SCROLL

HEADLINES

OVERVIEW

ALTERNATIVE SECTORS�& NEW ENTRANTS

MORE OR LESS?

WHERE ARE�THEY MOVING

WHO IS MOVING?

LESS BUT BETTER?

SO WHAT?

NATIONAL�OFFICE�MOVES

2025

THE COMPREHENSIVE ANALYSIS OF THE WHO, WHAT, WHY and WHERE�of OFFICE RELOCATIONS ACROSS THE UK REGIONAL MARKETS.

Established companies

Comprises all occupiers that already have an office in a market.

MOVER

An office relocation�within the same market.

An office expansion, either within the existing office location or an additional location within the same market.

EXPANSION

Comprises all occupiers that have relocated their office from outside a market�or are a new occupier.

NEW�ENTRANTS

Comprises all education & medical occupiers who have taken office space in a market - not included in the relocations data.

EDUCATION & MEDICAL

Comprises all flexible workspace providers who have taken a traditional lease or signed a management agreement in a market - not included in the relocations data.

FLEXIBLE WORKSPACE

CONTACT US

KIRAN�PATEL

Head of National Offices Research

kiran.patel@cushwake.com

Head of National�Office Agency

charles.dady@cushwake.com

Charles�Dady

Head of Midlands�Office Agency

scott.rutherford@cushwake.com

Scott Rutherford

Head of Yorkshire�Office Agency

adam.cockroft@cushwake.com

Adam Cockroft

HEAD OF LEASING,�UK

alistair.brown@cushwake.com

Alistair Brown

National Offices�Capital Markets

andrew.meikle@cushwake.com

Andrew�Meikle

Head of South West Office Agency

steve.lane@cushwake.com

Steve�Lane

Head of North West�Office Agency

rob.yates@cushwake.com

Rob�Yates

HOVER ON EACH BOX TO LEARN MORE

This was 11% above the 278 deals reported for 2023. Take-up for 2024 across these markets totalled 7 million sq ft, which represents a 22% increase on the 2023 total of 5.7 million sq ft, though remaining�10% below the five-year average.

Nearly half (46%) of these deals took place in the South East, with a total of 142 transactions—an 8% increase from 2023. Indeed, all regional markets saw�a rise in deal activity, except for Birmingham which recorded a minor decline of one deal.

The resilience of the regional office market across the CBDs of the Big Five regional markets and the South East is reflected in its diverse mix of occupiers.

CENTRAL LONDON OFFICE�LEASING COMPOSITION

An additional 196 deals were completed by occupiers with an established presence in the regional markets.

Of these, 32 companies expanded their footprint—either by growing within their current premises or by adding new office space to their portfolio—accounting for 285,900 sq ft of take-up. A further 92,000 sq ft across 9 leases resulted from occupiers transitioning from serviced offices into conventional office space. 155 occupiers expanded or contracted their office space through relocating to new office space within the same market, or by contracting within their office space within their current premises.

Over the past few years, the education, medical, and flexible office sectors have become increasingly prominent in the regional office market.

Demand from higher education institutions accelerated in 2024, with universities increasingly acquiring prime office space to support administrative functions, research, and specialist teaching—particularly in city centre locations where traditional campus expansion is limited. The sector accounted for 17 deals during the year, contributing 457,400 sq ft of total take-up. A standout transaction was Aston University’s acquisition of 189,100 sq ft at 10 Woodcock Street in Birmingham, which represented the second-largest regional office deal of the year.

ABOUT CUSHMAN & WAKEFIELD

Cushman & Wakefield (NYSE: CWK) is a leading global commercial real estate services firm for property owners and occupiers with approximately 52,000 employees in nearly 400 offices and 60 countries. In 2023, the firm reported revenue of $9.5 billion across its core services of property, facilities and project management, leasing, capital markets, and valuation and other services. It also receives numerous industry and business accolades for its award-winning culture and commitment to Diversity, Equity and Inclusion (DEI), sustainability and more.

For additional information, visit www.cushmanwakefield.com.

There were 308 office transactions in excess of 5,000 sq ft across the ‘Big Five’ regional markets and the South East�in 2024.

OVERVIEW

2024 IN HEADLINES

DEAL OVERVIEW

THE�EXPANDERS

THE CONTRACTORS

THE�NET EFFECT

The South East accounted for nearly half (46%) of all deals, with 142 transactions, representing an 8% year-on-year increase.

A total of 308 office transactions over 5,000 sq ft were recorded across the Big Five regional city centre markets and the South East in 2024—an 11% increase on the 278 deals reported in 2023. Take-up totalled 7.0 million sq ft, which reflects a 22% increase on 2023, whilst still remaining 10% below the five-year average.

Education & Medical occupiers continued to grow their presence,

leasing an additional 567,900 sq ft across 27 deals in 2024.

New market entrants contributed to 12 additional transactions, half of which took place in Manchester, reinforcing its appeal�as a key regional hub.

Flexible workspace operators acquired 468,600 sq ft in 2024�across 20 transactions—more than triple the 136,000 sq ft transacted�in 2023.

Established occupiers within the Big Five and South East regions were behind 196 transactions, with 32 firms expanding their footprint within the same market—either by taking more space in their current premises or opening a second office—adding 285,900 sq ft of take-up.

Of these 196 deals, 114 (59%) involved footprint growth—either through additional offices, moves from serviced space, or relocations into larger offices—totalling 2.33 million sq ft of take-up and delivering 925,900 sq ft of net expansion.

The remaining 82 deals (41%) involved firms reducing their footprint through downsizing or relocation, generating 1.43 million sq ft of take-up but resulting in a net loss of 1.46 million sq ft compared to their previous space.

When accounting for both expansions and contractions, office deals across the Big Five and South East regions resulted in a net loss of 531,500 sq ft in 2024, with expansions outnumbering contractions but the scale of downsizing outweighing the gains on a sq ft basis.

In contrast, sectors including Pharmaceutical & Life Sciences, Manufacturing�& Energy, Technology, Retail & Leisure, and Insurance recorded notable net contractions, largely due to consolidations and flexible working strategies.

Occupiers increasingly consolidated into high-quality, amenity-led offices, with 80 expansions and 73 contractions occurring in Grade A space, highlighting shifting occupier preferences towards premium office space.

All Big Five regional markets recorded net gains in office space, with expansion deals dominating activity, while the South East saw a significant net loss of 793,800 sq ft, driven by a number of large-scale consolidations.

Sectors such as Banking & Finance, Media, Business Services, and parts of the Government & Public sector actively expanded in 2024, reflecting growth strategies, return-to-office momentum, and targeted regional focus.

GET IN TOUCH

GET IN TOUCH

Grade A offices recorded a net contraction of 691,600 sq ft, evidencing the continued relevance of the ‘less but better’ trend in the aggregate.

The Grade B/C market saw a modest net gain of 160,100 sq ft, though this was from far fewer deals—reinforcing that occupiers continue to prioritise top-tier space when adjusting their footprints.

Flexible Workspace operators took 468,600 sq ft of new space across 20 transactions in 2024, more-than tripling the 136,000 sq ft transacted in 2023. The presence of Education & Medical occupiers in the regional office markets continued to grow�in 2024, with these tenants leasing an additional 567,900 sq ft of office space across 27 transactions. Beyond these sectors, new market entrants contributed to 12 additional transactions, with half of them taking place in Manchester underscoring�the city's appeal as a key market.

ALTERNATIVE�SECTORS

ALTERNATIVE SECTORS &�NEW ENTRANTS

ALTERNATIVE�SECTORS

NEW�ENTRANTS

Additionally, the Victoria College of Arts and Design expanded into both Manchester and Leeds, with these two deals totalling 47,000 sq ft.

At the same time, the growth of the UK medical industry has driven increased demand for office space from medical and healthcare organisations. In 2024, the sector accounted for 110,400 sq ft of take-up across�10 deals. The largest of these was Health Services Laboratories, securing 50,100 sq ft of Grade A space at Croxley Park. Additionally, eyecare specialists SpaMedica expanded their presence in the South East through three deals totalling 31,700 sq ft.

ADDITIONAL TAKE-UP FROM�ALTERNATIVE SECTORS

The serviced office sector continues to grow in significance within the regional office market, with flexible workplace solutions catering to a wide range of occupier needs. In 2024, flexible workspace operators acquired 468,600 sq ft across 20 transactions—more than tripling the 136,000 sq ft transacted in 2023. Notably, IWG signed a lease for approximately 73,000 sq ft at the £1.3 billion Olympia redevelopment in West London. Further to this, serviced offices continue to play a vital role as a launchpad for smaller businesses and those in transition, providing the flexibility to scale operations—evidenced by 92,000 sq ft of take-up across nine leases from occupiers moving from serviced offices into conventional office space.

Excluding activity from alternative sectors, New Entrants to the regional markets accounted for 100,000 sq ft of take-up across 12 transactions during 2024.

Notably, half of these deals took place in Manchester, reinforcing the city’s status as a leading destination and key hub for business expansion. Among the New Entrants were three occupiers from the Retail & Leisure sector—Shein, Levy Merchandising, and VF Corporation—who collectively took up 26,700 sq ft across three deals. Another significant transaction saw communications regulator Ofcom lease 9,400 sq ft�at 1 Circle Square, establishing a new digital and technology hub in the city.

The largest deal involving a new market entrant was Glencore Industrial Assets’ relocation from London, securing 19,870 sq ft at One Bell Street in Maidenhead.

NEW�ENTRANTS

Firms with an established presence�in the Big Five and South East regional markets accounted for�196 office deals.

Of these, 32 companies expanded their footprint within the same market in addition to their existing portfolio —either by taking additional space within their current premises or opening a second office—resulting in 285,900 sq ft of additional take-up. In addition, nine firms transitioned from serviced offices to their own leased space, contributing a further 92,000 sq ft of take-up.

Conversely, four companies chose to reduce their footprint by downsizing within the same building, leading to a combined contraction of 31,200 sq ft. The remaining 149 deals involved occupiers relocating office space within the same market, equating to 2.44 million sq ft of take-up.

DEAL OVERVIEW

Out of these 196 eligible deals from established occupiers, 114 (or 58%) involved an addition to the firm’s footprint – either through the acquisition of an additional office,�a move from serviced office space,�or acquiring more space than their previous office through relocation.

In the aggregate, these expansions accounted for take-up of 2.33 million sq ft,and total expansion of 925,900 sq ft.

The two largest upsizes of 2024 were both in the Manchester market. BNY Mellon’s move to 196,400 sq ft�of space at 4 Angel Square was not only the largest deal in Manchester since 2018 and the largest Big Five office deal since 2020, but was also the largest upsize of 2024 as its relocation of two existing Manchester offices involved increasing the bank’s office footprint by 57,900 sq ft.

In addition, ARM’s move into 68,900 sq ft at No. 1 St Michael's in Manchester involved an upsize of 38,900 sq ft. Elsewhere, the BBC’s move to 84,000 sq ft at Typhoo Wharf in Birmingham includes taking 33,100 sq ft more space than its previous location at The Mailbox.

THE EXPANDERS

DEAL OVERVIEW

THE EXPANDERS

MORE OR LESS?

THE CONTRACTORS

THE NET EFFECT

The number of firms either reducing their space within their current office premises or through relocation totalled 82 – or 42% of deals from established occupiers.

All in all, take-up from firms reducing their office space footprint totalled 1.43 million sq ft, which represents a net loss of 1.46 million sq ft on their previous office space. All five of�the largest downsizes in 2024 occurred in the South East, the largest of which involved Johnson & Johnson consolidating�its three Thames Valley campuses that totalled approximately 299,300 sq ft into 97,500 sq ft at the Tempo building in Maidenhead. Other notable downsizes involved The AA reducing their space by 110,400 sq ft in their relocation from their long-term office in Fanum House to Plant in Basingstoke, and The Body Shop relocating to Plus X in Brighton, resulting in a contraction of 84,600 sq ft.

THE CONTRACTORS

Accounting for both occupiers expanding and contracting their space, office deals across the Big Five and South East regional markets resulted�in a net loss of 531,500 sq ft in 2024.

While more established occupiers chose to expand rather than reduce their footprint, this overall net loss suggests that the scale of downsizes or relocations outweighed the additional take-up gained through expansions, indicating a continued trend of consolidation and a more measured approach�to long-term office space commitments.

Among the various size bands, net expansions in office space were limited but notable. The 100,000+ sq ft category saw only expansionary activity, resulting�in a net gain of 83,100 sq ft.

The largest deal involving a new market entrant was Glencore Industrial Assets’ relocation from London, securing 19,870 sq ft at One Bell Street in Maidenhead.

THE NET EFFECT

However, these gains were outweighed by more substantial losses in other categories. The 10,001–20,000 sq ft band recorded 42 expansion deals compared to 25 contractions, but the scale of space released meant this translated into a net loss

of 34,500 sq ft—highlighting the uneven nature

of mid-sized occupier activity.

In the 50,001–100,000 sq ft band, despite over twice as many expansions as contractions, the scale of the space released led to a net loss of 119,700 sq ft. The 5,000–10,000 sq ft range, while seeing the highest number of expansion deals (46), also had 35 contractions, resulting in a net loss of 66,800 sq ft.

The most significant impact came from the

20,001–50,000 sq ft bracket, where expansion and contraction deals were relatively balanced (18 versus 16), but the scale of the contractions drove a net loss of 239,400 sq ft, the largest across all size bands. Overall, despite some areas of growth, the combined effect across all categories led to a contraction

of 12% in office space across the Big Five and South East regional markets.

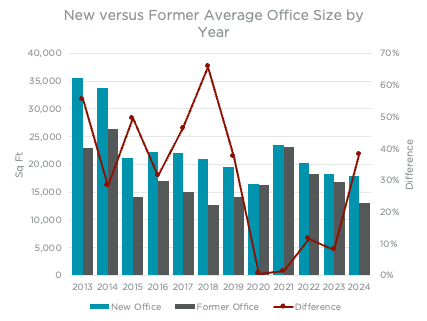

Across the Big Five and South East office markets, most regions experienced net gains in office space, with expansion deals making up�the majority of activity.

Leeds led the way, where 72% of upsizing/downsizing deals were expansions, resulting in a net gain of�101,000 sq ft.

The public sector was responsible for almost half of this net gain, with moves from the National Wealth Fund (previously the UK Infrastructure Bank), the Bank of England, and HM Courts and Tribunal Service accounting for an expansion of 46,100 sq ft combined. None of the five contractions in Leeds amounted to a loss of more than 10,000 sq ft, with Ernst & Young’s contraction into 25,300 sq ft at 12 Wellington Place being the largest.

Excluding activity from alternative sectors, New Entrants to the regional markets accounted for 100,000 sq ft of take-up across 12 transactions during 2024.

Notably, half of these deals took place in Manchester, reinforcing the city’s status as a leading destination and key hub for business expansion. Among the New Entrants were three occupiers from the Retail & Leisure sector—Shein, Levy Merchandising, and VF Corporation—who collectively took up 26,700 sq ft across three deals. Another significant transaction saw communications regulator Ofcom lease 9,400 sq ft at 1 Circle Square, establishing a new digital and technology hub in the city.

The largest deal involving a new market entrant was Glencore Industrial Assets’ relocation from London, securing 19,870 sq ft at One Bell Street in Maidenhead.

NEW�ENTRANTS

WHERE ARE THEY MOVING?

ALTERNATIVE SECTORS�& NEW ENTRANTS

Bristol’s largest expansion involved Frazer Nash taking 41,500 sq ft, which represented a 50% increase in space on their previous lease. On the other hand, DAC Beachcroft’s relocation to 44,200 sq ft at the Welcome Building represents a 49% decrease on their previous space at Portwall Lane.

In stark contrast, the South East stood out as the only region to experience a significant net loss, with a contraction of 793,800 sq ft. This was driven by several significant downsizes, with the five largest transactions�in the regional markets occurring in the South East and resulting in a contraction of 530,600 sq ft combined. Notably, the South East was the only region where contraction deals outnumbered expansions, making up 54% of activity. However, it’s important to acknowledge that the South East comprises a wide range of submarkets, including both central business districts and out-of-town business parks and suburban offices. Many of the larger consolidations and space reductions occurred within the latter, where occupiers are reconfiguring their office footprint in response to shifting workplace strategies and hybrid working patterns.

ALTERNATIVE SECTORS�& NEW ENTRANTS

A key theme shaping the regional office market over the last few years is the continued emergence of the 'less but better' trend. This reflects a growing shift among occupiers towards reduced overall space requirements, while placing greater emphasis on quality.

Rather than simply cutting space, businesses are consolidating into higher-grade, amenity-rich,�and energy-efficient offices that better support collaboration, well-being, and talent attraction�and retention.

The latest data from regional office markets provides strong support for this trend. A significantly higher volume of both expansion and contraction deals occurred within Grade A space (80 and 73 deals respectively), compared to just 34 expansions�and nine contractions in Grade B/C stock.

LESS BUT�BETTER

An evolving investor landscape is reinforcing the focus on best-in-class office buildings across the Big Five and South East regional markets. While allocations remain selective, when high-quality assets do come to market, they continue to attract strong interest and competitive bidding�from both UK and overseas investors.

Looking ahead, capital flows are expected to improve throughout 2025, supported by stabilising pricing and the renewed investor engagement seen at the end of 2024. However, strong occupational fundamentals will remain key to navigating the capital markets in core regional locations. By the end of 2024, prime rents across the Big Five markets had risen by 4.6% annually, with a further 2.6% increase recorded between Q4 2024 and Q1 2025. This upward pressure has been driven by occupier demand for a limited supply of high-quality space, reflected in a Years’ Supply of just 1.12 across�the Big Five and 2.6 in the South East, suggesting�that premium office stock could be quickly absorbed under average levels of take-up.

Competition for the best space is set to intensify further, with a looming ‘development drought’ in the regional markets. As of April 2024, just 2.9 million sq ft of new office space was under construction, nearly 20% of which is already pre-let, with all schemes due to complete before the end of 2026. With no new development currently under way beyond 2026, these supply constraints combined with enduring occupier preferences for quality space, are likely�to continue pushing headline rents upward.

In turn, the income potential from rising rents may prompt developers with planning permission to bring forward new schemes, particularly if inflation stabilises and lower interest rates improve the viability of development finance. On the occupier side, the ongoing scarcity of Grade A space means that in the near term, pre-letting may become increasingly necessary to secure the quality of space occupiers are seeking. However, given that the vast majority of expansions involved forms taking less than 50,000 sq ft — which is a typical minimum threshold to sufficiently de-risk a new office development — it remains to be seen whether requirements will be able to spur schemes into�commencing construction.

SO WHAT?

Excluding activity from alternative sectors, New Entrants to the regional markets accounted for 100,000 sq ft of take-up across 12 transactions during 2024.

Notably, half of these deals took place in Manchester, reinforcing the city’s status as a leading destination and key hub for business expansion. Among the New Entrants were three occupiers from the Retail & Leisure sector—Shein, Levy Merchandising, and VF Corporation—who collectively took up 26,700 sq ft across three deals. Another significant transaction saw communications regulator Ofcom lease 9,400 sq ft at 1 Circle Square, establishing a new digital and technology hub in the city.

The largest deal involving a new market entrant was Glencore Industrial Assets’ relocation from London, securing 19,870 sq ft at One Bell Street in Maidenhead.

NEW�ENTRANTS

ALTERNATIVE SECTORS�& NEW ENTRANTS

Office space activity in 2024�has shown significant variation across sectors, with some industries actively expanding their footprint while others continue to consolidate.

Professional Services was the most active sector in terms of number of deals with — 16 expansions and 15 contractions. Despite the high volume of activity, the sector saw a net loss of 66,600 sq ft, indicating that different firms within the Professional Services umbrella are actively reassessing space needs.

Banking & Finance followed with 29 deals, with�a strong bias toward growth—22 expansions and just seven contractions. This translated into the largest net gain in office space at 88,500 sq ft, signalling renewed confidence and physical office investment in the sector.

The Government & Public sector posted a more modest net gain of 22,500 sq ft, driven by 10 expansion deals against eight contractions. On the contraction front, both National Highways and the NHS downsized through relocations across two markets each, resulting in a combined net loss of 56,400 sq ft. Conversely, the government’s Places for Growth programme — which aims to relocate civil service roles to established regional hubs — has driven expansion among branches such as the HM Courts and Tribunals Service in Leeds and the UK Space Agency in the South East. This reflects a broader strategy to stimulate economic activity in regional cities and tap into more diverse local talent pools. While not part of the civil service, several national institutions, including the Bank of England and the National Wealth Fund, have also expanded in regional markets, following a similar rationale.

Conversely, Pharmaceutical & Life Sciences recorded the largest net loss of office space at 222,000 sq ft, with the Johnson & Johnson consolidation in Thames Valley driving much of this loss. Manufacturing & Energy followed, with a net loss of 156,400 sq ft, even though the number of expansion (11) exceeded contractions (nine), suggesting the downsizing deals were of a larger scale. A similar trend was present in the Technology sector, which saw a net loss of 65,100 sq ft despite more expansions (13) than contractions (12). Other notable net contractions included Retail & Leisure (135,600 sq ft) and Insurance (96,200 sq ft), likely reflecting a more relaxed approach to hybrid work strategies.

WHO IS�MOVING?

A strong return to work mandate may also be linked

to this change, with research suggesting that over

three quarters of financial services firms are planning

to increase office attendance over the course of 2025.

It is particularly notable that the Media sector recorded only expansions, with seven deals and no contractions — resulting in a net gain of 63,400 sq ft. This suggests a clear growth trajectory among media occupiers in 2024. Business Services also showed strong expansion, with nine expansions and just one contraction, contributing

a net gain of 62,200 sq ft.

A reduction in space within the existing office location.

CONTRACTION

Research Analyst - National Offices

joshua.woolnough@cushwake.com

Joshua Woolnough

Head of UK�Offices

ben.cullen@cushwake.com

Ben�Cullen

Head of�UK Research

daryl.perry@cushwake.com

DARYL�PERRY

Head of Edinburgh�Office Agency

james.thomson@cushwake.com

James�Thomson

308�OFFICE�TRANSACTIONS

142�TRANSACTIONS�IN SOUTH EAST

EDUCATION &�MEDICAL�OCCUPIERS

FLEXIBLE�WORKSPACE�OPERATORS

NEW�MARKET�ENTRANTS

�� �ESTABLISHED�OCCUPIERS

�EXPANSIONARY ACTIVITY

�CONTRACTIONARY�ACTIVITY

�THE�NET EFFECT

�REGIONAL�VARIATION

�EXPANDING�SECTORS

�CONTRACTING SECTORS

INTO A�GRADE�A SPACE

�LESS�BUT BETTER?

SECONDARY�MARKET�EXPANSION

Cushman & Wakefield (NYSE: CWK) is a leading global commercial real estate services firm for property�owners and occupiers with approximately 52,000 employees in nearly 400 offices and 60 countries.�In 2024, the firm reported revenue of $9.4 billion across its core service lines of Services, Leasing,�Capital markets, and Valuation and other. Built around the belief that Better never settles, the firm�receives numerous industry and business accolades for its award-winning culture.

For additional information, visit www.cushmanwakefield.com.

ABOUT CUSHMAN & WAKEFIELD

The serviced office sector continues to grow in significance within the regional office market, with flexible workplace solutions catering to a wide range of occupier needs. In 2024, flexible workspace operators acquired 468,600 sq ft across 20 transactions—more than tripling the 136,000 sq ft transacted in 2023. Notably, IWG signed a lease for approximately 73,000 sq ft at the £1.3 billion Olympia redevelopment in West London. Further to this, serviced offices continue to play a vital role as a launchpad for smaller businesses and those in transition, providing the flexibility to scale operations—evidenced by 92,000 sq ft of take-up across nine leases from occupiers moving from serviced offices into conventional office space.

Manchester followed closely with a net gain of 93,700 sq ft, driven by 71% of deals being expansions. The BNY Mellon�and ARM deals at 4 Angel Square and No. 1 St Michael's represented the largest upsizes in the regional markets�in 2024, whereas Ford Credit taking up 14,000 sq ft and Virgin Media leasing 45,700 sq ft represented significant�78% and 59% downsizes on their previous leases.

Similarly, Birmingham recorded a positive net change of 50,500 sq ft, with expansions representing 58% of activity. The BBC’s 33,100 sq ft expansion into 84,000 sq ft Typhoo Wharf represented the largest expansion in Birmingham, with National Highways’ relocation to Three Snowhill being the largest contraction at 13,300 sq ft.

Edinburgh and Bristol saw more modest net gains at 15,800 sq ft and 1,400 sq ft respectively, though expansion still outweighed contraction in both accounting for 63% of�deals in Edinburgh and a region-leading 75% in Bristol. In Edinburgh, Heineken’s consolidation of two office spaces into 43,100 sq ft at 6 St Andrew Square was the market’s largest contraction at 43,900 sq ft, whereas Royal London’s opening of an additional office at Waverley Gate represented the largest expansion at 24,900 sq ft.

EXPANDERS & CONTRACTORS�BY REGION

This suggests that even as occupiers adjust their footprints, they are overwhelmingly doing so within the upper tiers of the market by either expanding selectively or upgrading through relocation.

In terms of square footage, Grade A offices saw over 702,900 sq ft of expansion activity, but this was offset by a larger volume of contraction (1.39 million sq ft), resulting in a net reduction of 691,600 sq ft. This supports the idea that while many occupiers are reducing space, they are often doing so as part of a strategic shift toward better-quality, smaller footprints. Meanwhile, Grade B/C space showed a modest net gain of 160,100 sq ft, but given the far lower deal count, this likely reflects isolated requirements rather than a reversal of the broader market shift.

Together, these trends highlight that in the aggregate, occupiers are not just using less space, they are being more intentional about where and how they use it. The flight to quality continues to shape the market, with occupiers favouring fewer but more effective and amenable square feet. However, it is important to acknowledge that the ‘less but better’ trend is not universal; while overall space may be contracting, a greater number of occupiers are expanding into Grade A space than contracting out of it. This highlights not only the enduring appeal of high-quality offices, but also their role in supporting growing business growth and firms with stronger return to office mandates.

Together, these trends highlight that in the aggregate, occupiers are not just using less space, they are being more intentional about where and how they use it. The flight to quality continues to shape the market, with occupiers favouring fewer but more effective and amenable square feet. However, it is important to acknowledge that the ‘less but better’ trend is not universal; while overall space may be contracting, a greater number of occupiers are expanding into Grade A space than contracting out of it. This highlights not only the enduring appeal of high-quality offices, but also their role in supporting growing business growth and firms with stronger return to office mandates.

EXPANDERS & CONTRACTORS�BY GRADE

YEAR'S SUPPLY AND�NET EXPANSION BY MARKET

DEVELOPMENT PIPELINE,�BIG FIVE & SOUTH EAST

KINDLY PROVIDE IMAGE

KINDLY PROVIDE IMAGE

KINDLY PROVIDE IMAGE

KINDLY PROVIDE IMAGE

KINDLY PROVIDE IMAGE

A strong return to work mandate may also be linked to this change, with research suggesting that over three quarters of financial services firms are planning to increase office attendance over the course of 2025.

It is particularly notable that the Media sector recorded only expansions, with seven deals and no contractions — resulting in a net gain of 63,400 sq ft. This suggests a clear growth trajectory among media occupiers in 2024. Business Services also showed strong expansion, with nine expansions and just one contraction, contributing a net gain of 62,200 sq ft.

LOCAL LOYALTY

Across 294 deals, the average occupier moved just 0.7 miles from their former�to new office.

2024 recorded the lowest average distance travelled by occupiers on record.

MAP_1 SAMPLE FOR PLACEMENT ONLY

CENTRAL LONDON MARKETS

We can also see how the trend played�out across markets, with the Wider City�in particular achieving a high degree of loyalty amongst its occupiers.

KEY THEMES

MAP_1 SAMPLE FOR PLACEMENT ONLY

MOVERS FROM THE WIDER CITY�PRIMARILY STAYED IN THEIR MARKET

We can also see how the trend played out across markets, with the Wider City in particular achieving�a high degree of loyalty amongst its occupiers.

The arrows on the map show were Wider City movers relocated from and to in 2024.

The vast majority stayed local, with 94% of Wider City relocators remaining within the market – the highest proportion on record. Just 12 occupiers moved from the Wider City into the West End, with no moves recorded into East London.

The shorter distance moved reflects the focus on core, central locations that occupiers have shown over 2024 and in the last few years with these areas reporting�a high share of overall deals and a high number of stayers.

ALL 294 MOVERS

180 OCCUPIERS MOVED

UNDER 0.5 MILES

5.9 MOVED 0.5 TO 1 MILE

55 MOVED OVER 1 MILE

This was the most on record for this distance bracket, significantly ahead�of the 143 10-year average.

180 occupiers moved under 0.5 miles – equivalent to the distance from London Bridge to Tower Bridge.

A further 59 moved between 0.5 and 1 mile,�in line with the average.

This was the second lowest figure�on record, behind only 2020.

Finally, just 55 occupiers moved more than 1 mile�in 2024.

MAP_1 SAMPLE FOR PLACEMENT ONLY

MOVERS FROM THE WEST END

There were 24 movers from the West End into the Wider City, continuing the long-term migration trend across the two markets with 12 cross-market migrations on net – albeit at a significantly slower rate than the 19 West to Wider City movers averaged over the last 10 years. No moves were recorded to East London from the West End in 2024.

Looking ahead, supply shortages in core West End markets may drive a higher degree of migration across markets – and further rental growth for the remaining spaces.

In the West End, occupiers also reported�a high degree of loyalty to their existing market. Of 2024 movers previously located in the West End, 79% moved to another market. This is above the 73% averaged over the last 10 years.

MAP_1 SAMPLE FOR PLACEMENT ONLY

CENTRAL LONDON SUBMARKET

This can be shown through sector ellipses, which encompass two thirds of the transactions that occurred within their respective sector in 2024.

These are calculated by mapping one standard deviation around the geographic mean of the deals within each sector.

Not all sectors moved in the same way, however. Some were more footloose than others, while some remained highly location sensitive.

MAP_1 SAMPLE FOR PLACEMENT ONLY

SECTOR ELLIPSES

Banking & Finance is also specific in location, concentrating on core West End areas.

The Insurance and Legal sectors are the most locationally sensitive, confining themselves to the City Core primarily with the Insurance sector particularly focused on the tower cluster.

Represents one standard deviation around the geographic mean of each sector, encompassing approximately two thirds of transactions.

MAP_1 SAMPLE FOR PLACEMENT ONLY

Media, Retail & Leisure, Manufacturing & Energy and Media are all broadly spread across Central London,�from the West End into the Wider City.

Professional Services firms are more distributed but remain focused on central locations in particular.

SECTOR ELLIPSES

Represents one standard deviation around the geographic mean of each sector, encompassing approximately�two thirds of transactions.

MAP_1 SAMPLE FOR PLACEMENT ONLY

SECTOR ELLIPSES

Represents one standard deviation around the geographic mean of each sector, encompassing approximately two thirds of transactions.

Government & Public Sector is the most footloose, spanning from the West End into Canary Wharf and Stratford. This reflects the broad range of occupiers within this grouping, as well as their more price-sensitive requirements.

The Technology sector also has a wide base, pushing further north into the tech clusters of King's Cross and Shoreditch.

MORE AND BETTER

LOCAL LOYALTY

FOCUS ON THE CORE