Titanium in 2025: Normalise before take-off

Titanium metal is a key critical raw material used in the aerospace and defence, industrial and medical markets. Geopolitical fractures, emerging supply markets and downstream supply chain challenges have forced a reassessment of the fundamentals in the last two years. An impending deficit of aerospace-approved titanium sponge is set against a burgeoning Chinese market; the ramp-up in aerospace manufacturing has yet to truly take off, skewing scrap market dynamics, and near to medium term growth prospects; and leaving inventory overhang in various parts of the value chain.

Argus Interactive Insights

2

1

4 Market Drivers

2025 will be a year to patch up and resolve various issues before an inflection point in 2026, as the aerospace market addresses unresolved bottlenecks, tests and potentially qualifies Chinese titanium sponge, and normalises inventories.

Airframer build rates

Sponge: impending deficit and Chinese oversupply

3

US ingot capacity expansions

4

Scrap generation versus consumption: when will the overhang clear?

Airbus and Boeing build rates and delivery targets have been subject to revisions, pushouts, and certain cases of surpassing. With build rate targets now stretching out to 2028 , the supply chain is gearing up for a ramp-up that will see widebody rates more than double as airframers vie to meet demand for international travel. But there is much work to be done to stabilise the supply chain before a true ramp can occur. Airbus and Boeing both hit their production targets (albeit a revised target on Boeing’s part) in 2023, but operations in 2024 were hit by parts shortages, federal interventions, labour disputes, acquisitions and groundings. As a counterreaction, the resulting drop in output at certain supply tiers has led to an accumulation of inventories at some manufacturers. And so the tail wags the dog. Shortages in 2024 included engines, and more specifically high-pressure turbine blades, structural castings, heat exchangers, cabin equipment and aerostructures. Delays on aircraft deliveries to airlines have forced operators to run their existing fleets for longer, driving demand for maintenance, repair and overhaul (MRO) services. This extends the strain on parts suppliers who have to manage their new build and aftermarket commitments. Recent OEM comms indicate that some of these bottlenecks will be partially if not wholly resolved in the coming year. But the damage that the Covid-19 pandemic and geopolitical fractures since 2022 have exacted on the supply chain cannot be understated, and it has remained under duress to deliver on the ramp-up ever since.

Click to see more

#1

Story

Data

Facts

Airbus, Boeing production rate targets

Boeing deliveries

Airbus deliveries

Buy-to-fly ratio from titanium ingot to finished part is upward of 6:1 through conventional forging and machining.

Titanium demand for aerospace engine applications to grow at 10.5pc CAGR over next 5 years: ATI.

Grade 5 titanium (6Al 4V) is the workhorse of the aerospace industry.

Widebody aircraft – 777X, 787, A350 – are up to 20pc by weight.

Narrowbody aircraft – A320neo, 737MAX – contain up to 10pc titanium by weight

Argus Non-Ferrous Markets service

Learn more

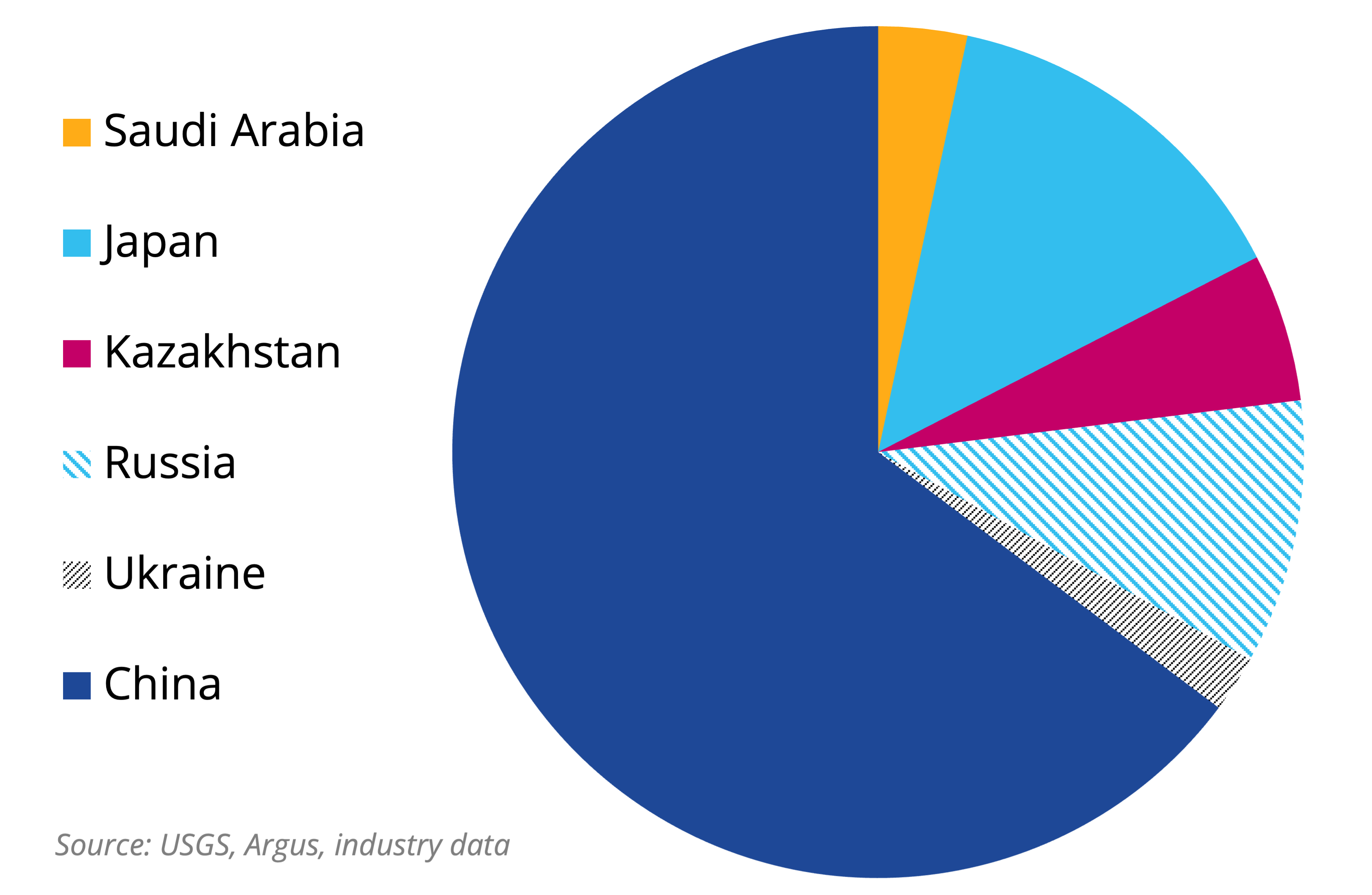

The titanium sponge market is simultaneously forecast to enter a deficit in the next four years, according to Toho Titanium, and facing vast oversupply from a burgeoning Chinese market. While contradictory, both scenarios are true. Titanium utilised in aerospace parts must be sourced from qualified producers, which currently includes Toho Titanium and Osaka Titanium in Japan, Ust-Kamenogorsk Titanium and Magnesium Plant (UKTMP) in Kazakhstan, and Advanced Metal Industries Cluster and Toho Titanium (ATTM) in Saudi Arabia. Sponge demand from aerospace and defence applications in 2024 stands at approximately 79,000t, and is expected to increase to around 90,000t by 2028 and 102,000t by 2031, Toho data show. Toho is set to bring online an additional 3,000t by January 2026, with a further facility under consideration, and Osaka an additional 10,000t by March 2028. No new expansions are slated for ATTM or UKTMP. The required capital investment to offset demand increases is vast and as such Toho anticipates that the sponge market (excluding China) will tip into a deficit in 2028. This is also contingent on continued offtake from Russia. China's burgeoning titanium market is significantly oversupplied relative to domestic requirements, and this surplus is expected to grow on continued capacity expansions, meaning it is predisposed to export. But Chinese sponge is not yet qualified for aerospace applications. Argus understands that certain US and EU consumers of aerospace-grade sponge are currently testing Chinese sponge. If Chinese material receives the relevant qualifications, the question remains as to the long-term viability of a trade partnership with China that may be subject to further tariff hikes under the tenure of President Trump.

#2

Titanium trade flow map

Current capacity

Argus launched Chinese titanium sponge export prices in 1Q-2025.

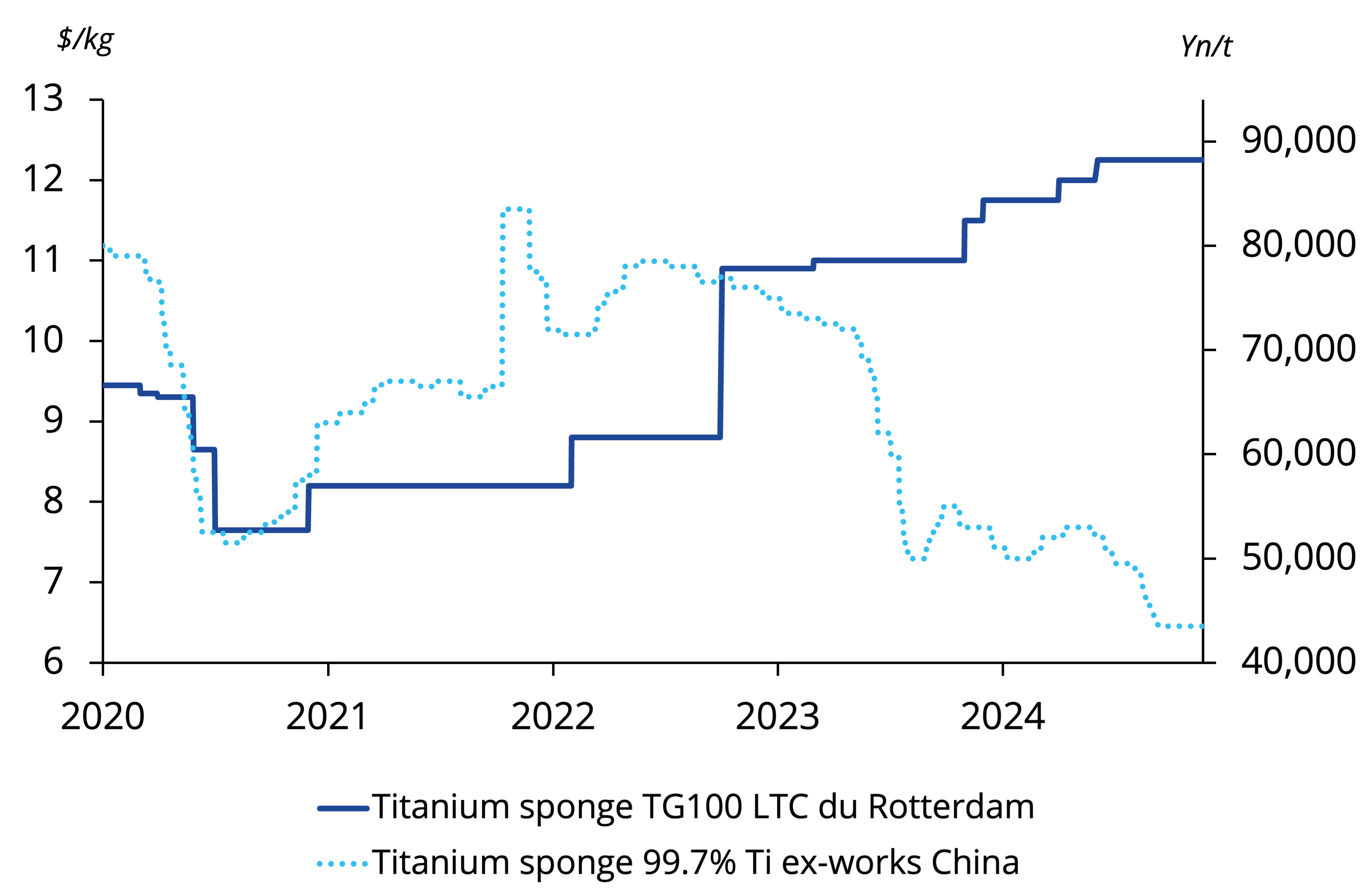

Chinese 99.7% titanium sponge prices are at their lowest level since 2016, while TG100 long-term contract prices are at their highest since 2012.

China produced 218,000t of titanium sponge in 2023, more than double the nameplate capacity of Japan, Kazakhstan and Saudi Arabia combined.

Aerospace qualifications can take up to 3 years for standard-quality sponge, and 5+ years for premium-quality rotor-grade sponge.

Projected capacity

China capacity

Titanium sponge price divergence

The start of the war in Ukraine in 2022 intensified a need for western-sourced titanium for both commercial aerospace and defence applications, prompting three of four US titanium mills to plan capacity expansions within their melting operations. Titanium mills are working to fill the void left by Russian titanium producer VSMPO-AVISMA's departure from US supply chains but have faced headwinds induced by downstream manufacturing challenges. Forecasts for titanium demand set at the beginning of 2024 broadly failed to materialize after production missteps and a labour strike at Boeing reduced certain suppliers’ ingot requirements, bringing down prices for the intermediate product and freeing up furnace capacity that the mills have sought to fill. Titanium Metal (TIMET) expects to commence its new plant in Ravenswood, West Virginia, in the summer, bringing online seven vacuum arc remelt (VAR) furnaces and one electron beam (EB) furnace. The company estimates that the project will add 33mn lbs (14,968t) of ingot production annually in its first phase. ATI plans to finish product qualifications for its new EB and VAR furnaces at its Richland, Washington, site next year after targeting first melt in the fourth quarter of 2024. The additional capacity comes after ATI restarted three furnaces and added one more in Albany, Oregon at the end of 2023. The two moves combined should boost ATI’s melting capacity by 80pc above 2022 levels. Perryman Group is ramping up its new EB furnace, as part of a wider expansion that adds VAR capabilities, at its melting facility in Coal Center, Pennsylvania. This should boost the mill’s production capacity by 16mn lb/yr to 42mn lb/yr. French ingot producer EcoTitanium is set to bring online a new VAR furnace in the first quarter of 2025.

US ingot melting expansions

#3

US ingot production map

Scrap accounts for around 2/3 of the raw material utilised in ingot production, with sponge representing the balance, although this can vary on customer specifications and feedstock costs.

Large scrap solids, such as bulk weldable and feedstock, are preferred for use in a VAR furnace, while turnings can be utilised in EB melting.

Titanium ingots are forged into semi-finished products — such as billets and slabs — before those are processed via rolling and further machined into specific components.

Ample supply of titanium scrap relative to demand in the US has soured expectations for near term price recovery, with consumption set to lag domestic generation and imports in the first half of 2025. That gap could narrow by the middle of next year when titanium melters’ capacity expansions are either completed or come online, which could lead to a temporary run on scrap as consumers compete for the same scrap units to feed new furnaces. A meaningful uptick in consumption demand would help deplete domestic inventories of scrap, as domestic generation could fall behind the curve in the short term owing to longer lead times on progressing milled products into machine shops. Still, any significant impact on scrap from TIMET’s Ravenswood startup would potentially not be felt until 2026 because of product qualification timelines. Whether Boeing returns to normalised build rates for its main narrowbody and widebody aircraft programs will also determine when some of the supply overhang should clear. The aerospace industry anticipates that the airframer will recover from lost production and parts shortages in 2025, which would benefit titanium melters’ order books and scrap merchants’ operations. Imports of titanium scrap increased annually from 2021-2023 and were set to rise again in 2024, further bolstering stockpiles on the ground. Shipments reached 23,580t in January-October 2024, compared to 22,446t in the same period a year earlier. But full-year volumes have yet to recover from pre-pandemic levels, which peaked in 2019 at 29,928t.

#4

US vac-scrap price chart

Argus plans to launch 6-4 feedstock scrap price in 2025.

Parts manufacturing accounts for nearly half of all scrap generation, with the remainder originating from titanium mills’ internal production, followed by end-of-life scrap.

US titanium scrap imports primarily consist of aerospace or commercially pure grades, while exports mainly represent ferro-titanium quality scrap.

Titanium scrap forms include turnings (sometimes referred to as chips), clips (sometimes referred to as cobbles), feedstock and bulk weldable, and are differentiated by size.

The Argus Non-Ferrous Markets service is your trusted source for comprehensive daily non-ferrous market intelligence covering base metals, ferroalloys, rare earths, high temp metals, technology metals, alloys and light metals. The service includes titanium price assessments representative of the various stages of titanium production from sponge to scrap in markets across Europe, North America and Asia-Pacific, to ensure you have the last insight into this rapidly evolving market. Aerospace OEM's, Tier 1 suppliers, recyclers and titanium producers around the world use our indexation-standard assessments to manage price risk in long-term contracts, spot market transactions and cost modeling.

Argus Non-Ferrous Markets

Argus plan to launch 6-4 feedstock scrap price in 2025.