A Cushman & Wakefield publication

MARKETBEAT PORTUGAL

WE DIDN'T COME THIS FAR, JUST TO COME THIS FAR.

SPRING, 2025

01

ECONOMY

02

OFFICES

03

RETAIL

04

INDUSTRIAL & LogIsticS

05

HOSPITALITY

07

DEVELOPMENT

08

INVESTMENT

09

SUSTAINABILITY

06

LIVING

CONTENT

EconOmic INDICATORS 2024

According to Moody's Analytics, the Portuguese economy slowed in 2024, with GDP growing by 1.8% (after a 2.5% increase in 2023), remaining one of the best performers in the eurozone.

GDP

PRIVATE CONSUMPTION

EXPORTS

INFLATION

UNEMPLOYMENT RATE

+1.8%

+1.4%

+2.4%

+2.8%

+4.0%

6.4%

Global uncertainty continues to cast a shadow over investment, with a slight recovery recorded compared to the previous year (1.4%). Inflation continued to ease gradually throughout last year, falling to 2.4%, after reaching 4.4% in 2023. In the labour market, after its upward trend in 2023, the unemployment rate in Portugal continued its steady fall, reaching 6.4% at the end of 2024.

Additionally, according to data released by the Ministry of Finance last year, the public accounts showed a surplus of €354.1 million, well above the forecasts that pointed to a deficit of €1,495 million. These indicators suggest that the budget balance (in national accounts) may have stood at around 1%. Against the background of reduced interest rates, private consumption was fuelled by the increase in household purchasing power, rising by 2.8% last year. External demand continues to be a key economic driver, with exports increasing by 4.0%, predominantly supported by the continued recovery in the tourism sector.

Source: Moody’s (February 2025)

EconOmic FORECAST 2025/2026

For the next two years, GDP growth of 2.0% is foreseen for 2025, followed by a slowdown to 1.4% in 2026; nonetheless, it is still set to outperform the eurozone average.

+2.0%/ +1.4%

Moody’s Analytics predicts that the European Central Bank will continue to reduce benchmark interest rates, expecting them to reach neutral levels by mid-2025.In line with projections for the eurozone, a moderate drop in inflation is expected, reaching the 2% target in 2025 and dropping to 1.2% in 2026. Unemployment is forecast to continue to fall, reaching 5.9% in 2025 and 5.4% in 2026 – a 25-year record low.

Exports are expected to pick up pace in the short term as companies bring forward orders, envisaging potential additional tariffs, followed by a slowdown in 2026. Although exports may face some challenges, domestic demand is expected to continue driving the economy in 2025 and 2026.

-0.2%/ +1.6%

+2.0%/ +1.2%

+1.5%/ +0.4%

+4.9%/ +2.8%

5.9%/ 5.4%

GREATER LISBON

TAKE-UP

New Completions

Average Deal Size

Under Construction

Vacancy Rate

221,900 sq.m (+97%)

1,270 sq.m (+71%)

7.4% (+0.2 p.p.)

104,200 sq.m

212,300 sq.m

The Greater Lisbon office market experienced a significant recovery in 2024, with 221,900 sq.m of take-up. This represents a year-on-year increase of 97% - the second highest in the last decade. This positive trend is primarily due to the completion of several large-scale transactions, including seven deals of over 5,000 sq.m, accounting for 42% of the total take-up during the period.

Source: Cushman & Wakefield; LPI

TAKE-UP BY SEMESTER AND AVERAGE DEAL SIZE

Amongst the largest deals of the year are two transactions in buildings still under construction in Parque das Nações (zone 5): the purchase of WellBe (26,710 sq.m) by Caixa Geral de Depósitos, to house its future headquarters; and the lease of roughly half of Oriente Green Campus (15,840 sq.m) by the European University. The entire 17,020 sq.m of Álvaro Pais 2, fully occupied by Banco de Portugal, stands out in the New Office Areas (zone 3). The first two zones boasted more than half of the annual take-up, with the Financial Services sector representing more than a fifth of the demand, driven by the largest deal recorded in 2024.

MAIN TRANSACTIONS

TENANT

Caixa Geral de Depósitos

Banco de Portugal

Universidade Europeia

Confidential

Deloitte

SIBS

Leroy Merlin

Monday by Urbania

Ayvens

WellBe

Oriente Green Campus

Álvaro Pais 2

Báltico

Rato, 11

Alfrapark – E

World Trade Center - Block 1

Marquês de Pombal, 2

Malhoa 17

Quinta da Fonte - Q43 (Fernão Magalhães)

PROJECT

5

3

2

6

1

ZONE

26,710

15,840

17,010

6,320

5,820

5,630

4,880

3,850

3,820

3,780

AREA (sq.m)

Development activity remains solid, promoting the emergence of new high-quality spaces that meet the needs of current demand. A total of 104,200 sq.m of new space was completed throughout the year, marking the second-largest volume of the last decade. Of this total, only 23% remains available for occupancy. The influx of supply, mainly due to year-end completions, led to a slight increase in the vacancy rate by 0.2 percentage points (p.p.), which reached 7.4% by the end of 2024. Future supply for the next three years remains sizable, totalling 361,500 sq.m. Most of this area (212,300 sq.m) is under construction, and half has already guaranteed occupancy.

MAIN NEW COMPLETIONS

VACANCY RATE BY ZONE

Exeo Office Campus - Echo

Exeo Office Campus - Aura

EDP 2 Headquarters

Taguspark - Novo Banco (expansion)

4

CONSTRUCTION TYPE

Refurbishmen

New

DEVELOPER

Norfin (Orion)

Avenue

EDP

Taguspark

41,100

16,800

21,500

11,400

8,200

MAIN PROJECTS UNDER CONSTRUCTION

Source: Cushman & Wakefield

Fidelidade - Álvaro Pais

Oeiras city hall - Paços do Concelho

República 5

Campo Novo - building 1

Cais 5

Rato 11

Torres Colombo - North tower

Camilo Castelo Branco, 43

José Malhoa, 12

Refurbishment

Fidelidade

Atenor

Oeiras City Hall

Signal Capital / Sonae Sierra

Norfin (King Street)

Square Asset Management (Signal Capital)

Sonae Sierra / AXA IM

French Family Office

BPI Gestão de Ativos

FS Capital (AM Alpha)

38,400

26,700

30,500

11,200

9,500

5,900

35,100

5,800

9,400

4,900

EXPECTED COMPLETION DATE

2025

2026

AVERAGE AND PRIME RENTS

Heightened demand for top-grade buildings has driven up new increases in prime rents in some areas of Lisbon. The largest increase in headline rents, compared to 2023, was seen in the Secondary Office Zones (zone 4), where an increase of €2/sq.m/month was recorded. Prime CBD (zone 1) and Parque das Nações (zone 5) followed suit, both showing an increase of €1.5/sq.m/month.

GREATER LISBON: PRIME RENTS

GREATER PORTO

76,600 sq.m (+53%)

1,020 sq.m (+31%)

8.9% (+0.4 p.p.)

45,900 sq.m

102,600 sq.m

Source: Cushman & Wakefield; PPI

The Greater Porto office market maintained a solid performance, with a take-up of 76,600 sq.m throughout 2024, representing a year-on-year increase of 53% and the second-highest volume since this indicator was first measured. A total of 75 deals were completed, the second-highest number observed to date. The two largest deals corresponded to the lease of entire buildings, notably the pre-let of 10,370 sq.m in the Mutual building by Deloitte. This made the CBD Boavista (zone 1) the most sought-after area, representing one third of the total take-up. The second largest deal includes the total occupation of the 5,090 sq.m Pharmacia building in Downtown CBD (zone 2), by an entity who needs to remain confidential for now. The 4,640 sq.m lease in Tecmaia – Plot 4 by Infineon stands out as the third largest deal in this period. TMT's & Utilities, as well as Consulting and Legal sectors, played a relevant role, each representing between 37% and 28% of total take-up, respectively.

Infineon

PwC

Tecmaia – Plot 4

Matosinhos Office Center

Barbosa de Castro

Mutual

Pharmacia

7

8

4,640

3,950

3,360

10,370

5,090

Greater Porto’s vacancy rate increased by 0.4 p.p. standing at 8.9%, mainly driven by the completion of some buildings during the year, a significant part of which is still available. In 2024, 45,900 sq.m of new supply were completed, of which 21% remains unoccupied. Concerning future supply, 181,600 sq.m are expected to be completed over the next three years, of which 102,600 sq.m are under construction, and the occupation of one third is already secured. Development activity remains dynamic, contributing to an increased supply of high-quality spaces in Porto.

Brasília Building - Av. Boavista

Noto Office Center

TecMaia - Plot 4

Violas Ferreira

Padrão Casual

IDS Group

ABB

5,500

7,000

6,200

M-ODU (Matadouro)

Viva Offices

SPARK Matosinhos

Latino Coelho, 85

Fernão de Magalhães, 127 (Magnet)

Joana D'Arc

HOP (former la Vie)

Porto city hall

Osborne+Co / Adriparte

Geo Investimentos

GFH / Sonae Sierra

Castro Group

Quest Capital / Tikehau Capital

12,200

10,400

5,100

18,800

14,500

17,400

4,500

15,000

2027

The shortage of quality supply in Porto has continued to put pressure on prime rental values, resulting in increases in most areas. The most notable rise was in the CBD Boavista (zone 1), where rents increased by €2/sq.m/month.

TRends

Workspaces increasingly focus on employee well-being, with natural light, efficient ventilation, and green and leisure areas. ESG certifications (LEED and BREEAM) remain a fundamental requisite in terms of new leases and renegotiations, underscoring the sector’s commitment to sustainability.

The hybrid work model is reshaping office layouts, with greater emphasis on collaborative areas and shared workstations. Companies are streamlining their office footprint, by minimising unutilised areas and implementing more efficient workplace strategies, such as satellite offices and hot desking.

In both Lisbon and Porto, the supply of modern, top-grade office spaces remains constrained, struggling to keep pace with demand. With no new quality supply expected before 2027/2028, pressure on prime rents will remain, in addition to heightened competition to occupy the most sought-after space.

Demand for flexible spaces and plug & play offices is growing, driven by the need for scalability and lower upfront costs. Companies are also relocating their offices in an effort to entice employees back to the office, creating more appealing and functional hubs.

Long leases with a break clause option are now commonplace: 10-year leases with a break at years 5 or 7. In a market where tenants play an increasingly active role in negotiations, this provides stability and dilutes fit-out costs.

Prioritising well-being and ESG have become key strategic criteria

Flexibility and occupancy efficiency

Increase in flex offices and relocation

More structured lease agreements

Scarcity of quality supply and increase in prime rents

RETAIL SALES INDEX

112 (+4.1%)

In 2024, the retail sector continued its upward trajectory, primarily reflected in the increased supply of retail parks and new openings. Sales volume in the retail sector recorded a year-on-year increase of 4.1%, with the food retail segment growing 4.8%. After two years of slowing down, e-commerce regained momentum, with the percentage of consumers making online purchases growing by 5.0 p.p., compared to 2023. It is estimated that in 2024, B2C e-commerce reached €9.7 billion, a trend set to rise at an average annual rate of 5% until 2027.

Total

105 (+4.8%)

Food Retail

118 (+3.4%)

Non-food Retail

E- COMMERCE

49% (+5.0 p.p)

Consumers who made purchases / orders online

Source: INE; data deflated and adjusted for calendar and seasonal effects; Index base 2021 = 100; YTD

Source: APCC; year-on-year variation for the first half of the year.

Mouse hover to view the notes

Source: INE

+5.4%

Sales

+5.7%

Footfall

Footfall and Sales Index in Shopping Centres

23,400 sq.m

160,400 sq.m

Pipeline

Retail Schemes

Until 2027

In the quarter prior to the survey

Source: IDC

The Portuguese Association of Shopping Centres (APCC) reported historic 2024 results in shopping centres, with the year-on-year sales volume growing by 5.4%, fuelled by the increase in the average rise in sales and the number of visitors, which climbed 5.7%. In terms of the new retail supply, the retail park format was again dominant. Four new projects were completed in 2024, totalling 23,400 sq.m of GLA. Most noteworthy is the Penafiel Retail Park, with 8,800 sq.m. The pipeline for the next three years estimates that an additional 160,400 sq.m of GLA will enter the market, 40% of which is under construction. Developers continue to prefer this format, with retail parks commanding 89% of the new future supply.

SUPPLY OF RETAIL SCHEMES

RETAIL SCHEMES

Source: Cushman & Wakefield * Pipeline

NEW OPENINGS

According to Cushman & Wakefield’s proprietary transactions database, 2024 saw 880 new openings, a significant year-on-year increase of 27%. High street retail strengthened its leading position, representing 70% of all new openings, followed by shopping centres with 14%. The Food & Beverage (F&B) sector remained popular with 51% of the new units, while the “Others” sector accounted for 18%. Amongst the most active retailers, the low-cost non-food retailer Normal stood out, with 14 openings throughout the year. In the food sector, the German retailer Lidl led the way with 13 new openings and continued investing in modernising its network, completing four refurbishments in 2024. The Spanish food retailer Mercadona also maintained a strong pace of growth, opening 11 supermarkets and closing the year with 60 operational units. Furthermore, the Sonae Group brands ZU (pet products) and Wells (cosmetics) each accounted for close to a dozen new units, further reinforcing their market presence.

880 (+27)

New Openings

70%

High Street Retail

51%

F&B

Non-random sample of retail demand aggregated by Cushman & Wakefield based on public sources and targeted fieldwork.

DEMAND

Others

Food

Leisure & Culture

Fashion

BY FORMAT

2024

2023

BY SECTOR OF ACTIVITY

Throughout 2024, the city of Lisbon benefitted from 36% of all new openings in Portugal, predominantly in the high street. The areas of Avenidas Novas and Cais do Sodré/Santos stand out, each with 40 and 20 new openings, respectively, mostly in F&B. This sector remained the most sought-after in the capital, representing 61% of all new units. Among the most noteworthy openings was Zara’s new 5,000 sq.m flagship store in Rossio, the second largest in the world. This project underlines the dynamism and enhanced appeal of this emblematic area of the capital.

320 (+16%)

93%

61%

LisboN

The city of Porto commanded the second-highest number of openings in the country, representing 17% of the openings nationwide. Like the capital, most new openings occurred in the high street, with the Baixa area attracting around one third of the new supply. Key milestones included the opening of the Time Out Market Porto, in the southern wing of São Bento station, with 16 spaces; and the Bonjardim project, with 10 new units. F&B remained the most prominent sector, especially for international and chain culinary concepts. 2024 boasted several new openings, including Asian cuisine units, many featuring distinctive interior design, as well as the arrival of Imanol (Basque cuisine), the expansion of Starbucks with two new units and the opening of the second Honest Greens restaurant.

150 (+17%)

86%

69%

Porto

The backdrop of a supply shortage and heightened demand contributed to an upward shift of rents, reaching historic highs, with rent increasing by €10/sq.m/month in Chiado and Avenida da Liberdade (Lisbon) and by €5/sq.m/month in Baixa (Porto). In shopping centres, prime rents have risen by €12.5/sq.m/month, and in retail parks by €0.75/sq.m/month.

PRIME RENTS

FORMAT

Shopping Centres

Retail Parks

Lisbon - Av. Liberdade

PORtugal

Lisbon - Chiado

Lisbon - Downtown

LOCATION

€ 115.0

€ 13.0

€ 135.0

€ 120.0

PRIME RENTS (€/SQ.M/MONTH)

Porto - Clérigos

Porto - Downtown

Porto - Av. Aliados

€ 45.0

€ 82.5

€ 55.0

TRENDS

Location remains the key factor in the expansion strategy of brands. Brands are more willing to commit to greater investment in order to secure the best possible locations, inevitably contributing to higher rents. City centres, with a dynamic tourism and business focus, are the most sought-after areas for the strategic expansion of international brands.

Brands increasingly invest in a circular economy, promoting eco-friendly and waste-reducing practices. Consumers identify with brands that follow an ethical, environmentally and socially conscious and sustainable business model. Major brands are progressively integrating social responsibility into their strategy to improve customer engagement.

Operational improvement and increased profitability through cost reduction and more efficient stock management. Greater alignment and integration between the digital and physical experiences, as brands are more selective in choosing their locations.

Flagship units investing in service automation

A fusion of sportswear and leisurewear, focusing on fashion, comfort and well-being. A concept growing globally and gaining prominence in the fashion industry, with brands increasingly diversifying their offering to align with this trend.

The expansion of Athleisure brands

BRANDS WITH PURPOSE

circularity, sustainability, and social responsibility

INDUSTRIAL & LOGISTICS

Throughout 2024, foreign trade activity led to a slight widening of the trade balance deficit, driven by a 2% and 3% increase in exports and imports, respectively.

IMPORTS

Lease / Sale

€95.8 billion

9,000 sq.m

793,400 sq.m

€73.9 billion

88%

(+2%)

(+3%)

(+85%)

(+34%)

International Trade of Goods

4.2%

€3.1 million sq.m

STOCK

Greater Lisbon Logistics Market

Source: INE; Cushman & Wakefield; IPI

Source: INE; excluding fuel and lubricants

After a two-year slowdown, following the historical high in 2021, industrial & logistics take-up again reached a new record in 2024, with 793,400 sq.m transacted, reflecting a year-on-year increase of 85%. This growth was driven by large-scale transactions, with the top five representing more than a third of the total take-up. This emphasises companies’ drive to concentrate operations in higher-quality and more efficient warehouses. Amongst the most prominent deals are the pre-lease of 119,000 sq.m, in the new phases of the Lisbon North Logistics Platform project. This is followed by the future occupation of the industrial unit by Coloplast in Felgueiras, set to be the Danish multinational’s largest unit; and the leases to Torrestir and CTT, totalling 73,000 sq.m, in the newly opened Benavente Logistic Park. Invicta Park (Vila do Conde) attracted the highest number of deals, with four leases totalling 25,000 sq.m.

In terms of the geographical distribution of demand, Greater Lisbon remains the most popular with half of the total take-up. Greater Porto followed suit with 25% and the northern region with 13%. Additionally, speculative development remained dominant, representing 88% of the total, as opposed to build-to-suit projects.

9

Reflects the new areas used within the scope of IPI, whose correspondence can be found on the rent map. Additionally, zones 17: Remaining North, 18: Remaining Center, and 19: Remaining South are included.

Torrestir

CTT

Coloplast Manufacturing

Continental Mabor

Benavente Logistics Park

Continental

Merlin Lisboa Park – Lisbon North Logistics Platform

Felgueiras Factory

Greater Lisbon

Greater Porto

North

REGION

14

17

43,500

29,500

22,900

119,000

56,000

COVERED AREA (sq.m)

Atlantic-Cargo

Testo Portugal

Logistics Center - Setúbal

Quinta da Marquesa IV

Panattoni Park Lisboa-Santarém

Albergaria-a-Velha Industrial Zone

Vendas Novas Industrial Park

Alentejo

Centre

18

19

20,000

19,000

17,000

22,700

The vacancy rate in the Greater Lisbon logistics market stood at 4.2%, underlining the scarcity of quality supply, thereby driving the development of new projects, many of which on a speculative basis. During 2024, 396,200 sq.m of new logistics spaces were completed, more than two thirds of which in Greater Lisbon, with an occupancy rate of 89%. Among these projects are the Castanheira do Ribatejo Logistics Platform, developed by Montepino, and the Benavente Logistics Park, developed in partnership between Invesco and Magna General Contractors. Furthermore, 309,100 sq.m of logistics space is currently under construction in Portugal, of which two thirds have already secured occupancy, mainly in Greater Lisbon (143,100 sq.m) and Alentejo (80,000 sq.m). Noteworthy projects include the Panattoni Park Valongo, Lidl’s future Logistics Warehouse in Loures, and the second phase of Mercadona's Almeirim Logistics Platform, developed by Garcia Garcia.

Almeirim Logistics Platform (Mercadona) - Phase I

VGP Park Montijo

Castanheira do Ribatejo Logistics Platform - Plot 1

Ermida Park

RIBATEJO

Greater PORTO

Garcia Garcia

VGP

Logicor

Montepino

Invesco / Magna General Contractors

50,600

31,400

30,600

105,500

90,700

Almeirim Logistics Platform – (Mercadona) – Phase II

Lisbon North Logistics Platform – Phase II

Panattoni Park Valongo

Loures Logistics Warehouse

Ribatejo

Merlin Properties

Panattoni

Lidl

47,000

33,000

75,000

54,000

URBAN LOGISTICS

(LAST MILE)

€7-8/sq.m/month

Increased market activity, particularly in high-quality projects, has resulted in a general rise in prime rents. In Greater Lisbon, rents in Castanheira - Azambuja (zone 1) rose to €5.20/sq.m/month, while in Greater Porto, in Port of Leixões – Airport area (zone 10), values reached €5.75/sq.m/month. Meanwhile, the urban logistics segment in Lisbon and Porto saw an increase of between €0.50 and €1.10/sq.m per month.

€6.1-6.5/sq.m/month

INDUSTRIAL & LOgIsticS

Optimisation of operational costs and greater efficiency

Modern and sustainable spaces at a premium

The growth of Data Centres and Self-Storage

Companies increasingly recognise that upgrading to new logistics spaces is more efficient from an operational viewpoint. Additionally, they consolidate their operations by planning their future space needs to ensure expansion opportunities in the medium/long term.

Globalisation and the pursuit of economies of scale led to manufacturing and stockpiling centring mainly in Asia. The recent supply chain interruptions and stock shortages worldwide, including in Portugal, set off a trend for nearshoring, that is, installing new industries in Europe to meet local and regional needs. Demand for warehousing, as well as industrial units, from companies in the renewable energy sector, has also risen.

Much of the current stock is “dated” and occupiers as well as investors are primarily interested in modern properties with sustainability credentials. Heightened focus on larger assets, which are more functional and include amenities to enhance employee retention and meet ESG criteria. For logistics operators, more sustainable warehouses can attract new accounts and retain customers.

The self-storage sector still has a lot of potential to grow throughout the country with older buildings being adapted for this purpose. Concerning data centres (currently also known as logistics and data computing), Portugal has caught the attention of the biggest data centre operators, as it is perceived as a safe country, with sufficient availability of power, and benefiting from its connectivity to intercontinental submarine cables which land in Portugal.

Nearshoring fuelling demand

Tourism activity in Portugal maintained a positive trend throughout 2024, with widespread growth across all the main indicators, and despite a slowdown in growth rates, the year delivered all-time highs. Over the past year, the number of guests and overnight stays presented year-on-year increases of 5% and 4%, respectively. International demand continued to play a determining role, representing more than 70% of overnight stays, with a particular emphasis on long-distance markets, namely the North American market, which recorded the highest year-on-year increase (+13%) amongst the top five source markets. A year-on-year rise in overnight stays was seen across the country, most notably in the Azores (+8%), the Centre region (+7%), and the northern and West and Tagus Valley regions (+6% each). The Algarve and Madeira recorded more moderate increases (+1% and +2%, respectively). These results demonstrate greater regional diversification, with visitors exploring new areas of the Portuguese territory.

TOURISTS

Overnight Stays

REVPAR

Total Revenues

Occupancy Rate

25.0 million

65.1 million

€5,780 million

€77.7

66.4%

(+5%)

(+4%)

(+11%)

(+8%)

(+1 p.p.)

YTD July

11

Em estabelecimentos de alojamento turístico

TOURISM INDICATORS

Source: INE; Turismo de Portugal

PIPELINE BY REGION

Hotel revenues continued to boast a solid performance with total revenues 11% higher than the same period in 2023.

OVERNIGHT STAYS AND REVPAR BY REGION

10

The RevPAR (Revenue per Available Room) rose by 8%, reaching €77.7, and the occupancy rate (per room) stood at 66.4%, reflecting a year-on-year increase of 1 p.p.

By region, the most significant increases in RevPAR were experienced in the islands, Madeira and the Azores, with 15% and 13%, respectively. The Short-Term Rental segment accounted for 12.1 million overnight stays and 5.1 million guests throughout 2024, a year-on-year increase of 6% in both indicators. Total revenue grew by 12%, reaching €624 million, with RevPAR maintaining an uptrend and rising by 3% to €43.7.

Center

West and Tagus Valey

Setúbal Península

Algarve

Açores

Madeira

NEW SUPPLY

During 2024, around 60 new hotels opened, providing 3,630 new keys. Whilst most projects were 4-star hotels (41%), 25% of the new hotels fall under the 3-star category, reflecting a diversification of supply to meet different demand profiles. Lisbon and Porto remained the principal growth hubs, with 25 of the new units, totalling 1,580 keys. Amongst the most notable openings are some 3-star units, such as the Locke de Santa Joana (Lisbon, 370 keys), the B&B Hotel Porto Gaia (Vila Nova de Gaia, 210 keys), and the Icon Apartments (Porto, 170 keys). In terms of future supply, more than 100 new projects are planned, which will add 10,370 rooms to the market by 2027. This expansion reinforces the commitment to upscaling the hospitality sector, with a strong focus on 4- and 5-star hotels, representing 41% and 42% of the projects, respectively, concentrated in the metropolitan areas of Lisbon and Porto.

MAIN OPENINGS

+60

Hotels Opened in 2024

+3,630

New Keys

Source: Cushman & Wakefield; Turismo de Portugal (RNET)

HOTEL

Icon Apartments

Ibis Styles Lisboa Aeroporto

Locke de Santa Joana

B&B Hotel Porto Gaia

Hotel Quinta da Ombria

Nôma

Accor Hotels

Viceroy Hotels & Resorts

Locke

B&B Hotels

OPERATOR

Loures

Loulé

Lisbon

Vila Nova de Gaia

CITY

3 STARS

4 STARS

5 STARS

3 stars

CATEGORY

170

160

140

370

210

B&B Hotel Viana do Castelo

Holiday Inn Braga

Cénica Porto Hotel

B&B Hotel Leiria Fátima

INNSiDE Braga Centro

IHG Hotels & Resorts

Hoti Hotéis / Meliã Hotels & Resorts

Curio Collection by Hilton

Viana do Castelo

Braga

Leiria

120

110

130

KEYS

In 2024, tourism in Lisbon maintained its upward trajectory. Humberto Delgado Airport saw an increase of 4% in the number of arrivals compared to the previous year. Cruise tourism experienced a slight increase of 1%, due to the increase in transit tourism, despite a decline in the volume of embarkations and disembarkations. During this period, Lisbon recorded 12.8 million overnight stays, a year-on-year increase of 5%. Nonetheless, the capital’s operational indicators reflected mixed results, with an increase in RevPAR reaching €117.8, but a slight decrease in the occupancy rate, which fell to 73.7%.

17.6 million

12.8 million

73.7%

€117.8

In terms of new supply, there were 13 new hotel openings in 2024, providing 1,000 more keys, predominantly 3-star units. By 2027, around 30 more hotels with 2,900 keys are expected to be added to the city’s supply. Luxury hotels continue attracting interest, with over half of these keys in 5-star units. Prominent examples include the Meliá Lisboa (5 stars, 240 keys) and the Moxy Alfragide Lisbon (3 stars, 220 keys).

AIRPORTS

CRUISE TERMINALS

Tourist Arrivals

(-0,3 p.p.)

(+6,4%)

764 thousand

(+1%)

Overnight stays, occupancy rate and RevPAR refer to hotel establishments

LISBON

Source: INE; APL

8.0 million

4.9 million

67.7%

€86.7

There were 15 hotel openings throughout the year, totaling 780 keys, primarily 3-star units. Ten new hotels, largely 4-star units (44%), with 640 keys, are expected to be completed in the next three years, including the B&B Hotel Madalena (3 stars,180 keys) and the Aliados Plaza Hotel & SPA (4 stars,100 keys).

TOURIST ARRIVALS

(=)

(+4.5%)

196 thousand

(+32%)

PORTO

During 2024, tourism in the Porto region continued to follow a positive trend. Francisco Sá Carneiro Airport recorded a 5% increase in traffic, while in the cruise segment, Port of Leixões boasted a 32% increase, setting a new record. The number of overnight stays in tourist accommodation in the region increased 8%, totaling €4.9 million, with RevPAR adjusting to €86.7 while the occupancy rate remained stable at 67.7%.

12

Internationalisation of supply

Exposure to new markets

Capital allocation / Investment in hospitality

Diversification and upscaling of hotel supply targeted at demand with a high purchasing power. Growth of new accommodation concepts, combining short, medium, and long-term stays. Increased competitiveness of new tourist destinations, supported by nature, gastronomy, and cultural packages.

Consistent growth in the North American market, with an increase in the market share in terms of overnight stays and the contribution to tourism revenues. Sustained exposure to the Asian markets, with greater growth potential than nearby markets.

More investment activity committed to the hospitality industry. Operating platform deals and opportunities for portfolio sales. More core+ capital available for acquisitions. Investors appear willing to pay premiums for projects aligned with ESG policies.

NR. OF UNITS SOLD

Average Absorption Time

AVERAGE PRICE

Average Discount and Adjustment Rate

NEW

2,260

(+12%)

TOTAL

9,520

(+13%)

€6,860/sq.m

(-1%)

€4,790 sq.m

(-3%)

-4%

-8%

15 months

7 months

1,530

(-6%)

5,680

(+17%)

€4,200/sq.m

€3,310 sq.m

-7%

9 months

6 months

13

New and used

SALE OF APARTMENTS

Source: SIR Ci

RESIDENTIAL PROJECTS LICENSING

In the context of falling interest rates and the consequent increases in spending power, 2024 saw a rise in buying and selling activity in the residential market. According to information from the Residential Information System/Confidencial Imobiliário (SIR Ci), 2024 recorded a 10% increase in the number of apartments sold in Portugal, to 94,200 units, with the average price rising by 5%, reaching €2,800/sq.m, when compared to the previous year. The imbalance between supply and demand, especially due to the scarcity of new developments targeted at the mid-end housing segment, was one of the key factors pushing up sales prices. Throughout 2024, a total of €24.9 billion in mortgage lending was granted to individuals, according to the Bank of Portugal, reaching an all-time high for the past two decades. A survey of the banks, carried out by the Portuguese Central Bank showed an increase in demand for credit by individuals over the past year, particularly in the residential segment.

15

Percentages correspond to the year-on-year variation of the indicators

Bank of Portugal Credit Market Survey (publications from January 2025 in relation to the previous quarter)

sale of apartments

Source: Pipeline Imobiliário Ci

SALES PRICE OF APARTAMENTS

In Lisbon, the average sales price of apartments (both new and used) recorded a year-on-year decline of 3% to €4,790/sq.m, falling slightly lower for new properties (-1%). For both new and used properties, the Historical Centre remained the most sought-after, reaching average sales prices of €5,830/sq.m, followed by the Traditional zone (€5,640/sq.m). The most significant downward adjustment occurred in Parque das Nações (-18%), dropping to €5,170/sq.m. The average discount and adjustment rate increased to 8%, with the average take-up time falling to seven months. In terms of future supply, Lisbon experienced a considerable drop in the volume of licensed residential projects (-21%) and an 14% increase in projects submitted for licensing.

PRICE OF APARTMENTS

16

21

Source: Cushman & Wakefield; SIR Ci

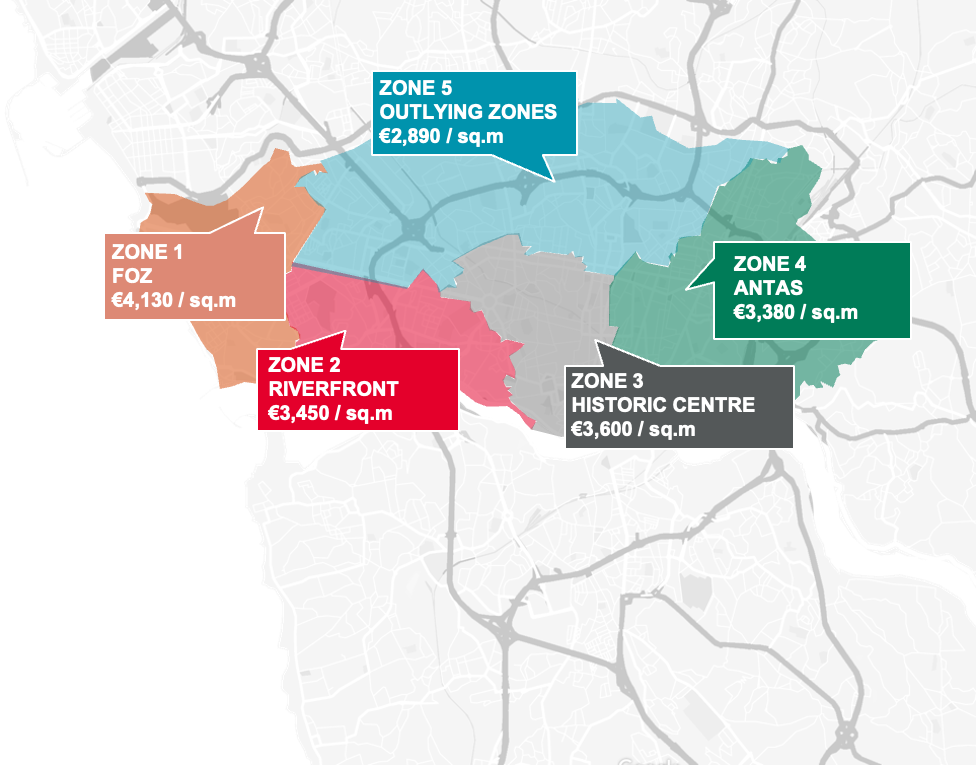

In Porto, the sales price of apartments saw an increase of 2%, to €3,310/sq.m, while on the contrary, new units saw a year-on-year decline of 3%. Foz continued to command the highest prices, reaching €4,130/sq.m, whereas Ribeirinha saw the most significant year-on-year decrease (-9%), dropping to €3,450/sq.m. The average discount and adjustment rate stabilised at 7%, with the average take-up time decreasing to six months. In terms of future supply, Porto recorded a sizable increase in the volume of licensed projects (+50%) as well as in projects submitted for licensing (+17%).

NR. LEASED UNITS

Average Monthly Contracted Rent

230

(+41%)

2,880

(+9%)

NOVO

€24.4/sq.m

€19.1/sq.m

-6%

3 months

(-5%)

500

(-4%)

€17.9/sq.m

(-7%)

€15.4/sq.m

-5%

4 months

RENTAL MARKET

In 2024, the disparity between supply and demand persisted in the private rented sector (PRS), according to SIR Ci. Unlike the built-to-sell market, this contributed to a slight decrease of 1% in the number of apartments rented nationwide, totalling 8,980 apartments. This decline was associated with a marked increase of 6% in the average rent, to €15/sq.m/month. Although the shortage of supply continues to generate interest among some developers in developing built-to-rent projects, their limited financial viability and lack of confidence in the legal framework have led to the majority of future projects in this segment being public initiatives.

In Lisbon, average rents remained at €19.1/sq.m with a slight decrease of 1% for new properties, falling to €24.4/sq.m/month. The Historic Centre maintained its lead, remaining stable compared to the previous period. In Porto, the average rental price rose slightly by 1% to €15.4/sq.m, with new apartments recording a decrease of 7% to €17.9/sq.m/month. Like the built-to-sell market, the area of Foz remains the most popular, and recorded the highest year-on-year rental growth (+13%), despite the reduction of rented properties. The discount and adjustment rates increased in both cities, with the average take-up time falling by one month for new properties in Lisbon and remaining stable in Porto.

RENTAL PRICE OF APARTAMENTS

The student accommodation and CoLiving segments continue to suffer from a lack of supply, especially of purpose-built accommodation. In terms of private sector supply, five new units were completed last year, with a total of 890 new beds, with Ebora Residentes (Évora) standing out with 330 beds and two units from the Odalys Group, the Odalys Asprela (Porto) and the Odalys Belém (Lisboa) with a total of 390 beds. The ratio of beds per student picked up to 15%, with activity by private operators, who now represent close to 40% of the supply, remaining stable.

29,200

15%

40%

Total Supply (nr. of beds)

Private Operators

Provision Rate

(+7%)

Ratio between number of beds and displaced national and international students

Student Accommodation / CoLiving

Next 3 years

Heightened demand continues to attract the private sector and encourage the allocation of public investment to these segments, particularly through the National Plan for Housing in Higher Education (PNAES), funded by the EU Recovery and Resilience Plan (RRP). In this context, the new supply forecast by 2026 currently stands at 10,500 beds. However, some of these projects were initially scheduled for completion in previous years, and have experienced delays. Amongst future private supply, prominent examples include the Alta de Lisboa – Plot 12 project with 640 beds, and Xior Boavista (Porto) project, with an additional supply of 500 beds.

MAIN PRIVATE OPENINGS

MAIN PRIVATE PIPELINE

AMRO Porto

Odalys Belém

Ebora Residences

Odalys Asprela

StudentVille Palma

AMRO Estudiantes

Grupo Odalys

StudentVille

Royal Prime

Évora

150

20

330

270

The Social Hub - Lisbon Carcavelos

The Social Hub – Porto Bonjardim

Alta de Lisboa – Plot 12

Xior Boavista

Milestone Olaias

The Social Hub

Milestone

Smart Studios

University Hub

Cascais

440

400

640

In the senior housing sector, the number of available beds continues to increase, standing at 106,200. However, the rate of new openings has not kept pace with the ageing of the population, and, hence, the equipment ratio has remained stable at 14%. The private sector continues to be driven by high occupancy rates and a lack of quality supply. In 2024, the DomusVi group is worth highlighting with the opening of a 130-bed unit in Leiria, as well as the MomentusSenior Living Residences with a project of 110 beds in Cascais. Looking ahead, over the next three years, another 210 new beds are expected from the main private operators, with two of these in Cascais.

106,200

14%

(+1)

Ratio between the number of beds and population aged 80 and over; 2023 estimated population (Source: INE).

25%

Equipment Rate

Senior Housing

Source: GEP; INE; ACSS

SUPPLY

MAIN PRIVATE OPERATORS’ PIPELINE

MAIN PRIVATE OPERATORS’ OPENINGS

Source: Office for Strategy and Planning – Social Charter (excludes Madeira and Azores)

Residência Assistida Estuário do Douro

DomusVi Santo Agostinho

Momentus Sénior - Cascais

Emeis

DomusVi Group

MomentusSenior Living Residences

Amera Estoril

Lifento Cascais

Amera

Neurostate Home

90

Setúbal Peninsula

Residência Assistida Farol da Guia

Residência Bom Sucesso

100

Pressure on the residential market for the middle-class housing segment persists

Demand for student accommodation or co-living projects will continue to rise

The shortage of senior housing is expected to exacerbate

Continued supply-demand imbalances will fuel rising prices.

Excessive taxation and the inadequate legal framework continue to hinder the development of specific built-to-rent products for the mid-end segment.

Demand for student accommodation and more exclusive co-living concepts from occupiers and investors is expected to maintain its upward trend, with developers looking for larger and more appealing solutions that serve as suitable alternatives to the traditional residential segment. The market is expanding to cities beyond Lisbon and Porto, particularly Braga, Aveiro, Coimbra and Covilhã.

In the context of an ageing population, increased supply still falls a long way short of what is needed, fostering the development of private assisted living homes and offering quality services for the elderly. Nonetheless, the development of this segment could be impacted, on the one hand, by the high monthly rates for the average Portuguese family and, on the other hand, by the difficulty of hiring specialised staff, especially in locations outside large urban centres.

Development of the build-to-rent market remains slow

Development

MAIN URBAN DEVELOPMENT AND REGENERATION DEALS

Amongst the main investment activity in the development and urban regeneration sector in 2024, Millenium BCP’s sale of the Villafundo land in Amadora, and Zume Flat’s purchase of Marconi Parque, both for an estimated price of €30-35 million, are noteworthy.

TYPE

Land

Land & Building

Building

Abanca Plot

Santa Luzia Plot

Marconi Parque

Villafundo Plot

Future Panattoni Park Lisbon-City

ASSET

Amadora

31,700

15,200

221,800

242,000

85,000

€690

€1,380

€150

€130

€300

VALUE (€/sq.m)

€20-25 M

€20-22 M

€30-35 M

€24-27 M

VALUE (M€)

REAL ESTATE PROJECTS UNDER LICENSING

Concerning future supply, last year 10.1 million sq.m were submitted for licensing in mainland Portugal, distributed over approximately 23,800 projects, reflecting a year-on-year growth of 28% and 9%, respectively. Most of the area submitted for licensing is for residential use (67%) and new construction (73%). In terms of the type of construction, the dominance of new development ranged from 75% in retail to 84% in the residential sector.

REAL ESTATE PROJECTS LICENSING

In 2024, the licensing of real estate projects by construction area in Lisbon followed an asymmetric trend when compared to the same period last year, with a significant 81% increase in the area of projects submitted for licensing and a decline in the total area of licensed projects (-35%). Concerning the projects submitted for licensing, despite the prevalence of the residential sector, representing 229,000 sq.m, the tourism sector boasted the highest year-on-year increase (+94%), reaching 105,000 sq.m. These two sectors were both relevant amongst the licensed projects, the residential sector represented almost 60% of the total area with 180,000 sq.m, and the tourism sector saw the largest increase (+97%), reaching 68,000 sq.m. Most of the licensed area (77%) was for refurbishment as opposed to new construction.

651,500 sq.m

(+81%)

284,400 sq.m

(-35%)

LICENSED

Submitted for Licensing

LICENSED REAL ESTATE PROJECTS

Construction costs decreased for new construction, while construction costs for high-end and luxury refurbishment projects increased slightly, with average costs (excluding VAT) in Lisbon, ranging from €1,350/sq.m to more than €2,000/sq.m, for new construction, and between €1,800/sq.m and more than €3,000/sq.m for refurbishment projects.

CONSTRUCTION COSTS BY SEGMENT

High

Average

Luxury

€1 750/sq.m

> €2 000/sq.m

€1 350/sq.m

New Construction

€2 500/sq.m

> €3 000/sq.m

€1 800/sq.m

A total of 403,100 sq.m were licensed in Porto in 2024, a year-on-year increase of 22%. The projects submitted for licensing saw an increase of 23% when compared to the previous year, totalling 433,700 sq.m. In terms of the projects submitted for licensing, the residential sector remained the most popular covering 253,000 sq.m, with the area allocated to the tourism sector commanding an increase of 30%, standing at 62,000 sq.m. Regarding the newly licensed projects, the residential sector remained dominant, corresponding to more than 60% of the total area, with a balance between the area for new development and refurbishment.

433,700 sq.m

(+23%)

403,100 sq.m

(+22%)

LICENSED REAL ESTATE PROJECTS*

Construction costs in Porto rose slightly for the high-end refurbishment segment, with prices (excluding VAT) ranging from €1,250/sq.m to more than €1,900 sq.m for new construction and between €1,550/sq.m and more than €2,500/sq.m for refurbishment projects.

€1 650/sq.m

> €1 900/sq.m

€1 250/sq.m

€2 000/sq.m

> €2 500/sq.m

€1 550/sq.m

The need to promote housing for the mid-end segment will remain a priority. The lack of supply will continue to be affected by high taxation, lack of incentives for new construction and high construction costs.

Shortage of Housing Development

The increasing return to offices and demand for more modern and environmentally and energy efficient offices will fuel development in the office sector and the potential creation of new business centres. Simultaneously, older buildings in more traditional and touristic areas will become available to be converted into housing or other types of accommodation and leisure.

Development of a new cycle of more sustainable, efficient and certified buildings

Growing interest in modular, passive and prefabricated homes is having a significant impact on the sector Efficiency: these types of construction techniques enable homes to be assembled much more quickly and sometimes at slightly lower costs

Modular and prefabricated construction

The adoption of digital and technological solutions in the construction and real estate sector in Portugal is rapidly gaining momentum. Some of the key trends include: Building Information Modelling (BMI): This technology is being increasingly utilised as it facilitates better coordination between architects, engineers and builders, reducing errors and costs. Artificial Intelligence: this is being applied in several areas, ranging from market analysis to the optimisation of construction processes.

Digitalisation and Technology

More affordable land/allotment prices: many developers are opting to channel their efforts into finding out-of-town solutions at more affordable prices and the possibility of offering more reasonably priced options to families. Emergence of satellite cities: new planned developments emerge on the outskirts of large cities, offering urban amenities and a more tranquil environment.

Increase in the value of the surrounding suburbs of large urban centres

Following a period of relative stability in the first half of 2024, commercial real estate investment experienced a dramatic rebound in the second half of the year, with a total volume of €2,380 million, reflecting a year-on-year growth of 39%. In contrast to last year’s trend, large-scale deals saw an uptick. The five most sizable deals represented a third of the total volume invested, with the average deal size rising to €29 million, in more than 80 transactions. Foreign capital continued predominant, representing 73% of the total investment volume, surpassing the average recorded in the last five years. The largest share of this capital came from Europe, with the French and Spanish markets together accounting for half of the foreign volume invested.

TOTAL VOLUME

Foreign Investment

RetaIl

€2,380 million

(+39%)

73%

50%

22

COMMERCIAL REAL ESTATE INVESTMENT

Institutional investment in completed and income-producing real estate properties.

INVESTMENT BY QUARTER

Capital allocation by sector in 2024 strengthened the recovery of the retail sector, which is responsible for half of the total volume invested. The retail segment benefitted from an invested amount of €1.19 billion, boasting the three largest deals of the year. The most notable deal was LeadCrest Capital Partners’ purchase of a 49% stake in the real estate branch of the Os Mosqueteiros Group in Portugal (Athos Portfolio) for €245 million. This was followed by two shopping centre deals: Lighthouse Properties’ purchase of Alegro Montijo from Ceetrus for €178 million and Castellana Properties’ purchase from Harbert of LoureShopping, 8.ª Avenida and RioSul Shopping for a total consideration of €177 million. Hospitality strengthened its presence in the investment market, representing 21% of the total volume, with €500 million invested. This was influenced by three major deals in the 5-star category: Quinta do Lago Group’s purchase of the Conrad Algarve from DK Partners for more than €150 million, Accor Invest’s sale of the Sofitel Lisboa Liberdade to a private French investor for €75 million, and BTG Pactual’s purchase of The Oitavos from the Champalimaud Group for around €70-80 million.

INVESTMENT DISTRIBUTION BY SECTOR

MAIN INVESTIMENT DEALS

Or €/key in hospitality. In case of a range in the “Value (M€)” column, the calculation of this indicator is based on the range’s average value.

Offices corresponded to 14% of the total amount invested, standing at €320 million. The most noteworthy deal was the purchase of K Tower by Real I.S. from Krestlis for approximately €75-80 million. “Other assets” consolidated their position in the market, attracting 11% of the total investment, with increased activity in the Purpose-Built Student Accommodation (PBSA) sector. In this segment, Xior’s purchase of Home & Co Campo Pequeno for €58 million and the purchase of two PBSA units in Lisbon by Stoneshield Capital for between €55-60 million stand out. Finally, the industrial and logistics market continued to be less dynamic and secured a mere 5% of the total amount invested, standing at €110 million, reflecting the lack of supply. Following upward adjustments across all sectors during the last two years, the evolution of prime yields has remained stable throughout the year. By year end, the retail sector stood out for its solid performance, with yields declining by 25 basis points (bp).

23

Alegro Montijo

LoureShopping, 8.ª Avenida & RioSul Shopping

Athos Portfolio

Conrad Algarve

LCN Portfolio 1

Alegro Sintra (50%)

K Tower

Sofitel Lisboa Liberdade

The Oitavos

Barreiro Retail Planet

Montijo

Seixal

Several

Sintra

Barreiro

56,800

74,080

240 Keys

28,820

14,990

160 Keys

140 keys

34,760

Ceetrus

Harbert

Os Mosqueteiros Group

VENDOR

DK Partners

LCN Capital Partners

Nhood

Krestlis

Accor Invest

Champalimaud Group

AM Alpha

Lighthouse Properties

Castellana Properties

LeadCrest Capital Partners

PURCHASER

Quinta do Lago Group

Slate Asset Management

Real I.S.

French Private Investor

BTG Pactual

Redevco

€178 M

€177 M

€245 M

>€150 M

€150 M

€90 M

€75-80 M

€75 M

€70-80 M

>€70 M

€3,130

€2,382

>€635,590

€2,000

€3,120

€5,170

€460,120

€520,830

>€2,010

7.20%

9.00%

6.25-6.75%

YIELD (%)

Hospitality

Retail

Office

SECTOR

OUTLOOK Forecasts for 2025 indicate that the upward trend in commercial real estate investment will continue, indicating an estimated total volume of around €2.56 billion, reflecting a year-on-year growth of 8%. Under this scenario, the decline of prime yields observed in the retail sector at the end of last year could extend to other sectors.

PRIME YIELDS

Local open-ended funds, pension funds, and family offices (involving smaller deals, without recourse to debt) still have a role to play.

Benchmark yields are declining due to lower interest rates. This effect will be especially evident in the most sought-after categories with a consequent increase in value (also supported by specific increases in prime rents for the best-performing assets). New or refurbished assets with excellent ESG credentials are more resilient.

Sluggish growth in the European economy, leading to investor uncertainty over the potential for rental growth. Limited fundraising for investment in Europe, in contrast to the buoyant American economy.

The differential between yields on income-producing real estate and the so-called "risk-free assets" stabilises through subsequent reductions in interest rates; Disparity in price expectations between sellers and buyers narrows.

Gradual recovery in investment activity throughout 2025, as...

While occupational markets remain healthy, investment recovery will be impacted by...

Capital values may increase in the most resilient asset types...

A gradual resurgence of large international investors is expected, but…

With funding available from both traditional lenders and structured finance players.

Healthy debt markets (both for acquisitions and refinancing)

COMMERCIAL REAL ESTATE CERTIFIED BUILDINGS

Sustainability and the integration of Environmental, Social, and Governance (ESG) criteria became firmly established across all sectors in 2024, shaping the decision-making processes of the domestic real estate market. In the Portuguese market, particularly in the banking sector, loan interest rates are already being linked to the sustainability metrics of an investment. In light of the current landscape, there is mounting evidence that tenants and investors are more inclined to pay a green premium for sustainable assets, making the adoption of building certification and compliance with the European Taxonomy unavoidable and an increasingly relevant trend. Additionally, there is a substantial drive towards energy transition, with a strong focus on enhancing the energy efficiency of buildings through refurbishment or repurposing to adhere to the forthcoming legal requirements.

24

New certification or renewal; only includes the projects listed by the respective entities (some projects are anonymous and therefore not published).

Source: BREEAM, LEED and WELL

In terms of the certification of sustainable projects, the number of BREEAM and LEED certified buildings in 2024 was almost triple the total certified during 2023; mostly in the office and retail sectors. Almost all BREEAM certification (90%) was obtained for buildings in use, in contrast to LEED certification, in which new construction/refurbishment dominated. In terms of the WELL certification, which focuses on the use of the building and the well-being of its occupants, in 2024, five certifications were issued in Portugal, all in office buildings, namely the Exeo Office Campus’ Lumnia building and the ALLO building, both located in Lisbon. This sector continues to lead future certification, with approximately 60 projects registered.

25

The current global context presents important challenges and opportunities for sustainability. Promoting a stronger and more independent economy reinforces sustainability insofar as it is necessary to work on energy and resilience issues. In 2025, the real state sector stands at the heart of a transformation driven by stringent regulatory requirements, the new Omnibus Package, recently published and awaiting approval, and a growing demand for sustainable buildings incorporating ESG practices. This shift is fuelled by a convergence of economic, social, and technological drivers that are reshaping how real estate assets are developed, managed, and valued. The focal areas for 2025 remain aligned with those of 2024, with some potential relaxation of regulations so that organisations can take on the ESG management model they consider most appropriate, according to their risk appetite. Below is a summary of our view of the ESG trends in the real estate sector:

Given that investment in real estate is risk-averse, and buildings play a critical role in resilience to the impacts of climate change and in protecting the population, there is a growing concern about assessing these climate risks and in the implementation of mitigation measures to better protect buildings, the activities carried out in them and their users. The devastating extreme weather event in Valencia at the end of October 2024, known as DANA (Isolated High-Level Depression), serves as a stark reminder of the urgency of these measures. Such events, worsened by climate change, underscore the need for resilient, future-proofed buildings. Research concerned with Climate Risk is gaining prominence, particularly under the European Taxonomy, which promotes transparency and accountability in managing environmental risks.

While decarbonisation has long been a priority in the real estate sector as a climate change mitigation strategy, the Energy Performance of Building Directive (EPBD), published in April 2024, sets even more ambitious energy efficiency targets, requiring extensive refurbishment and renovation of existing buildings. The transformation of the existing building stock, delaying its energy obsolescence, and its respective repositioning are unavoidable and will contribute decisively to improving the market positioning of these buildings, increasing their market value.

Decarbonisation and efficiency

Adaptation to climate change

The Corporate Sustainability Reporting Directive (CSRD) has come into force this year, and companies are now required to disclose their non-financial information vis-à-vis sustainability performance, as well as their climate transition strategies. These transition plans must outline the strategies and measures that the relevant funds will implement to mitigate climate risks and comply with evolving environmental regulations. The publication of these plans is essential to foster transparency and accountability in the management of climate risk, enabling investors to access reliable and comparable data, facilitating informed decision-making. The Omnibus package, if approved, will reduce the percentage of companies in-scope and delay their implementation. This initiative is designed to steer investment towards sustainable activities and ensure that companies are aligned with the European Union's (EU) sustainability goals. Nonetheless, a recent recommendation for a simplified application of the Taxonomy suggests that some regulatory flexibility may be introduced, also mentioned in the Omnibus.

Non-financial reporting and redirecting investment to sustainable activities

Following the adoption of the Corporate Sustainability Due Diligence Directive (C3D), in May of last year, large companies are now accountable for ensuring that their operations, including those of their subsidiaries and business partners, identify, prevent and address adverse human rights or environmental harm. Furthermore, the EU’s Carbon Border Adjustment Mechanism (CBAM), established under Regulation 2023/956, is designed to put a fair price on the carbon emitted during the production of carbon-intensive goods entering the EU. It aims to foster cleaner industrial production in non-EU countries while preventing ‘carbon leakage’, whereby companies relocate carbon-intensive production to regions with less stringent climate policies. As of 2026, cement, iron, steel, and aluminium importers will be required to purchase CBAM certificates, priced according to the weekly average auction price of the EU Emissions Trading System (ETS) allowances. Nevertheless, uncertainties and tension surrounding global trade dynamics and shifts towards nearshoring raise questions about the market’s reaction to these requirements, potentially driving up construction costs.

Integration of the value chain into corporate activities and reporting

Following its publication, the Portuguese Voluntary Carbon Market (VCM) is expected to come into operation in 2025, contributing to carbon neutrality goals and promoting projects that enhance biodiversity and natural capital, allowing the offsetting of the carbon emissions that could not be avoided in the real estate sector. In contrast, the Taskforce on Nature-related Financial Disclosures (TNFD) – like the Task Force on Climate-related Financial Disclosures (TCFD) – has taken on greater importance, with the development of recommendations so that companies and financial institutions can assess, report and act on their nature-related dependencies, impacts, risks and opportunities, in relation to their non-financial reports. This, therefore, demonstrates the surging relevance of natural values, in addition to a way of mitigating and adapting to climate change.

Increasing focus on biodiversity and natural capital

The real estate sector is in the midst of a fundamental transformation, where on the one hand integrating ESG criteria into investment decisions is no longer optional but a key strategic priority as ESG investment funds increasingly gain traction and attract significant capital, but, on the other, there is an attempt to make it more flexible, relieving legal pressure and leaving it up to the market to implement management models best suited to each organisation's activity and investment capacity. Real estate companies that proactively adopt robust ESG practices will not only enhance their market reputation but also future-proof their operations against evolving industry dynamics and reduce transition risks, thus maintaining the intention to implement ESG-aligned management models. These trends underscore a structural evolution in the real estate sector, where sustainability is an essential pillar for medium to long-term competitiveness and economic viability.

MARKETBEAT PORTUGAL,

SPRING 2025

For further information or copies of this or other reports, please contact: MARKETING & COMMUNICATION Miguel Sena miguel.sena@cushwake.com Tel.: +351 213 224 757 Cushman & Wakefield (NYSE: CWK) is a leading global commercial real estate services firm for property owners and occupiers with approximately 52,000 employees in nearly 400 offices and 60 countries. In 2024, the firm reported revenue of $9.4 billion across its core service lines of Services, Leasing, Capital markets, and Valuation and other. Built around the belief that Better never settles, the firm receives numerous industry and business accolades for its award-winning culture. To learn more, visit www.cushmanwakefield.com © 2025 Cushman & Wakefield. All rights reserved. Cushman & Wakefield Av. da Liberdade, 131- 5º 1250-140 Lisboa Av. Da Boavista, 1837- 8º 4100-133 Porto www.cushmanwakefield.com

HEAD OF PORTUGAL Eric van Leuven eric.vanleuven@cushwake.com TRANSACTIONS Paulo Sarmento paulo.sarmento@ cushwake.com RESEARCH & INSIGHT Ana Gomes ana.gomes@cushwake.com OFFICES Pedro Salema Garção pedro.salemagarcao@cushwake.com RETAIL João Esteves joao.esteves@cushwake.com INDUSTRIAL & LOGISTICS Sérgio Nunes sergio.nunes@cushwake.com HOSPITALITY Gonçalo Garcia goncalo.garcia@cushwake.com DEVELOPMENT & LIVING Manuel Magalhães manuel.magalhaes@cushwake.com

INVESTMENT David Lopes david.lopes@cushwake.com ESG Ana Luísa Cabrita analuisa.cabrita@cushwake.com ASSET SERVICES Bruno Silva bruno.silva@cushwake.com RETAIL ASSET SERVICES André Navarro andre.navarro@cushwake.com PROJECT MANAGEMENT Vitor Cajus vitor.cajus@cushwake.com VALUATION & ADVISORY Ricardo Reis ricardo.reis@cushwake.com BUSINESS DEVELOPMENT Isabel Correia isabel.correia@cushwake.com PRIVATE WEALTH Inês Sousa ines.sousa@cushwake.com