Sales, profits and orders/new business continue to shrink

Business performance weakened in the third quarter as all three indicators deteriorated, with profits taking the biggest hit.

Net balances sank deeper into negative territory. This is the difference between the share of firms with an increase and those with a decrease in an indicator, compared to the year-ago period. A positive net balance suggests expansion, and a negative one, contraction.

Sales Net Balance

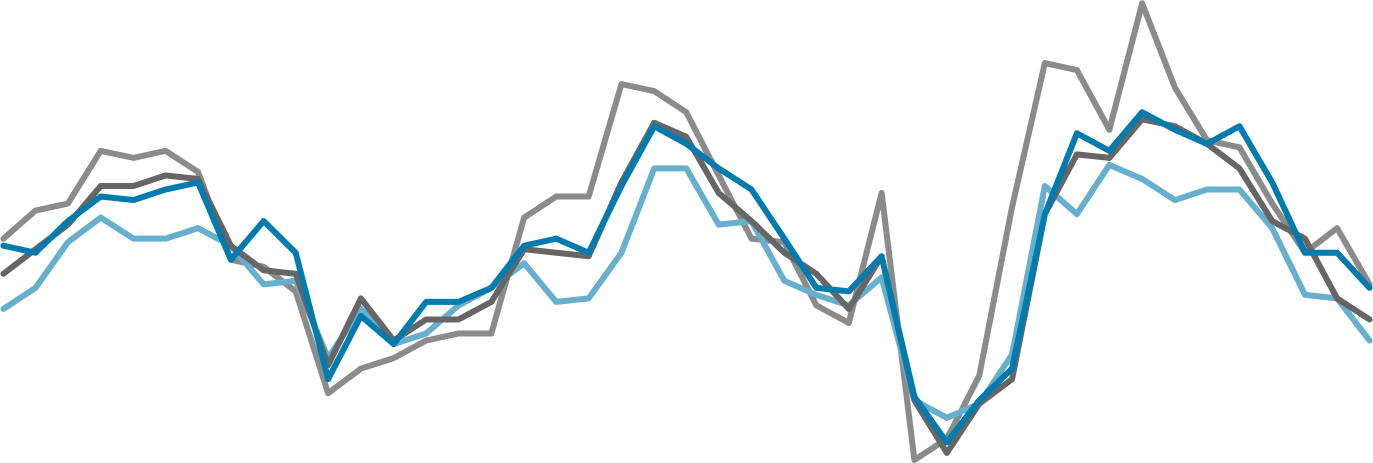

The net balance for sales slipped 10 points to minus 35 per cent, marking the fourth straight quarter in contraction. Sales net balances improved – though remaining negative – for small firms and foreign ones, but worsened for large firms and local ones.

Singapore firms' performance and prospects net balances in Q3

0

-10

-20

-30

-40

-50

Sales

Profits

Orders/New Business

Business prospects

Business performance across the various sectors remains uneven in the third quarter, said UOB senior economist Alvin Liew.

He cautioned that activity will continue to be lacklustre due to weak external demand in an elevated interest rate environment, and low business and consumer confidence in China over property sector stresses.

DBS economist Chua Han Teng noted that the survey findings on business prospects “surprisingly differed” from more positive findings in business expectations surveys for manufacturing and services, by the Economic Development Board (EDB) and Department of Statistics (SingStat) respectively.

“Without much visibility on the granular details of the survey’s data, we suspect the discrepancy could be due to sample size differences,” he said, noting that the BT-SUSS survey polled fewer firms than EDB and SingStat.

The consultants’ full-year growth projections of 0.9 per cent to 1 per cent was in line with the Ministry of Trade and Industry’s (MTI) official forecast range of 0.5 per cent to 1.5 per cent.

It is also close to DBS’ full-year forecast of 0.9 per cent growth.

“While the manufacturing sector remains weak, there are nascent signs that a gradual yet fragile recovery is underway,” said Chua, referring to the Purchasing Managers’ Index, which has improved for two straight months.

In addition, the services sector is likely to remain resilient, notwithstanding weakness in trade-related and financial services due to global headwinds, he said.

“Hospitality-related services have been strong, boosted by post-pandemic reopening tailwinds lifting inbound tourists, with the end-year seasonality also helping,” he added.

UOB was less optimistic, predicting full-year growth of 0.6 per cent year on year.

“Our forecast is consistent with MTI’s assessment for 2023 growth to come in at the ‘lower half’ of the range. Thus we are slightly more downbeat than the projections in the survey,” said Liew.

For Q4, UOB expects growth to be 0.9 per cent year on year – also lower than the consultants’ forecast range.

The construction sector was named the “star performer” in the third quarter, replacing transport and communications, which held the top position for three straight quarters. Firms had the best performance across all four indicators.

Star performer

But construction did not dominate among foreign firms. Among this group, the top spots were taken by firms in transport and communications, as well as financial and business services.

UOB’s Liew said the transport and communications sector’s growth could be normalising after benefiting strongly from reopening tailwinds in earlier quarters: “There has been a convergence to a more sustainable path of growth.”

In contrast, construction growth should remain robust as firms continue to complete backlogged projects delayed due to the Covid-19 pandemic, he said.

“The construction sector might have continued to face resource supply chain issues and labour force challenges during the earlier stages of reopening from Covid-19, but these challenges have subsequently become better managed, allowing the sector to take flight,” said Liew.

A strong pipeline of public and private sector projects could help to raise the prospects of the construction sector, he added.

Separately, firms were asked which country they thought had the best prospects in the next 12 months. Singapore was cited by the biggest share of firms – but its share of votes fell to a quarter, down from a third in the year-ago period.

Indonesia came in second place, while China and Malaysia tied for third place – displacing Vietnam.

Best business prospects

25

20

15

10

5

0

Singapore

Indonesia

China

Share of votes

Most

cited

Second most

cited

Third most

cited

“It is not surprising to see China and Malaysia as the top three countries with the best business prospects next year,” said UOB’s Liew.

“China remains a key production centre as well as an important end-consumer market for many large and small companies,” he said, adding that Malaysia is enjoying good investment flows and its manufacturing sector – especially electronics – is a strong recipient of these investments.

In contrast, Vietnam may have fallen out of favour as its economy has hit a soft patch of growth in recent quarters due to its reliance on external demand, particularly in manufacturing, noted Liew. And unlike China and Malaysia, its manufacturing activity is not as diversified.

Nevertheless, Liew believes the waning enthusiasm for Vietnam is only temporary: “Investors will focus on the country once again, once some of these challenges are resolved or better managed.”

Among foreign firms, China and Indonesia tied for first place, with 15 per cent of firms citing each as having the best prospects. The United Arab Emirates and the US came in joint second place.

By sector, Singapore was cited as having the best prospects for construction and financial and business services. Other sectors named Malaysia, Indonesia and the US as having the best prospects.

Best business prospects among foreign firms

15

10

5

0

China

Indonesia

UAE (Dubai)

US

Among foreign firms, China and Indonesia were the most-cited countries with the best business prospects in the next 12 months

SINGAPORE firms’ pessimism has worsened as businesses reported weaker performance compared to a quarter ago, the latest Business Times-Singapore University of Social Sciences (BT-SUSS) Business Climate Survey has found.

Opportunities abroad

Profits Net Balance

The profits net balance fell 12 points to minus 50 per cent. Profit contraction improved for small firms but worsened for all other groups.

Orders/New Business Net Balance

The net balance for orders or new business sank six points to minus 44 per cent. Large firms took the biggest hit, declining 10 points to minus 46 per cent.

Business Prospects Net Balance

Overall, firms have grown more pessimistic over business prospects for the next six months. The net balance for business prospects tumbled 16 points to minus 34 per cent in the third quarter.

Weak performance

60

40

20

0

-20

-40

2013

-60

-80

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

Sales

Profits

Orders/News Business

Business Prospects

Survey consultants' Singapore growth outlook

1.8% - 2%

0.9% - 1%

PROJECTED Q4

GDP GROWTH

Best business prospects by sector

Source: BT-SUSS Business Climate Survey

BTVisual: Chaytanya Bandishte, Charmaine Martin

PROJECTED 2023

FULL-YEAR GDP GROWTH

-100

— 34%

— 35%

— 44%

— 50%

Singapore was the most-cited country with the best prospects in the next 12 months

Malaysia

Share of votes

Darkened outlook