicator of future performance. Investment products may be subject to investment risks, involving but not limited to, currency exchange and market risks, fluctuations in value, liquidity risk and, where applicable, possible loss of principal invested. Any information quoted relating to the New Capital UCITS Fund plc is merely a brief summary of key aspects of the Fund. More complete information on the fund can be found in the prospectus, the simplified prospectus or key investor information document, and the most recent audited annual report and the most recent semi-annual report. These documents constitute the sole binding basis for the purchase of fund units. Copies of these documents are available free of charge in the United Kingdom at EFG Asset Management (UK) Limited (“EFGAM”), Leconfield House, Curzon Street, London W1J 5JB, United Kingdom. Copies of these documents are available free of charge in Germany at the offices of the German information agent, HSBC Trinkaus & Burkhardt AG, Königsallee 21/23, 40212 Düsseldorf, Germany. Copies of these documents are available free of charge in France from the French centralizing agent, Societe Generale, 29, boulevard Haussmann – 75009 Paris, France. Copies of these documents are available free of charge from the Swiss Representative: CACEIS (Switzerland) SA, Route de Signy 35, CH-1260 Nyon, Switzerland. Paying Agent: EFG Bank SA. 24 Quai du Seujet, CH-1211, Geneva 2, Switzerland. This document is not intended as a recommendation to buy, sell or take any other action in relation to any security mentioned herein. To the extent that this document contains non-independent research, this document should be considered a marketing communication. Such research has not been prepared in accordance with legal requirements designed to promote the independence of investment research and it is not subject to any prohibition on dealing ahead of the dissemination of investment research. Copies of these documents are available free of charge in Luxembourg at the offices of the Luxembourg paying agent, HSBC Securities Services (Luxembourg) S.A., 16 boulevard d’Avranches, L-1160 Luxembourg, R.C.S. Luxembourg, B28531.