SINK OR SWIM

fishing for yIEld

THERE ARE FEWER OPPORTUNITIES THESE DAYS, BUT INCOME IS THERE IF YOU LOOK IN THE RIGHT PLACES

a great catch

flexible strategies are helping to exploit inefficiencies in the credit markets

THE MIGHTY STREAM

FocusING on sustainability can help investors TO build more resilient bond portfolios

It’s a new decade but the problem is an old one. Yields are now at, or close to, record lows in many markets, and income-oriented investments offer fewer opportunities than they did a year ago. Yet high-yielding equities, preferred securities and emerging market debt, among others, are providing a useful vehicle for investors with sufficiently long investment horizons. The dilemma for income-seeking investors remains: move up the risk scale and try to achieve more yield, or reassess their yield expectations? In many cases, absolute return strategies have stepped in to provide some acceptable answers. We break down some flexible investment tactics being used to benefit investors. Finally, evidence is building that a focus on sustainability can help investors build more resilient bond portfolios. Indeed, the green bond market has grown dramatically to hit a new record in 2019, with $255bn issued, up 49% on the previous year. This year will be a feisty one. And the various layers of uncertainty – from political risk to credit risk – means that income investors have plenty to think about.

HOME

fishing for yield in a new decade

After a broad global rally in stocks and bonds, income-oriented investments offer fewer opportunities than they did a year ago, but there are still places to look for yield

Global fixed income and equity markets delivered stellar returns in 2019, following a tough end to 2018. Most broad-based US fixed income markets made mid- to high-single-digit returns, while corporate and emerging market debt notched up low- to mid-teen gains. Equity markets also rallied sharply with US stocks, up 20-30%. ‘Three 25-basis-point policy rate cuts by the Federal Reserve during the second half of 2019, a reversal on the Fed’s balance sheet policy, perceived progress on the US-Mexico-Canada agreement, improved prospects for an orderly Brexit and, eventually, the prospect of de-escalation of the trade war with China all served to embolden investors and improve risk sentiment through the final months of the year,’ said Peter Palfrey, co-manager of the Loomis Sayles Core Plus Bond fund.

‘Now with equity markets hovering at or near all-time highs and with multiples already reflecting a lot of good news, equity valuations appear to some to be quite full. Similarly, with the tailwind of easier Fed monetary policy now likely behind us, at least for the foreseeable future, and with credit spreads at or near cycle tights in corporate bond markets, a repeat of the strong returns investors enjoyed last year appears far less likely.’ For Yoram Lustig, head of multi-asset solutions for EMEA at T Rowe Price, income-seeking investors are being forced to navigate unsteady terrain. ‘After last decade’s unprecedented drop in bond yields, income has become scarcer,’ he said. ‘Investors seeking a stable income face a choice: they can regularly sell investments to generate cash flows, although it does not fit all investors for practical or behavioral reasons; they can compromise on the quality of their holdings, therefore increasing risks; or they can tap illiquid investments – such as types of property and infrastructure – although it could augment complexity and costs.’ Thankfully, income opportunities remain in traditional asset classes. Looking over a one- to three-year timeframe, here are six of the best:

JENNIFER HILL

1. HIGH-YIELDING EQUITIES

Dividends from equities around the world remain a good source of income. The MSCI AC World High Dividend Yield index yields 3.9% – very competitive relative to developed market government bonds. ‘And unlike bond coupons, dividends have the potential to grow,’ said Kera Van Valen, managing director of Epoch Investment Partners. Lustig suggests opting for large and liquid company shares in corporations that are likely to remain in business for the long term and keep returning cash to shareholders by way of regular dividends. ‘While the stock market is volatile during times of stressful downward periods, investors with sufficiently long investment horizon have time to recoup losses,’ he said. ‘For investors with appropriate risk tolerance and patience, equities could be a transparent, liquid income source, negating the need to seek income in illiquid, complex and expensive avenues.’

2. MASTER LIMITED PARTNERSHIPS

Master limited partnerships (MLPs) are an equity income asset class that is often overlooked by investors, perhaps because it is not well covered or understood, according to Max Gokhman, head of asset allocation at Pacific Life Fund Advisors. ‘With their preferential tax treatment, equity liquidity and stable dividend yields in the high-single digits, MLPs are a requisite part of any diversified income portfolio,’ he said. ‘More recently, MLPs have undergone a number of prudent changes that bolster their attractiveness, made evident by increased mergers and acquisitions in the sector. MLPs have simplified their capital structures and become increasingly self-funded, with capital expenditures often covered by cash flows, which themselves have been growing. ‘This in turn has allowed MLPs to prudently reduce their debt loads, making them more resilient for the next economic downturn, even as many have been able to increase income distributions to investors.’

3. PREFERRED SECURITIES

Brian Cordes, head of portfolio specialists at Cohen & Steers, rates the ‘unique income opportunity’ in preferred securities. Typically issued by high-quality issuers, such as Bank of America, Prudential and AT&T, these fixed income investments yield more than similarly rated bonds due to their subordinated position in the capital structure – an average 5.3% at the end of 2019 compared with 4.1% for municipal bonds, 3.8% for corporate bonds and 1.9% for 10-year Treasurys.

Distributions are often treated as qualified dividend income, taxed at a top rate of 20% versus 37% for interest income (plus a 3.8% Medicare surcharge in both cases). In the past five years, a 50/50 mix of municipal bonds and preferred securities delivered a higher return than municipal bonds alone, with less volatility. ‘The mix also appears attractive from an after-tax yield perspective, generating 50 basis points of extra yield over standalone municipal bonds,’ Cordes added.

4. EMERGING MARKET DEBT

With the signing of phase one of the US-China trade deal and early signs of improving global manufacturing activity, many emerging markets should benefit from better trade and global growth prospects. The yield on US dollar-denominated sovereign emerging market debt (EMD), as measured by the yield to worst of the JPMorgan EMBI Global Core index, is 4.8%. Lustig points to the potential for yields to fall, as they did in developed countries during the last decade, pushing the prices of assets upward and piling capital gains on top of attractive income. While EMD does not diversify equity risk – often falling when equity markets do – he believes a ‘thoughtful allocation’ makes sense. Palfrey likes corporate and sovereign debt in many Latin American markets, which he said offer a ‘significant yield premium with greater return potential in a market that may be better supported through improved global trading activity’.

5. SHORTER-DATED INVESTMENT-GRADE BONDS

US credit markets were among the strongest performers last year. The Bloomberg Barclays US Aggregate Bond index was up 8.7%, with US investment grade corporate bonds leading the pack. Within this space, Loomis Sayles’ Palfrey suggests investors focus on shorter-dated, higher-quality offerings that have less price sensitivity to potential US rates or spread change. ‘Investors should position with quality, liquidity and short-maturity yield in mind and be patient,’ he said. ‘With yield and spread valuations quite full by most historic measures, investors should treat their fixed income portfolio more as a store of value for now with a mind towards re-entering risk markets at more attractive levels. ‘We may not yet know what the risk event will be, but as always, there will be a correction, and it’s more comforting to buy the dip than to be the forced seller in a weaker market.’

6. TREASURY INFLATION-PROTECTED SECURITIES

US Treasury yields fell by as much as 100 basis points last year in response to weaker manufacturing activity and more accommodative Fed monetary policy. When designing a balance investment portfolio, Palfrey believes investors should have a meaningful allocation to the Treasury market, which represents nearly 40% of the Agg index, for liquidity and safety purposes, particularly in light of the late expansion phase of the credit cycle we are currently in. With US Treasury yields already quite low, a diversifier could be to add some Treasury inflation-protected securities (Tips) within an investor’s Treasury allocation. ‘Tips are a relatively more attractive way to build in some interest-rate protection in a portfolio, should inflation eventually start to get some traction in the current full employment environment or if oil prices stay elevated due to increased geopolitical concerns,’ he said.

Focusing on quality with Madison Dividend Income

JOHN BROWN, CFA® PORTFOLIO MANAGER, MADISON DIVIDEND INCOME FUND

There are few funds that can draw on a 32-year history of calibrating their investment processes – fewer still once the field is narrowed to dividend income strategies. John Brown and Drew Justman, who co-manage the Madison Dividend Income fund (BHBFX), anchored their investment approach in Brown’s past experience of serving conservative bank trust clients. ‘I’ve been using and fine-tuning the strategy for more than 30 years,’ Brown said. ‘Our relative yield approach came from a background of serving conservative clients who desired equity exposure but were risk-averse. ‘So the question is, how can we achieve good returns, provide an income and growing dividends but avoid big drawdowns in bear markets? Because that helps clients stay invested in the market when they feel like getting out,’ Brown continued. ‘The answer we’ve come up with over the years, is that we buy high-quality, large-cap, blue chip stocks with above average dividend yields when they’re out of favor. ‘These are household names like Procter & Gamble and Home Depot. We buy them when they’re out of favor, which means the price is down and the yield is higher than normal and we get paid to wait for the price to recover.’ At the heart of Madison’s investment process lies the selection of stocks with attractive relative yields. A stock’s relative yield is its dividend yield divided by the market dividend yield. The strategy typically invests in 40 to 50 well-established large-cap companies. Selection criteria include above market yield, with a preference for companies that have historically increased their dividends. To develop confidence that this yield rise is likely to continue, Brown and Justman, along with their research team, look for two key elements in a stock: a sustainable competitive advantage - or ‘wide moats’ - and a strong balance sheet. ‘We are capitalizing on the realization that, historically, a high percentage of the total return in stocks have come from dividends,’ Brown said. ‘We believe that the resulting portfolio should be especially attractive to investors who are seeking yield, particularly in today’s low-yield environment.’ A crucial step in Madison’s investment process is to avoid companies where problems are terminal and not just temporary. This approach is designed to keep stocks that are unlikely to recover out of the portfolio. Diversification is another important factor in the team’s bottom-up selection process. The strategy can invest up to 20% or two times the S&P 500 sector weight into any one sector. Brown and Justman believe this provides enough flexibility to differentiate the fund from the index without being overly concentrated.

DREW JUSTMAN, CFA® PORTFOLIO MANAGER, MADISON DIVIDEND INCOME FUND

Pharmaceuticals company Bristol-Myers is a good example of how Madison’s investment approach works in action. The stock flashed up on Madison’s radar when it started to deliver above-expectation earnings at a cheap equity price. When the team took a closer look, they liked what they saw: the stock had a wide moat at 11 times earnings with a 3.6% dividend yield and high financial strength with an A-plus-rated balance sheet by S&P. When Brown and Justman drilled down into why the stock was cheap, they found that Bristol-Myers had a thin pipeline of new products and a merger proposal with large biotech company Celgene on the table. ‘We thought that, strategically, this makes the pipeline better and would make them (Bristol-Myers) a leader, especially in the cancer area. With a little over two times debt to EBITDA, the stock looked attractive. We thought that there would probably be no other bidders emerging and those expectations all turned out to be correct,’ Brown said. ‘Since we bought it in August, they raised their dividend by 10% and rallied substantially by 45% or so. We’re still getting a 2.7% yield and paying 10 times this year’s earnings for it.’ Risk control and seeking to protect capital in down markets is just as important to the team as achieving solid returns when markets rally. Madison believes that keeping investors in the market through tough times is a key element to achieving long-term results. ‘We attempt to hold up much better in down markets. The fourth quarter of 2018 is a good example,’ Justman said. ‘We were down 6.2% while the S&P 500 was down 13.5%. One important question for investors looking for yield in the current environment is: at what risk are they prepared to get involved?

‘We like to find stocks that have above-average dividend yield with a history of dividend growth – not necessarily the highest yielding stocks in the market,’ Brown said. ‘Some utility companies have high yields, for example, but they don’t have the ability to grow. They may not have a wide moat. They just don’t meet the characteristics.’ Following the 10-year bull market, Madison warns that investors might not be prepared for the next bear market. ‘We focus on protecting during the downside, so whenever the next bear market comes, we expect to hold up better than the index, and that might be a good way for people to stay invested and realize the long-term potential from equities,’ Justman said.

Indices are unmanaged. An investor cannot invest directly in an index. They are shown for illustrative purposes only, and do not represent the performance of any specific investment. Index returns do not include any expenses, fees or sales charges, which would lower performance. Before investing, please fully consider the investment objectives, risks, charges and expenses of the fund. This and other important information is contained in the current prospectus, which you should carefully read before investing or sending money. For more complete information about Madison Funds® obtain a prospectus from your financial adviser, by calling 800.877.6089 or by visiting https://www.madisonfunds.com/individual/prospectus-and-reports to view or download a copy. Performance data shown represents past performance. Investment returns and principal value will fluctuate, so that fund shares, when redeemed, may be worth more or less than the original cost. Past performance does not guarantee future results and current performance may be lower or higher than the performance data shown. Visit madisonfunds.com or call 800.877.6089 to obtain performance data current to the most recent month-end. ©2020 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. As of 12/31/2019, the Madison Dividend Income Fund was rated against the following numbers of Morningstar Large Value funds over the following time periods: 1091 funds in the last three years, 945 funds in the last five years, and 690 funds in the last ten years. Past performance is no guarantee of future results.

Where can we turn for decent income?

ANDREW TOBUREN SENIOR PORTFOLIO MANAGER, CHARTWELL INVESTMENT PARTNERS

What challenges are fixed income investors facing at the moment? Around the globe, interest rates are very low, and in fact negative in many places. That’s frustrating for advisors, investors and managers alike. It doesn’t seem right that many investors have acted prudently, stayed the course with an investment plan, accumulated some degree of wealth or are on the path to accumulating wealth, yet find themselves in an environment of rotten investment choices. Traditional fixed income allocations like the Aggregate Index have performed reasonably well over the last few years, but today they offer a very low yield and a relatively long duration. So, fixed income is not doing what it’s supposed to do? Prior to the financial crisis, there was a more reasonable level of income available from core allocations in the asset class, maybe 5%, but it also provided a certain measure of total return potential or hedge against some riskier areas of a portfolio. A lot of that has changed. The difference today is that it’s hard to envision a scenario where any significant price appreciation is achievable on a go-forward basis. Really, we are just left with the income component. Yet, still, the prospect of price declines could end up flipping total returns negative in many portfolios. What options can investors pursue in this environment? Investors do have choices. They can target longer duration portfolios for more income, but of course that brings greater interest rate risk. They can target lower credit quality for more income, but of course that adds a significant element of credit risk. Emerging market or frontier market debt is another option, but they come with the associated geopolitical and currency risks. Elsewhere, structured notes or derivatives can be considered, although there is a certain amount of complexity and illiquidity risk in those types of investments. One area that’s grown institutionally is the private debt market. This is potentially an attractive area but investors will be rightfully concerned about liquidity. Often, your money is locked up for several years and you are exposed to the credit risk and underwriting standards of a new market that lacks the transparency of public markets. So there are options, but our position is that none are great because each comes with an aspect of risk that investors may be uncomfortable with. The Chartwell Short Duration BB-Rated portfolio is designed to harvest income while limiting risk. Can you talk us through the strategy and its parameters for risk? We’ve tried to be thoughtful in designing an understandable strategy that aims to deliver consistent monthly income. The strategy’s foundation lies on two key risk-control guardrails. The first guardrail is quality, where we focus on BB-rated corporate bonds. These bonds reside in the crossover area between the traditional high yield market and the traditional investment grade market. BB’s have historically held up relatively well in down credit cycles, and this is an area where we’re regularly able to uncover inefficiencies and capture extra income. The second guardrail is that the portfolio is short maturity. We limit the portfolio’s average maturity to less than three years, which helps to mitigate both interest rate risk and credit risk. What we’ve found, is that these two structural risk guardrails can work in combination to help generate reasonable levels of consistent monthly income. Over full cycles, the incremental total return per annum has been 1% - 2% greater than traditional core fixed income allocations. Interestingly, the return profile has not been substantially more volatile than the Aggregate.

Andrew Toburen, manager of the Chartwell Short Duration BB-rated fixed income strategy, discusses the crossover area between traditional high yield and investment grade, and how it can provide value for income-seeking investors

From a construction standpoint, we buy US dollar-denominated, publicly traded bonds in a transparent portfolio that is priced daily. We don’t utilize any derivatives, credit default swaps, emerging market securities, structured notes or pay-in-kind / toggle bonds. What challenges do you anticipate for the strategy going forward and for the sector more broadly? Operating a short maturity strategy does present a challenge because we regularly have 30% or 40% of the fund come back to us each year through refinancing activity – bonds being called or tendered for. Our challenge is to continually redeploy funds and recycle exposure out into the market. That’s where our team’s fundamental credit research comes into play. We’ve focused on this space for the past fourteen years, and believe we’ve built up a knowledge base that helps us to stay invested and continue generating income. More broadly, I do believe there is a risk for short maturity strategies that own the full credit spectrum of high yield bonds, which are the majority of assets raised in the space over the last decade. Portfolios that own BB-rated bonds, B-rated bonds, and CCC-rated bonds have enjoyed a tailwind of easy credit conditions. Eventually, we believe we’ll see softness in the economy, or even a recession. If we do, we think strategies without a quality guardrail can really take it on the chin – the underperformance can be substantial, as we saw in 2008. In summary, Chartwell’s approach to the short maturity corporate space employs two risk guardrails and tries to balance the trade-off between more income and risk. We focus on BB-rated securities, and typically don’t own B-rated or CCC-rated credit. It’s definitely a niche, a niche we like as part of an income solution.

A GREAT CATCH

Options for capturing income are increasingly scarce but flexible strategies are helping to exploit inefficiencies in the credit markets

The fixed income markets have been navigating unsteady terrain and meagre returns for some time. Yields are now at, or close to, record lows in many markets, yet the value proposition of the asset class hasn’t gone away. Indeed, money has poured into the US corporate bond market over recent months. Should yields remain at historic lows, income investors may again find that there are few options for capturing income on a consistent basis. All of this begs the question – should core fixed income allocations be redefined? Yes and no, said Eric Jacobson, director of fixed income research at Morningstar. ‘I do think there is a risk of overreacting. It would be wrong-headed to say, “yields are low, there’s no risk mitigation here, therefore we need to redefine and move out of US Treasurys”. Even if you think that high-volume Treasury assets are a negative choice because they are so bereft of yield, it’s always going to be comparative. The highest utility of a high-quality allocation is that it serves as a refuge.’

ON VIEW: ABSOLUTE RETURN

But the dilemma for income-seeking investors remains: move up the risk scale and try to achieve more yield, or reassess their yield expectations? At the Philadelphia-based Brandywine Global, head of global credit Gary Herbert points out that investors can take advantage of this market dislocation via absolute return fixed income. Absolute return strategies are not constrained by a benchmark, can take both short and long positions, depending on the manager’s view of the market using derivatives, and can have an emphasis on delivering positive returns with lower volatility than the market. Low correlation to traditional equity and bond markets is also a useful diversifier. Herbert said: ‘One of the things that we’ve improved in our portfolios since 2015 has been making sure that we use duration as a ballast for when there’s a growth shock, a trade scare or a political act that creates volatility. That’s where absolute return has been very helpful in allowing us to preserve value.’ Jacobson agrees that absolute return is a reasonable place to allocate money for some investors. ‘But what we saw in the US a few years ago is that managers pulled back from it. Most absolute return strategies have high-cost hurdles and, to some degree, that’s by design. Everyone’s looking for a high-margin product to sell. ‘The tricky element to absolute return products is that, when yields are so low, managers do end up in a situation where they need to both earn enough return to beat their cost hurdles and shield portfolios from interest-rate risk. What they end up doing is hedging their duration down to short or low. The only other thing you can do in the portfolio to stay competitive is to take on credit or structural risk.’ ‘Structured credit is an area that we dialled up over the last year,’ Herbert said. ‘But duration has been the most dynamic element of what we’ve done. Going into Q3 2019, we had a duration close to five or six years. We extended it to 10 years, and today, we have a duration of roughly four years. We’ve been consistent in maintaining a significant weight to the front end of the high-yield curve – significant in terms of maintaining an investment-grade credit. We felt that it would outperform Treasurys and obviously it did.’

THE CLO PLAY

According to Jacobson, many managers over the past few years have taken a strong view on, and a substantial position in, a variety of very high-quality asset-backed securities or structured products. These are often AAA-rated tranches of commercial-backed securities, collateralised loan obligations (CLO), other securitised consumer loans and even some residential mortgage securities. These are securities that have enough enhancement or protection at the tranche, or at the level within the capital structure, they invest. CLOs are a way to activate defences without giving up a lot of yield or spread, which means that managers don’t really have to worry about the global recession risk. ‘But valuations have grown so tight that even in areas of increased popularity like CLOs, we’re now starting to see yellow flags,’ Jacobson said.

2020 RISK WATCHLIST

The growing gulf between political visions for the US, trade uncertainty in the UK around Brexit and the continued viability of the eurozone makes avoiding losses a certain challenge. ‘We try to understand what the market is pricing in,’ Herbert stressed. ‘Obviously, the US election and Brexit have been challenging on currencies and credit spreads. But we also look for the tail risks where we could be wrong. We were astute in terms of anticipating Brexit as well as the surprise outcome of the 2016 US election. Astute because we were correctly positioned. ‘We had significant duration in both of our portfolios. We had exposure in the UK guilts market, which rallied, but we hedged out the sterling and then we had significant duration in the US around the election.’ Is there still scope for the Federal Reserve and the other central banks to raise rates? ‘I think because it’s an election year, the Fed will be on hold for the shorter term. I do think there will be an adjustment to interest on reserves. The Fed is likely to be very accommodating if there are any problems.’ On the US-China trade question, Herbert said their approach is to understand the likely outcomes and turn them into scenario analyses. ‘We recognise the seriousness that the tariff battle can and has had in terms of global trade volumes. Therefore, we moved to minimise much of our emerging market global currency exposure and instead focus on higher-quality duration opportunities within the US. That has been very beneficial for us.’

RETURNS WITH CAUTION

The various layers of uncertainty – from political risk to credit risk – has led the Brandywine manager into a measured outlook for bonds. ‘We’ve seen a lot of pessimism around bonds recently, but 2019 was a good year for credit, emerging markets and long-duration bonds globally. There are still ample ways to earn attractive returns on a risk-adjusted basis in the bond market.

A tough environment indeed. The more secure a security is, the more expensive it is. Does this mean the end of traditional fixed income investing? Not quite. But as the bond bull market fades, a more nimble and innovative approach to fixed income is required – an approach that looks to limit the duration risk but also capture the yield characteristics that fixed income provides. In many instances, absolute return investments are providing some acceptable answers.

‘In light of slowing growth in China and ongoing political risk in emerging markets, allocating to the right sectors as well as to the right sovereign bonds will allow for good returns while also providing a significant hedge against downside risk. If we see more significant inflation, then we’ll have a repricing, but that will present a good entry point.’ While broadly positive, Jacobson is more willing to sound the horn. ‘Many managers are extremely cautious right now. There’s a lack of predictability in the market. We’re going through a period where I think managers are wary of putting too large of a call into a portfolio, even if they feel very confident.’

Income Generation In A Low-Rate World

JONATHAN MOLCHAN EXECUTIVE DIRECTOR, LEAD PORTFOLIO MANAGER NATIONWIDE RISK-MANAGED INCOME ETF (NUSI)

With yield increasingly scarce, what are some of the market areas that investors might target to attain the income they need? Amid a persistent low-rate environment, investors and advisors alike have increasingly sought out alternatives to traditional bond investing. These alternatives include high-dividend stocks, real estate, emerging market debt, preferred stocks and high-yield bonds. However, it is important to fully understand the potential benefits and risks that come with these alternative income strategies. Yes, there is the potential benefit of high income; but one must really look below the hood to understand what they are exchanging for that measure of high income. For instance, do these strategies exhibit low volatility, provide portfolio protection or have enough liquidity? How does your strategy differ? Our approach uses an options-trading strategy for income generation. An option is the right, but not the obligation, to buy or sell a security at a specified price and date in the future. They can be used to speculate on the future direction of a security. Specifically, our strategy targets high monthly income with fewer risks relative to traditional income-focused investments. It seeks to provide investors with a measure of downside protection along with the potential of upside participation. The strategy is fundamentally designed with income generation in mind. It seeks to give investors and advisors the ability to generate high monthly income without adding excess interest rate sensitivity, duration-associated risk, inflation, leverage or commodity exposure.

Jonathan Molchan, lead portfolio manager of the Nationwide Risk-Managed Income ETF (NUSI), discusses how option-based strategies can provide a foundation from which to generate income while also seeking to protect investors from losses in down markets

Go to etf.nationwide.com for prospectus outlining investment objectives, risks, fees, charges and expenses, and other information that you should read and consider carefully before investing. Investing involves risk, including the possible loss of principal. Shares of any ETF are bought and sold at market price (not NAV), may trade at a discount or premium to NAV and are not individually redeemed from the Fund. Brokerage commissions will reduce returns. The Fund’s return may not match or achieve a high degree of correlation with the return of the underlying index. Nasdaq® and the Nasdaq-100® are registered trademarks of Nasdaq, Inc. (which with its affiliates is referred to as the “Corporations”) and are licensed for use by Nationwide Fund Advisors. The Product has not been passed on by the Corporations as to their legality or suitability. The Product is not issued, endorsed, sold, or promoted by the Corporations. THE CORPORATIONS MAKE NO WARRANTIES AND BEAR NO LIABILITY WITH RESPECT TO THE PRODUCT. Nationwide Fund Advisors (NFA) is the registered investment advisor to Nationwide ETFs, which are distributed by Quasar Distributors LLC. NFA is not affiliate with any distributor, subadviser, or index provider contracted by NFA for the Nationwide ETFs. Nationwide is not an affiliate of third-party sources such as Morningstar, Inc or MSCI. Representatives of the Nationwide ETF Sales Desk are registered with Nationwide Investment Services Corporation (NISC), member FINRA, Columbus, Ohio. MFM-3521AO (01/20)

Let’s review in more detail. How can options be used as a source of income? Given that options can be both bought and sold, the primary objective of using the instrument to generate income is by selling an option and in return the seller receives an options premium. Investors can turn to professional, risk-managed options’ strategies to potentially exploit current market dynamics whereby the strategies can adapt to current trading environments to grant a higher probability of success. Success would be defined as the best risk-adjusted return while maximizing income generation combined with a reasonable measure of downside protection. Simply put as the markets change the rules-based dynamic nature of the positioning of the options in these strategies will change as they seek the highest probability of a positive outcome. First, we seek to replicate the Index by purchasing all its underlying stocks. Then we deploy our rules-based strategy and couple the underlying stocks with index options. We sell a near-at-the-money to out-of-the-money call option to generate options premium and use a portion of the premium to purchase a protective put below the current market level. Then we distribute a monthly dividend using a portion of the options premium and seek to reinvest remaining net premium. How does this strategy build in protection for the investor? As described, we use a protective net-credit collar options strategy. This strategy combines two common options strategies but regarding protection we can focus on the protective put. Although this strategy combines two common options strategies – selling calls and buying puts – the primary goal of purchasing a put option is to limit potential losses in a price decline. It’s important to note that this put cannot be exercised and is always present. The profitability of a protective put is determined by the gains in the underlying stock minus the cost of purchasing the put option. However, in exchange for foregoing some of the upside, an investor can potentially benefit from limiting the maximum potential loss. This is because the put option will profit if the stock price declines below the strike price. This strategy is ideal for investors with a bullish outlook who are looking to hedge a long position in an underlying stock in the event of a downturn. How would you expect this strategy to perform in different market environments? Our strategy follows a systematic, rules-based system which allows us to close the short-call option prior to expiration. This, in effect, ‘uncaps’ the portfolio by allowing the underlying equity portfolio to potentially participate in a rising market. So, in a rising stock market, total return will likely come from capital appreciation of the underlying stock portfolio. The covered call component used as a part of the net-credit collar strategy may limit some of the upside growth potential but will still support the monthly dividend. In a sideways market, the strategy will pay its monthly dividend from the net-credit due to the covered call component and benefit from a potential move higher in the equity market while still providing a measure of downside protection from the protective put. In a down-trending stock market, the strategy is designed to seek higher total return than standard covered call strategies as well as the broader equity market. The net-credit from the covered call component will support the monthly dividend while the protective put seeks to preserve portfolio capital if the equity market drops below the put strike price.

Fixing Fixed Income with Non-Traditional Income Sources

Interest rates appear to be staying lower for longer, continuing to erode the real after-tax income investors need. Yield-starved investors need to consider broadening their opportunity set and diversifying with non-traditional income sources that have exhibited lower correlations, while being aware of the risk/return trade-offs. The field of yield possibilities may surprise them, particularly ETFs that offer innovative and differentiated exposure in hard-to-manage and difficult-to-access, non-traditional income asset classes. Notable categories include: Preferred Stocks – With a combination of low correlation, modest volatility, and high yields, preferred stocks have clearly gained attraction in a low yield environment. While index-based strategies hold a large majority of assets in the category, active management has trumped passive preferred stock funds over the long run, according to Morningstar. Private Credit – This growing asset class offers investors a different way to access alternative assets. Private credit players like business development companies (BDCs) carry less leverage than banks and are subject to diversification requirements. We expect credit fundamentals will remain strong and the market for private credit will continue to grow, especially in light of recent comments by the chief investment officer of the largest pension fund in the United States regarding direct lending strategies not currently in the fund’s portfolio – but should be. Utilities – Consider utilities an increasingly popular defensive play late in the cycle, given the potential for strong risk-adjusted returns and dividend growth. The sector continues to benefit from the combination of strong operating fundamentals and a supportive regulatory/legislative backdrop. Real Assets - As an alternative to traditional bonds, investors have begun allocating to real assets (real estate, infrastructure, and natural resources), which can offer both attractive yield and appreciation to protect against inflation. They also have demonstrated the potential to provide a degree of downside protection, having historically generated less volatility as a result of the income component associated with the asset class. Real estate fundamentals are likely to stay comparatively strong; infrastructure should benefit from long-term contractual agreements that help contribute to their stable revenue streams; and natural resources may benefit from being cheap relative to traditional financial assets. Leveraged Loans – Loans remain a compelling opportunity for every ETF investor’s fixed income portfolio, regardless of the direction of interest rates, but passive strategies can be inordinately risky. Active managers have the ability (and agility) to adjust to credit, liquidity, and trading risks during different parts of the business cycle. Master Limited Partnerships (MLPs) - We expect earnings to continue to be solid as volumes continue to increase and new projects come on line. After significant M&A activity last year, we expect additional strategic activity in the MLP sector as valuations are very depressed relative to Treasury bonds and other yield investments.

Past performance is no guarantee of future results. Asset classes are not representative of any Virtus portfolio. For illustrative purposes only, the indexes are unmanaged, their returns do not reflect any fees, expenses, or sales charges, and are not available for direct investment. Source: Morningstar Direct, Virtus Performance & Analytics. All data as of 12/31/19. Yields for the various asset class indexes have material differences including investment objectives, liquidity, safety, fluctuation of principal or return and tax features. Fixed income yields are yield-to-worst, equity yields are current dividend yield, while MLP yield consists primarily of return of capital which reduces an investor’s adjusted cost basis. Standard deviation, which measures variability of returns around the average return, is for the five-year period. Higher standard deviation suggests greater volatility of returns. Correlation is a measure that determines the degree to which two variables’ movements are associated. The correlation coefficient will vary from -1 to +1. A -1 indicates perfect negative correlation and +1 indicates perfect positive correlation. Treasury Bonds represented by 10-Year U.S. Treasury; U.S. Stocks by S&P 500® Index; Balanced Portfolio by 60% S&P 500® Index/40% Bloomberg Barclays U.S. Aggregate Bond Index; Core Bonds by Bloomberg Barclays U.S. Aggregate Bond Index; Private Credit by Wells Fargo BDC Index; MLPs by Alerian MLP Infrastructure Index; Bank Loans by Credit Suisse Leveraged Loan Index; High Yield by Bloomberg Barclays HY 2% Issuer Cap Index; Preferred Stock by S&P U.S. Preferred Stock Index; Global Infrastructure by S&P Global Infrastructure Index; REITs by FTSE Nareit All Equity REIT Index; and Utilities by S&P Utilities Index. Learn more at www.Virtus.com This commentary is the opinion of Virtus ETF Advisors LLC. This material was prepared without regard to the specific objectives, financial situation, or needs of any particular person who may receive it. It is intended for informational purposes only and it is not intended that it be relied on to make any investment decision. It does not constitute investment advice or a recommendation or an offer or solicitation and is not the basis for any contract to purchase or sell any security or other instrument.

the mighty stream of sustainability

While the equity market played an early role in sustainable investing, bond markets have lagged. But mounting evidence suggests a focus on sustainability can build more resilient bond portfolios

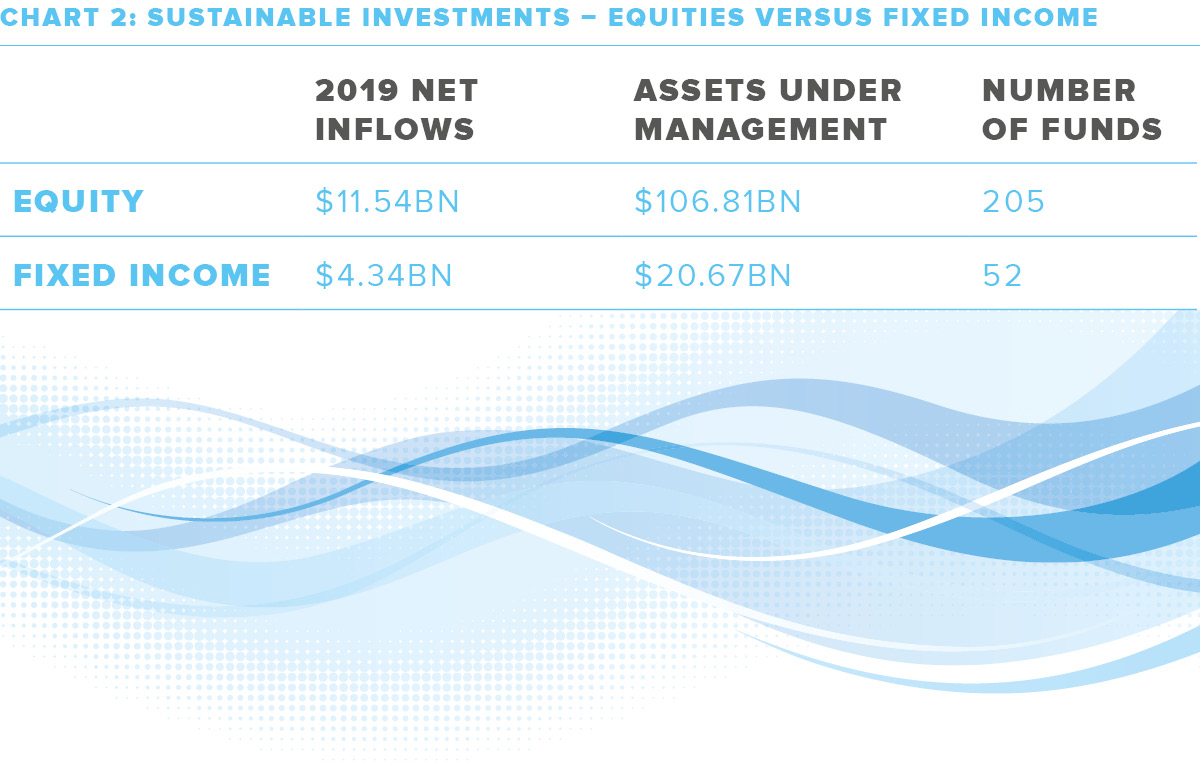

Sustainable investing now extends across the range of asset classes commonly found in diversified investment portfolios, but data shows fixed income is playing catch-up to equities. More than half (51%) of sustainable investments in the US, Canada, Japan and Europe were in public equities at the start of 2018, figures from the Global Sustainable Investment Alliance show. The next largest asset allocation was fixed income, with a 36% share (see chart 1). In terms of assets and numbers of funds, sustainable equities are more than four times the size of the fixed income market, an analysis by Touchstone Investments shows. Momentum is picking up, with more than $4bn net inflows to the sustainable fixed income space last year (see chart 2).

Andrew Parry, head of sustainable investment at Newton Investment Management, said: ‘There’s nothing like a bit of competition to spur developments in a market. The groundswell of enthusiasm for sustainable investing in recent years has largely been led by equities – public and private – but more latterly fixed income markets are rapidly recognising the relevance of sustainability criteria to their asset category.’ While fixed income investors cannot vote by proxies, larger investors have been increasingly exerting their influence on environmental, social and governance (ESG) factors that may impact an issuer’s credit quality. Loomis Sayles is an example of a company that is rapidly bridging the gap between equity investors and ESG principles. ‘Similar to the equity market, bondholders like us are aware that there are attitudinal shifts around the globe supporting ESG principles,’ said Steve Bocamazo, the firm’s credit research associate director. ‘Some have an immediate impact while others have a longer-term effect. ESG factors that will fully manifest themselves beyond the typical two- to three-year investment horizon are now becoming a higher priority for bond investors at the longer end of the curve.’

CLIMATE RISK

Given that resiliency is a key consideration for investors in the $100tn-plus global debt market, systemic risks associated with climate change should be at the forefront of their thinking, according to Parry. A recent publication by McKinsey, ‘Climate risk and response: Physical hazards and socioeconomic impacts’, vividly highlights the potential costs to capital markets of a rapidly warming climate, echoing warnings from Bank of England governor Mark Carney of potential bankruptcies at poorly prepared businesses. ‘The first rule of corporate sustainability is surviving – a consideration always close to the hearts of fixed income investors,’ Parry said. Investors need to ascertain the ability of impacted industries to adjust to changing regulations and whether investor sentiment will allow them to continue to access capital markets at a reasonable price over the bond’s term.

Sustainable fixed income is also playing a fundamental role in greening the brown sector of the economy. Not only does it address accountability and impact targets, but Reyl & Cie, the Swiss private bank, recognizes it as one of the most powerful tools for corporates to organize their transitions to more sustainable objectives. The green bond market has grown dramatically to hit a new record in 2019, with $255bn issued, up 49% on the previous year. ‘Green bonds issued by countries like Germany, the largest coal extractor in Europe, help to organize a true transition to clean energy by allocating that capital exclusively to new clean projects,’ said Fabio Sofia, head of debt and fixed income at Reyl & Cie.

GOVERNANCE

Yet, sustainable investing in the bond market goes beyond managing well-publicized climate-related risks. Governance has always been a consideration for bond investors – government as well as corporate – given the reliance on sound practice and adherence to rules that underpin the willingness to lend. ‘It is often thought that the voting power granted to equity holders gives them greater opportunity to engage with companies than bond investors, but that is rapidly changing,’ Parry said. ‘Investors, in corporate debt in particular, recognize that they have significant power to influence the management of the salient and material sustainability issues in a company due to the revolving nature of outstanding credit. ‘Companies constantly return to the debt market to finance day-to-day operations and longer-term investment plans. This affords bond investors the power to deny financing when a business is seen to be straying not only outside the bounds of financial prudence but also outside of environmental or social boundaries. ‘Equity investors might have the vote, but it is bond investors that have the capital and money talks. For both, sustainability is no longer an option: it’s an imperative.’ That argument is all the more compelling when you consider the influence that credit investors can have on a company’s cost of capital and the size of the bond market. ‘Don’t forget that the size of the fixed income market is many times that of the equity market,’ said Chris Bowie, portfolio manager at TwentyFour Asset Management.

PROPRIETARY APPROACH

Federated Investors’ credit analysts use ESG factors as an extension of their primary fundamental research in the same way its equity analysts do. ‘Regardless of the instrument, stock or bond, assessing financially-relevant ESG issues for a corporate issuer to determine the sustainability of future cash flows and mitigate risk provides a more comprehensive view and helps protect all investors’ blindside,’ said Martin Jarzebowski, director of responsible investing at Federated Investors. Yet, while the quantity and availability of ESG-related data has improved dramatically in recent years, coverage for fixed income markets still lags equities. One primary reason for this is that third-party ESG scores are typically sourced from publicly-listed equity data. ‘The trouble is that it leaves about 40% of global credit uncovered as many bonds are issued from special-purpose vehicles or unlisted entities,’ Bowie said. ‘This means that, for any credit investor to take ESG seriously, they need to score companies from an ESG perspective themselves.’ Consequently, dialogue with the issuer’s management is particularly valuable in the context of bonds. ‘As such, engagement regarding ESG matters is a priority for our research team,’ said Bonnie Wongtrakool, global head of ESG investments at Western Asset. Many asset managers have developed a proprietary approach. Aegon Asset Management combines internal and external research using both qualitative and quantitative inputs to identify issuers aligned with sustainable megatrends and ultimately build a sustainability-themed fixed income strategy. ‘The fixed income universe presents investors interested in sustainable investing with a wide variety of investment opportunities, many of which are not accessible through equities,’ said James Rich, chairperson of Aegon Asset Management’s sustainable investment committee. Examples include the debt of sovereign countries and municipalities that have a positive overall sustainability agenda and numerous sustainable sectors within securitized finance. Residential and commercial mortgage-backed securities have the direct ability to support the fight against climate change and sustainable growth by providing low-cost finance to companies involved in affordable housing, clean energy and the energy efficiency of property. Within asset-backed securities (ABS), solar ABS, auto ABS backed by loans on electric or hybrid vehicles and equipment ABS that finance projects to improve energy efficiency also provide investors with the ability to back environmentally-friendly causes.

PIVOTAL YEAR

BlueBay Asset Management regards 2019 as a pivotal year for ESG investing – it became a lead topic for the media and politicians, and large swaths of investors changed their opinions on the importance of climate change. ‘Bond managers have been embedding ESG more visibly in the investment process for some years, and as investors allocate capital toward ESG offerings, the robustness of their approach will be tested,’ senior portfolio manager Blair Reid said. ‘ESG screening and engagement will be a much larger part in bond investors’ and bond managers’ thought processes going forward, and we welcome the positive impact that may have for all of us in the future.’

CITYWIRE INVESTMENT WARNING This communication is by Citywire Financial Publishers Ltd (“Citywire”) and is provided in Citywire’s capacity as a publisher for general information and news purposes only. Citywire does not provide investment advice. You understand that no content contained in this communication constitutes a recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. To the extent any of the content published in this communication may be deemed to be investment advice or recommendations in connection with a particular security, such information is impersonal and not tailored to the investment needs of any specific person. You understand that an investment in any security is subject to a number of risks and that discussions of any security published in this communication will not contain a list or description of relevant risk factors. This communication and the information included herein is for general information purposes only and does not constitute an offer to sell or solicitation of an offer to purchase any security or any advisory or trading management service. Information presented in this communication does not represent the views or recommendations of Citywire, nor the opinion of Citywire on whether to buy, sell or hold any particular security. Users of this communication are advised to conduct their own independent research into individual securities before making a purchase, sell, or hold decision. In addition, investors are advised that past performance or portfolio performance is no guarantee of future price appreciation or performance. Citywire uses information obtained primarily from sources believed to be reliable (such as company reports and financial reporting services) however Citywire cannot guarantee the accuracy of information provided, or that the information will be up-to-date or free from errors. Investors and prospective investors should not rely on any information or data provided by Citywire but should satisfy themselves of the accuracy and timeliness of any information or data before engaging in any investment activity. All content in this communication is presented only as of the date published or indicated, and may be superseded by subsequent market events or for other reasons. As markets change continuously, previously published information and data may not be current and should not be relied upon. If in doubt about a particular investment decision an investor should consult a regulated investment advisor who specializes in that particular sector. Information includes but is not restricted to any video, article or guide content created or provided by Citywire. No Investment Recommendations or Professional Advice: The communication does not, and is not intended to; provide tax, legal, or investment advice. Nothing in this communication should be construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any security by Citywire or any third party. You are solely responsible for determining whether any investment, security or strategy, or any other product or service, is appropriate or suitable for you based on your investment objectives and personal and financial situation. You should consult an attorney or tax professional regarding your specific legal or tax situation. terms of service Citywire USA is owned and operated by Citywire Financial Publishers Ltd (“Citywire”). Citywire is a company registered in England and Wales (company number 3828440), with registered office at 1st Floor, 87 Vauxhall Walk, London, SE11 5HJ 1. Intellectual Property Rights. 1.1 Unless otherwise expressly indicated, we are the owner or licensee of all copyright, trademarks and other intellectual property rights in and to all content included in our publications (including all information, data, graphics, text, photographic images, moving images, sound, and illustrations in them and the selection and arrangement thereof) (collectively referred to as “Content”). CITYWIRE is trademark owned by Citywire and may not be copied, imitated or used, in whole or in part, without the prior written permission of Citywire. You acknowledge and agree that all copyright, trademarks, trade dress and other intellectual property rights in this Content shall remain at all times vested in Citywire and / or its licensors. 1.2 This Content is protected by copyright laws and treaties around the world. All such rights are reserved. Images and videos used on our websites (“Third Party Content”) are © iStockphoto, Shutterstock, Thinkstock, Topfoto, Getty Images or Rex Features (among others). For credit and/or permissions information relating to specific images where not stated, please contact picturedesk@citywire.co.uk. 1.3 You must not copy, reproduce, modify, create derivative works from, transmit, distribute, publish, summarise, adapt, paraphrase or otherwise publicly display any Content without the specific written consent of a director of Citywire. This includes, but is not limited to, the use of Citywire content for any form of news aggregation service or for inclusion in services which summarise articles, the copying of any fund manager data (career histories, profile, ratings, rankings etc) either manually or by automated means (“scraping”), the use of data mining, robots or similar data gathering or extraction methods, or the use of any means of circumventing, disabling or otherwise interfering with security-related features and/or copyright management information. Under no circumstance is Citywire content to be used in any commercial service. You must not copy, reproduce, modify, create derivative works from, transmit, distribute, publish, publicly display or otherwise use any Third Party Content. 2. Non-reliance. 2.1 You agree that you are responsible for your own investment decisions and that you are responsible for assessing the suitability and accuracy of all information and for obtaining your own advice thereon. You recognize that any information given in this Content is not related to your particular circumstances. Circumstances vary and you should seek your own advice on the suitability to them of any investment or investment technique that may be mentioned. You specifically acknowledge that Citywire is not liable for losses or gains arising out of information of any type in this Content, or damages or losses associated with any other use of this Content. 2.2 The fund manager performance analyses and ratings provided in this Content are the opinions of Citywire as at the date they are expressed and are not recommendations to purchase, hold or sell any investment or to make any investment decisions. Citywire’s opinions and analyses do not address the suitability of any investment for any specific purposes or requirements and should not be relied upon as the basis for any investment decision. 2.3 Persons who do not have professional experience in participating in unregulated collective investment schemes should not rely on material relating to such schemes. 2.4 Past performance of investments is not necessarily a guide to future performance. Prices of investments may fall as well as rise. 2.5 Persons associated with or employed by Citywire may hold positions or take positions in investments referred to in this publication. 2.6 Citywire Financial Publishers Ltd operate a policy of independence in relation to matters where the operators may have a material interest or conflict of interest. 3. Limited Warranty. 3.1 Neither Citywire nor its employees assume any responsibility or liability for the accuracy or completeness of the information contained on our site. 3.2 You acknowledge and agree that any information that you receive through use of the site is provided “as is” and “as available” basis without representation or endorsement of any kind and is obtained at your own risk. 3.3 To the maximum extent permitted by law, Citywire excludes all representations, warranties, conditions or other terms, whether express or implied (by statute, common law, collaterally or otherwise) in relation to the site or otherwise in relation to any Content or Feed, including without limitation as to satisfactory quality, fitness for particular purpose, non-infringement, compatibility, accuracy, or completeness. 3.4 Notwithstanding any other provision in these Terms, nothing herein shall limit your rights as a consumer under English law. 4. Limitation of Liability. To the maximum extent permitted by law, Citywire will not be liable in contract, tort (including negligence) or otherwise for any liability, damage or loss (whether direct, indirect, consequential, special or otherwise) incurred or suffered by you or any third party in connection with this Content, or in connection with the use, or results of the use of Content. Citywire does not limit liability for fraudulent misrepresentation or for death or personal injury arising from Citywire’s negligence. 5. Jurisdiction. These Terms are governed by and shall be construed in accordance with the laws of England and the English courts shall have exclusive jurisdiction in the event of any dispute in connection with this Content or these Terms.