An Interactive Industry Leadership Report from

CATEGORY

CAPTAINS

2024

Breakfast

Salad Dressing

Coffee Creamers

Dry Packaged Dinners

Fresh & Deli

Frozen Foods

Peanut Butter

Protein Snacks

Plant-Based Beverages

Specialty Foods

Culinary Salt

Yogurt

A Canadian Grocer exclusive, click below to find data and insights that identify trends and growth opportunities in these categories:

CATEGORY CAPTAINS TABLE OF CONTENTS

CULINARY SALT Captain: Windsor Salt

FRESH & DELI Tree of Life

PROTEIN SNACKS Jack Link's Canada

SPECIALTY FOODS Tree of Life

CHECK BACK FOR MORE CATEGORIES ADDED MONTHLY

SPECIAL PROMOTIONAL FEATURE

BREAKFAST Kraft Heinz

PEANUT BUTTER The J.M. Smuckers Co.

SALAD DRESSING Pure by J.L. Kraft

COFFEE CREAMERS International Delight

PLANT-BASED BEV. Silk

YOGURT Activia

Bread

Coffee

Eggs

FROZEN FOODS Con Agra

EGGS Gray Ridge

COFFEE Van Houtte

BREAD Bimbo

Established Items

Culinary Salt is a well-established staple category in Canada, reporting $59MM in annual sales. The category reported some decline during the pandemic, but recovered fully in 2023, showing +14% growth vs. the previous year.

Specialty/Global

Personal Care

CULINARY SALT

2024 CATEGORY CAPTAINS

KEY CATEGORY INFORMATION

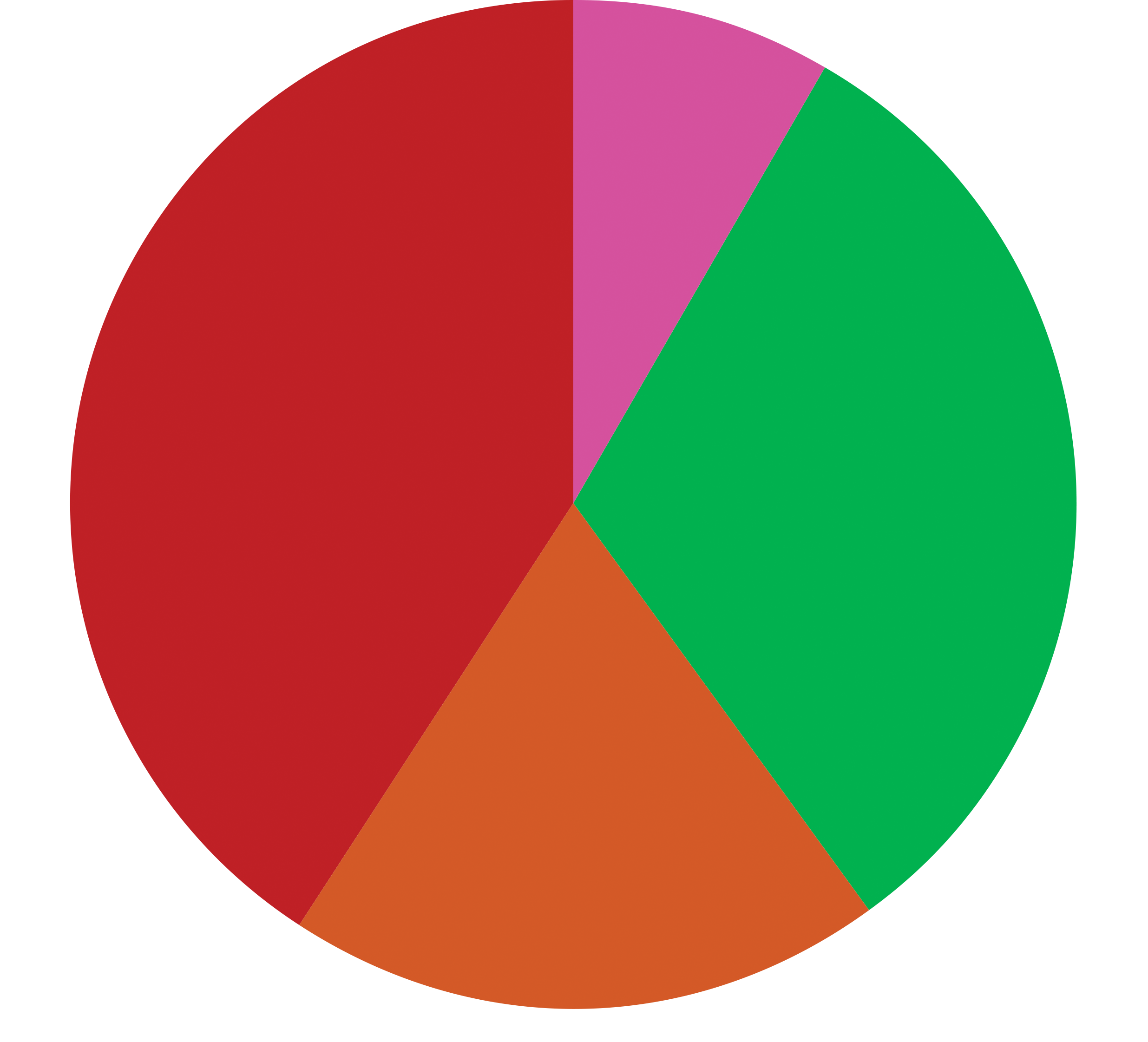

There are seven main segments in the Culinary Salt Category with Sea Salt, Table Salt and Pink Salt being the main segments, representing over 75% of the total market share.

Sea Salt (+5.4%) and Pink Salt (+2%) are the fastest-growing segments, reflecting rising consumer interest in natural and unprocessed food products along with awareness of the benefits of Sea/Pink Salt.

On average, Canadian consumers purchase two different types of Culinary Salt per year.

Culinary Salt Market Size, $ Sales

Types of Culinary Salt Purchased in Previous 12 Months/Most

$ Share and Variation by Salt Segment

TABLE SEA PINK KOSHER SEASONINGS PICKLING SUBSTITUTEs OTHER

Table Sea Pink Kosher Pickling Seasoned Salt Salt Substitute

$50 MM

$55 MM

$51 MM

$59 MM

2019

2020

2021

2022

2023

+10%

-7%

+0.5%

+14%

63%

46%

34%

16%

10%

42%

9%

On average, consumers have purchased

types of culinary salt in the Previous 12 Months

2.0

23.5% 35.6% 16.1% 8.3% 10.5% 3.0% 1.8% 1.2%

Sales $ Share by Segment

Source: Culinary Salt U & A Study, 2024 Q10. Which of the following types of culinary salts did you buy for your household in the past 12 months? Base: Gen Pop (n=2481)

35.6%

23.5%

16.1%

8.3%

10.5%

3.0%

1.8%

1.2%

Sea

TABLE

Pink

Kosher

Seasonings

Pickling

Substitutes

Other

2024 CATEGORY CAPTAIN

CATEGORY DATA

Sales $ Share By Segment

$ Share and variation by salt segment

BACK TO HOME PAGE

Source: Culinary Salt U & A Study, 2024

Year-Over-Year Growth

Source:

1

2

3

NEXT TO FRESH & DELI

Source: NielsenIQ, NAT GB+DR+MM, latest period ending May 18, 2024

Salad Dressings

Frozen Food

Sources: 1 Caddle Cheese Shopping Insights, March 2023; 2 NielsenIQ, All Channels, Natl L52W period ending Dec 30, 2023; 3 Mintel Canada, Cheese, 2022

Canadians take their cheese seriously, with 86% saying that cheese is a planned purchase.1 Packaged cheese is by the far the largest segment within the category, representing a 60% dollar share or $3B and growing at +5%.2 Most consumers are making their cheese purchases at grocery stores – with an even split between channels: 48% of consumers buy at conventional grocery and 47% buy at discount. Within the grocery store, most consumers are purchasing from the dairy section, however 1/3 are also purchasing from the deli counter and another 1/3 are purchasing from dedicated cheese counters.3

Canned Tomatoes

Plant-Based

FRESH & DELI

Expanded occasions – the versatility of cheese will be its winning factor. The vast array of domestic and imported varieties fulfills all need-states and occasions.

Cheese has not been immune to ongoing pricing concerns, but the pièce de resistance of this category is its flexibility between nourishment and indulgence.

Source: NielsenIQ, All Channels, Natl L52W period ending Dec 30, 2023

Familiar flavours – flavoured cheeses are an important segment to the category, but consumers will reach for familiar before unique flavour innovation. Familiarity is a safe buying strategy, especially for specialty cheeses.

Variety for occasion – cheddar continues to hold a large share of our fridge deli drawers, but curious consumers are open to trying different varieties. Domestic artisanal brands are showcasing stellar cheeses. Meanwhile, access to imported cheese varieties from abroad allows for global exploration.

Base: 1,901 internet users who eat cheese Source: Kantar Profiles/Mintel April, 2022

Dairy section of grocery stores (i.e. where cheese is pre-packaged)

Deli counters in grocery stores

Dedicated cheese counters in grocery stores (i.e. sells artisanal cheese)

Where Cheese Is Typically Purchased

Cheese Ticks the Boxes on Both Nourishment and Indulgence

Cheese makes meals/snacks more nourishing

Cheese makes for an indulgent treat

% agree

As a category, one of cheese's biggest advantages is it meets a variety of needs. The vast majority of Canadians view cheese as being both a nourishing and indulgent option when deciding what to eat. As the category looks to grow in a heavily penetrated market, increasing frequency offers more opportunity. In this respect, cheese's versatility is its biggest asset.

NATURAL CHEESE - EXACT WEIGHT NATURAL CHEESE - EXACT WEIGHT DELI CREAM CHEESE - EXACT WEIGHT NATURAL CHEESE - RANDOM WEIGHT PROCESSED CHEESE SLICES COTTAGE CHEESE GRATED CHEESE PRODUCTS

3,073,162.1 909,617.7 353,842.6 249,813.7 248,764.4 144,349.6 100,667.7

+5% +6% +9% -7% +6% +18% -5%

433,464.0 107,491.0 74,454.3 7,187.5 49,873.1 28,905.9 10,524.7

+1% -1% 0% -9% +1% +9% -10%

Cheese Performance in Canada

$ (000)

$ Change vs YA

Units (000)

Unit Chg vs YA

90% agree

83% agree

Source: Mintel Canada, Cheese, 2022

NEXT TO PROTEIN SNACKS

BACK TO CULINARY SALT

Sources: 1 Mintel, Future of Animal Proteins, 2024; 2 Canadian Grocer GroceryIQ Study, 2024; 3 Mintel, Snacking Motivations, 2024

Within the Protein Snack category, meat snacks have continued to demonstrate consistent year-over-year growth in Canada, fueled by consumers' desire to ensure they are getting enough protein in their diet.

PROTEIN SNACKS

Meat Snacks encompass more than just Beef Jerky. Although Jerky represents over 60% of the category, we continue to innovate to provide a variety of protein types, flavours and formats (meat sticks, tender bites, steaks & combos) to meet all consumer and shopper preferences.

Canadians are turning to snacks with protein in their quest for healthier food options.

46% of Canadian consumers agree they can't get enough protein without eating animal meat.1

Consumers are increasing their snacking, with 22% snacking 3+ times a day, and 63% at least somewhat agree that a few snacks can be more satisfying than a meal.3

Trends in product innovation, coupled with consumers’ focus on prioritizing nutritional snacking, will continue to fuel the growth of Meat Snacks in Canada.

Meat Snacks, as a Category, Continue to Deliver Sales Growth

$213 MM

$221 MM

$231 MM

$250 MM

2026*

Source: NielsenlQ MarketTrack. National All Channels. Total Meat Snacks Trended sales L52W period ending July 13, 2024. * Projected Sales

Although consumers face mounting expenses, they prioritize categories offering potential long-term health benefits.

Protein is considered the most important nutrient, and most Canadians think of meat as the main source of protein.

Canadians are turning to snacks with protein in their quest for healthier food options.1

Meat Snack Segments and Formats

Jerky & Nuggets

Meat Sticks

Meat & Cheese Combos

Steaks & Bars

26%

64%

6%

4%

Source: 1 SimplyProtein/Maru Public Opinion online panel survey, February 8, 2023

Source: NielsenIQ. National Grocery, Drug & Mass Merchandise + Convenience WCGM. L52W period ending May 18, 2024

NEXT TO SPECIALTY FOODS

BACK TO FRESH & DELI

Nearly 1 in 4 health conscious grocery store shoppers indicated that they are interested in the protein content of the foods they purchase.2

Meat Snacks Continue to Attract New Shoppers

Meat Snacks attracted +200,000 additional Canadian households to purchase the category in 2023. Shoppers are spending more and putting Meat Snacks in their basket more often.

More Buyers

More $ Per Buyer

More Trips Per Buyer

3.4 Million Households

+200,000

Source: Nielsen Homescan. Market Summary. 52 weeks to Feb. 2024. Total Outlets. Total Meat Snacks

SPECIALTY FOODS

Sources: 1 Stats Can; 2 Nielsen IQ Item Ranking – Oriental Sauces Plus Cooking & Baking Sauces, National excl NFLD GB+DR+MM, L52W period ending Sept 2, 2023; 3 Mintel – Internationally Inspired Foods, Canada, 2023

Source: Mintel – Internationally Inspired Foods, Canada, 2023

The Asian cooking and baking sauces segment in Canada experienced a 12% increase in sales, reflecting the growing preference for home cooking.2 Chinese cuisine is favoured, followed by Mediterranean and Latin American/Mexican dishes. African cuisine piques the interest of 45% of Canadians, followed by Korean and Caribbean flavours.3

Chinese Mediterranean Latin Am./Mexican Western European Eastern European Japanese Indian/South Asian Southeast Asian Middle Eastern Caribbean Korean African

Canada: Consumption and Interest in International Foods, 2023

Canada's shifting demographics, fueled by immigration and global connectivity, is propelling its culinary world into a vibrant tapestry of flavours. Almost 40% of new immigrants hail from Asian countries like India, the Philippines, and China, enriching Canada's food culture.1 While Canadians are increasingly embracing international cuisines for diverse experiences, new immigrants often seek comfort in dishes reflecting their cultural heritage.

Grocery stores can diversify their offerings by introducing meal kits, and frozen or fresh prepared meals, encouraging customers to explore new flavours. Fusion dishes are a welcoming gateway to international cuisine for those seeing new culinary experiences. With these trends, Canada's food landscape is set for ongoing expansion and evolution.

Source: Nielsen IQ Item Ranking – Oriental Sauces Plus Baking & Cooking Sauces, National excl NFLD GB+DR+MM, L52W period ending Sept 2, 2023

Canada: International Foods Canadians Have Not Eaten But Are Interested in Trying, 2023

Canada: Areas of Interest in International Foods, 2023

Market Size, Dollar Growth and Unit Sales

African Korean Caribbean Southeast Asian Eastern European Middle Eastern Western European Indian/South Asian Japanese Latin American/Mexican Mediterranean Chinese

Fusion dishes inspired by a mix of differnt regions

Seasoning kits inspired by a mix of differnt regions

Salty snacks seasoned with internationally inspired flavours

Desserts infused with internationally inspired flavours

Beverages

Heatable prepared foods inspired by international foods

International/internationally inspired meal kits

90.0

82.7

81.7

76.7

72.7

69.3

67.8

67.6

65.8

58.3

48.1

25.2

6.5

11.1

11.6

17.1

18.3

14.7

16.7

18.8

17.2

26.8

30.7

45.1

4.5

6.2

6.7

9.0

16.0

15.5

13.6

17.0

14.9

21.2

29.7

percent of customers

45

31

27

19

18

17

15

12

11

6

43

41

38

32

ORIENTAL SAUCES PLUS BAKING & COOKING SAUCEs

Dollar Sales

$231,827,243

+12%

59,301,806

59,936,863

Have eaten

Have not eaten, but interested in trying

Have not eaten, not interested in trying

90

83

82

77

73

69

68

66

58

48

25

4

7

9

16

14

21

30

Unit Sales

-1%

$207,449,931

BACK TO PROTEIN SNACKS

Sources: 1. NielsenIQ, National All Channels, L52W Period Ending July 13, 2024; 2. NielsenIQ Panel On Demand Homescan Data, L52W Period Ending July 13, 2024; 3. Erickson Research, Peanut Bureau of Canada – Canada (2024)

With annual household penetration at 67.8%,2 Canadians continue to consume peanut butter in their diets, perceiving it as a healthy, convenient, on-the-go option that satisfies hunger and provides an energy boost.3 With multiple usage occasions, Canadians continue to use peanut butter as a spread (77%), ingredient in dishes (45%) or even straight out of the jar (28%).3 Peanut Butter continues to offer an affordable solution to evolving consumer needs, making it key for retailers to offer a variety of Brands to meet them.

Peanut Butter continues to be a household staple for Canadians, reaching annual sales of $351 million.1 While the total category has experienced inflationary dollar growth of 6%, tonnage volume has declined slightly by 2%.1 The category is led by Regular (Stabilized) Peanut Butter, accounting for 81% of sales across the category and experiencing dollar growth of 7% vs year ago, while the Natural Peanut Butter segment represents the remaining 19% of total category with annual dollar growth of 2%.1 Creamy Peanut Butter continues to be the preferred Peanut Butter sub-segment of consumers (68%), followed by Crunchy (19%), Light (12%), and Dark Roast (1%).1

Total Dollar Volume and % of Dollar Share

Source: NielsenIQ, National All Channels, L52W Period Ending July 13, 2024 Note: Creamy and Crunchy calculations exclude overlap of Light and Dark Roast Sub-Segments

Creamy

Crunchy

Light

Dark Roast

$236,792,526

$65,125,490

$42,663,009

$5,135,263

67.7%

18.6%

12.2%

1.5%

Peanut Butter Sub-Segments

Source: NielsenIQ, National All Channels, L52W Period Ending July 13, 2024

Total Peanut Butter Dollar Volume

80.6%

$283,176,854

19.4%

$68,026,059

$351,202,913

Natural Peanut Butter

Regular Peanut Butter

Peanut Butter Segments, Dollar Volume and Dollar Share

L52W 2YA

$306,018,347

$330,060,419

57,061,381

60M

40M

20M

0

$350M

$300M

$250M

$200M

$150M

55,771,549

54,421, 861

L52W YA

L52W

$ Volume

Tonn Volume (kg)

Peanut Butter 3-Year Trend

PEANUT BUTTER

Sources: 1 NielsenIQ, TOTAL National - L52W period ending Aug 17 2024 & Cal-Year 2022 & 2023 2 NielsenIQ, TOTAL National - BMO TOTAL OUTLETS - L52W period ending Jul 27 2024 & Cal-Year 2022 & 2023 3 NielsenIQ, TOTAL National - L52W period ending Aug 17 2024 4 Ipsos FIVE 12ME February 2024 | % Occurrences – Total Food Universe

Pourable Salad Dressings are primarily consumed at meal occasions led by dinner, and routinely used with over 60% consuming it three or more times per week4. Since 2020, household penetration continues to decline as consumers are dissatisfied with the additives and lack of flavour in current offerings, turning to homemade dressings for simpler, customizable ingredients. While salads remain the top host food, consumers are expanding consumption to non-traditional occasions such as dipping with creamy dressings and marinating with vinaigrettes4.

Pourable Salad Dressings (PSD) is a $316MM1 mature category with a +3.4% 2-year CAGR and an average household penetration of 71.7% over the last 2 years2. The category is comprised of two major segments, refrigerated and shelf stable dressings (SSD), where SSD represents two-thirds of the category. In the last 52 weeks, PSD has seen a continued rise in dollar sales vs. prior year while overall product consumption declines (-3.0% pounds vs. last year)3 – this is due to two factors, rise of inflation and growth of premium smaller/restaurant brands.

2024*

*Note: Year to date, August 17, 2024 Source: NielsenIQ, TOTAL National - L52W period ending August 17, 2024 & Cal-Year 2022 & 2023

Dollar Sales ($)

$295,138,383

$315,264,376

$315,666,765

75,146,987

75,104,053

72,856,507

Volume in Pounds (lbs)

80M

70M

75M

$320M

$280M

Dollar Sales Growth But Decline in Pounds Due to Inflation & Premiumization

Importance in Both Shelf Stable & Refrigerated Segments

Shelf-Stable Share

Refrigerated Share

66.3%

33.7%

66.2%

33.8%

66.5%

33.5%

*Note: Year to date, August 17, 2024 Source: NielsenIQ, TOTAL National - BMO TOTAL OUTLETS - L52W period ending July 27, 2024 & Cal-Year 2022 & 2023

% of household penetration

74.6%

72.5%

71.8%

70.8%

Household Penetration

SALAD DRESSINGS

Sources: 1. Mintel, June 2023 | Insight Plant-Based Milks Can Recruit New Flex-Dairy-ans; Mintel, Dairy and Non-Dairy Milk Canada, 2023. 2. Mintel, August 27, 2024 | Report Milk and Non-Dairy Milk – US – 2024. 3 Nielsen, MarketTrack, National Incl. NFLD GB+DR+MM – L52W period ending July 13, 2024.

The Plant-Based category lends itself to the changing consumer landscape as 80% of new Canadians, particularly those from South Asia, have purchased non-dairy milk in the last three months.1 This is especially true for recruitment and retention of younger shoppers as 73% of new Canadians aged 18-34 have purchased non-dairy milk in the last three months, important facts for long-term category growth as 44% of the Canadian population is expected to be multicultural by the year 2030.2 Consumer behaviours have influenced Coconut base growing at +13.4% dollars3 due to its versatility across many occasions including cooking. Changing demographics and the high protein offering in Soy helped the segment deliver +0.2 dollar share gains.3 The Dairy Like segment, delivering on taste and texture sought out by the plant-based consumer secured a 2.0 share, +17.3% dollars in the latest 52 weeks3 on portfolio and distribution expansion.

Health and taste are the main reasons why Canadians turn to non-dairy milk, with health as the number one purchase driver for all plant-based shoppers in Canada. Personal values influence buying behaviour as those who eat plant-based diets are 2.5 times more likely than the average consumer to say they chose their diet to align with their values, highlighting the impact of rising consumer concerns around health, sustainability, animal welfare and food security.

Source: Nielsen, Marketrack, National Incl. NFLD GB +DR +MM, L52W period ending July 13, 2024.

Source: Nielsen, Marketrack, National Incl. NFLD GB +DR +MM L52W period ending July 13, 2024.

$ Share of Segment

PLANT-BASED BEVERAGES

Coconut/Almond 1%

Cashew 3%

Oat 27%

Dairy-Like 2%

Coconut 5%

Soya 15%

Almond 46%

Active Health 20.3%

Rice 1%

2012

2013

2014

2015

2016

2017

2018

L52 2023

Total Plant-Based Beverages

Almond

Oat

Soy

Blends

Dairy-Like

20%

30%

40%

50%

Sources: 1. Coffee & RTD Coffee Report – US – 2024, Mintel, 2024 2. Nielsen, MarketTrack, National Incl. NFLD GB+DR+MM L52W period ending September 7, 2024

Cold coffee drinks (Cold Brew & Iced Coffee) continue to create excitement with portfolio innovation and increased awareness fueled by a rise in distribution points across all channels. Cold Brew, in particular, has posted category growth of +27.2% in the last 52 weeks. Despite the growth of RTD and multi-serve RTD cold coffee, 30% of consumers reported drinking more hot coffee compared to last year, driven by Gen Z and Millennials paving the way for continued coffee creamer growth.1

Consumers seeking to replicate an out-of-home coffee experience are fueling the growth of Flavoured Coffee Creamers (+7.4%), ranking as one the fastest growing categories within the Refrigerated Dairy case in the last 52 weeks.2 Refrigerated Coffee Flavourings are fueled by strong growth within the Traditional Segment +4.9% dollar sales driven by Dollar Sales per Point of Distribution growth of +9.1% and Large format (>1L) growth of +16.7% in the last 52 weeks.2 Refrigerated Plant Based Creamer's momentum continues as the segment grew at +7.3% in the last 52 weeks.2 Creamers performance is supported by the growth of Barista Shelf Stable Creamers, posting gains of +11.5% in the last 52 weeks on increased TDP’s of +4.6%.2 Category growth is aided by new occasions created through innovative items such as Cold Foam Creamer, introduced to the market in February 2024, the segment has secured a 3.4 dollar share of the Total Refrigerated Coffee Creamers & Flavourings in the last 12 weeks.2

Segmentation & Shifting

Traditional

Dairy Cream 49.9%

Coffee Creamers & Flavourings 50.1%

68%

32%

Source: Nielsen, MarketTrack, National Incl. NFLD GB+DR+MM – L52W period ending September 7, 2024

July 2021

June 2022

June 2023

June 2024

28.8%

32.3%

33.1%

33.2%

COFFEE CREAMERS

L52W Growth: +4.7%

L52W Growth: +7.4%

L52W Growth: +3.5%

$391M

$393M

Sources: 1. Nielsen Homescan, National Incl. NFLD GB +DR + MM, L52W period ending June 15, 2024. 2. Nielsen, National Incl. NFLD GB +DR + MM, L52W period ending September 7, 2024 3. Yogurt and Yogurt Drinks Report 2024 - Canada, Mintel.

Consumption of yogurt has been driven in part by an increase in household penetration, hitting 88.6% in the last 52 weeks,1 +0.2 pts and a shift towards more premium and value-added segments, mainly functional benefits, which has lifted total Yogurt category growth of +9.2% dollar share, +5.4% EQ (tonnage) in the last 52 weeks.2

Rolling 52 w/e June 18, 2022

Source: Nielsen Homescan, National Incl. NFLD GB +DR + MM, rolling 52W period ending June 15, 2024.

88.2%

88.6%

Household Penetration (%)

90%

85%

Household Penetration Rate (Last 3 Years)

Source: Nielsen, National Incl. NFLD GB +DR + MM, L52W period ending September 7, 2024.

Light 4.2%

Indulgent 6.5%

Absolute Change in Sales $

Absolute $ Growth of the Segment

YOGURT

The primary motivation for consumers planning to increase their yogurt intake is the pursuit of a healthier diet, focusing on products that offer specific health benefits. Yogurts highlighting health attributes, include those with natural ingredients, protein and added functional benefits.1

The Greek segment continues to drive absolute dollar sales as shoppers are seeking out high-protein options within their diets. 45% of consumers agree that "high in protein" is a key health-related consideration when choosing yogurt products.3 50% of consumers are interested in yogurt with a creamier/thicker texture which is very on trend with the profile of High Protein and Indulgent segment. In addition to consumer interest in high-protein, shoppers are seeking gut-healing properties found within Yogurt, especially within the Active Health segment holding a 20.3 dollar share of total yogurt on +3.8% dollar growth in the last 52 weeks2 driven by gut health, gut microbiome and probiotic trends. Continued growth of the yogurt category will stem from an appetite for healthier lifestyles, satisfied by a broad selection of Yogurt with functional benefits and diverse flavours.

YOGURT GREEK INCL SKYR ACTIVE HEALTH KIDS REGULAR INDULGENT LIGHT ORGANIC PLANT-BASED ALL OTHER

113,720,886

164,727,754

14,674,871

1,655,685

12,285,629

17,883,297

-172,725

2,503,865

-281,161

2,457,408

Regular 15.8%

Kids 13.8%

Greek Including SKYR 34.5%

Plant Based 2.0%

Organic 2.5%

Other <1%

Rolling 52 w/e June 17, 2023

Rolling 52 w/e June 15, 2024

Sources: Ipsos 10th Edition of Consumption Habits and Attitudinal Trends, Dec. 2023

Breakfast habits in Canada are shifting in the wake of the pandemic. Skipping breakfast is becoming more common, particularly among younger adults, with more than one in five Canadians acknowledging a tendency to skip this meal. In contrast, families with children continue to prioritize breakfast, presenting opportunities for retailers and brands. Currently, 81% of breakfast occasions are sourced from home, with an increase in carried-from-home options (+1% vs. 2022) among work commuters. Traditional breakfast staples like eggs, sliced bread, and ready-to-eat cereals remain popular, showing strong ongoing performance. Brewed coffee remains the primary breakfast beverage, however, there has been growth in the consumption of specialty hot coffee and hot chocolate.

Source: Ipsos FIVE R12ME August 2023 – % Occasions, Indexed to Total Population

Top Commercial Beverages at Breakfast

Source: Ipsos FIVE R12ME August 2023 – % Occasions Based on Total Foods consumed at Breakfast, Indexed to Total Population

Top Food at Breakfast

Source: Ipsos FIVE R12ME August 2023 – % Food/Comm Beverage Occasions, Indexed to Total Population

Total Population

Breakfast Occasion Venue

BREAKFAST

The top motivators for breakfast choices are the need for physical energy, hunger satisfaction, and ease of preparation. Consumers of all ages are increasingly seeking ultra-convenient breakfast options that take less than 15 minutes to prepare, favouring portioned and portable choices. Given breakfast is the most important meal of the day, brands and retailers have ample opportunity to grow by addressing evolving consumer preferences and emerging trends.

Carried from home

8%

81%

1%

Sourced from restaurants

Sourced from home

Sourced from HMR/All Other

PT. Chg. vs. 2022

+1.0

+0.6

-0.2

-1.4

Eggs Fresh fruit Sliced bread/toast RTE cereal Cheese Yogurt Hot cereal All other breads Bagels Bacon Muffins Waffles/pancakes Croissants/biscuits Buns/rolls Bars

Pt. Chg. v. 2022

+0.3 -0.7 +1.1 +0.2 -0.6 -0.4 +0.2 +1.0 -0.6 -0.5 +0.7 0.0 -0.1 +0.5 -0.1

32% 25% 25% 19% 15% 12% 10% 8% 8% 7% 4% 4% 3% 3% 3%

Hot brewed coffee Milk and dairy alt. Dairy milk Plant based beverages Fruit/veg. juice/drink Hot tea Flat bottled water Specialty hot coffee Hot chocolate Carbonated soft drinks Iced/cold coffee Smoothie Sparkling water Iced tea Enhanced Water

+0.5 -2.4 -3.1 +0.3 -2.3 +0.4 +1.0 +0.7 +0.5 -0.3 0.0 +0.4 +0.1 +0.1 +0.1

46% 14% 12% 2% 13% 12% 8% 7% 4% 2% 2% 1% 1% 1% 0.3%

Sources: 1. Shopper Intelligence, Coffee Category Decision Factors Importance, 12 months ending Q1, 2024. 2. Mintel, The Sustainable Consumer, Canada, December 2023. 3. Coffee Association of Canada, Coffee drinking trends, (n=1,503), December 2023.

The Coffee category has seen continued value growth over the past year, fueled by the rising demand for instant coffee, espresso capsules, and ready-to-drink beverages across grocery stores, drugstores, and mass merchandisers. While traditional coffee and K-Cup® pods remain key stable segments, meeting consumer needs for innovation1, sustainability2, and affordability1 is critical for driving further expansion. Over the last 52 weeks, larger K-Cup® pod formats have gained popularity as consumers navigate economic pressures and tighter budgets. The latest Coffee Association of Canada study reveals that many are stocking up on coffee to manage inflation3. Highlighting sustainability and promoting value-driven messaging will help unlock additional growth opportunities.

Source: 2023 Q4 Shopper Intelligence Grocery Survey, Decision factor importance rank 1 to 10

Rising Influence of Younger Coffee Drinkers (16-34 yrs.)

Source: Coffee Association of Canada, Coffee drinking trends, (n=1,503), December 2023

Coffee Shopper Behaviours

Source: Nielsen NATIONAL EX NFLD GB +DR +MM, L52W period ending June 15 2024, Espresso Caps are compatible Nespresso capsules sold at retail.

Coffee Annual Value

COFFEE

Coffee Disc

$563M

$500M

$73M

$35M

Espresso caps

K-Cup Pods

Traditional Ground

$168M

$233M

$81M

Total Coffee Annual Value $2,661M / +6%

Traditional Beans

Instant

Ready to Drink Coffee

This group is more likely to make unplanned purchases, with

of them indulging in spontaneous buys.

21%

61%

of consumers are stocking up on at-home coffee when it's on sale

of consumers started buying larger packages of at-home coffee to save money

+0%

+39%

-17%

-2%

+2%

+7%

+6%

Sources: 1. Nielsen, National All Channel L52W period ending June 15, 2024. 2. IPSOS Canada, 5YR month ending June 2024.

Frozen Food in Canada continues to experience notable growth, with a compound annual growth rate (CAGR) of 7.6% over the past five years, accompanied by a unit growth of 1.3% during the same period. Key factors, including rising inflation, are infl uencing the growing trend of meals prepared at home, now accounting for 78.8% of food consumption, up from 77.3% last year. Consumers’ desire for convenient yet high-quality meal options has propelled frozen dinners and entrées, the largest subcategory, to grow at an 8.5% CAGR, reaching $2.6 billion in sales.1

Source: IPSOS Canada, Total Food Items 12M ending June 2024.

Where Food Was Eaten

Source: IPSOS Canada, 5YR month ending June 2024

Top 10 Frozen Meals & Entrees Motivations

Source: Nielsen, National All Channel L52W period ending June 15, 2024

Frozen Food Department Performance Report

FROZEN FOODS

Frozen dinners and entrées are favoured by a diverse range of demographics. Millennials and Gen Z, responsible for 41% of frozen food occasions, are drawn to the wide selection of global flavours available, offering culinary adventure without the time and effort of cooking from scratch. For busy families with young children, frozen meals provide quick, nutritious solutions, while frozen snacks and appetizers have become a go-to for snacking.2

Older adults also appreciate frozen foods for their ease of preparation, reliability, and portion control, particularly as they seek balanced meals with minimal effort. At the same time, classic comfort foods continue to play a significant role across all age groups. These familiar dishes provide a sense of nostalgia and comfort, making them a go-to for those seeking warmth and simplicity in their meals.

The Frozen category strikes an effective balance between convenience, affordability, variety, and familiar comfort, making frozen dinners and entrées a staple for a wide array of consumers.

Sources: 1. NielsenIQ MarketTrack National Incl NFLD GB+DR+MM L52W period ending August 10, 2024 2. NielsenIQ Panel data National Total Outlets L52W period ending June 15 2024

Commercial Bread is $3.4 billion in sales1 in the last 52 weeks (ending August 10, 2024) with sales growth of +1% and gaining $29 million in Canada. Commercial Bread is a large grocery category and plays a significant role at retail with a high household penetration of 97%2. Higher Health—comprised of grains, rye, dietary needs (weight management, no fat, no sugar, gluten free) and organic breads— is the largest segment in Commercial Bread with almost a 19% dollar share, followed by White Bread at 18%, Buns & Rolls at 18%, and Breakfast at 15%. These four major segments account for 70% of the Commercial Bread category.

Source: NielsenIQ MarketTrack L52W period ending August 10, 2024

Commercial Bread Segmentation

Source: NielsenIQ MarketTrack BRANDED ONLY L52W period ending August 10, 2024

Innovation Key Growth Drivers

BREAD

Higher Health is the segment that supports consumers’ growing awareness and demand for healthy, nutritious and “better-for-you” products.

Sources: 1. NielsenIQ - National EXCL NFLD GB +DR +MM - L52W Period Ending May 18, 2024 2. NielsenIQ – National All Channels - L52W Period Ending May 18, 2024

In Canada, Eggs in all forms (Shelled, hard boiled, liquid and liquid replacement eggs) is a $1.5B dollar category1. Mature categories rarely generate significant growth yet Canadian consumers have increased total Egg sales by $111.8MM (+8%) vs the same time last year. The value added segments are also contributing to total egg growth (Figure 1).

Source NielsenIQ - National EXCL NFLD GB +DR +MM - L52W Period Ending May 18, 2024

Figure 3 - Average Unit Price

Source: NielsenIQ - National GB+D+MM L52W Period Ending June 29,2024

Figure 2 - $ Sales, $ Share and $% Change

Source: NielsenIQ - National EXCL NFLD GB +DR +MM - L52W Period Ending May 18, 2024

Figure 1 - $ % Chg vs YA

EGGS

More households are purchasing Shelled Eggs (buyers +2%) and those households who purchased last year are spending more ($’s per HHLD +5.8%).2 (see Figure 4) This trend isn’t surprising as consumers are looking to larger pack sizes in the category to find value. Both 18 Packs (+13%) and 30 Packs (+33%) have increased their share of Eggs significantly versus a year ago.1

Shelled Eggs are the largest segment accounting for 97% of total Egg sales and growing +8%.1 From coast to coast, Shelled Eggs are generating more revenue for retailers. (see Figure 2) It is important to understand segment development for the east vs west to address regional consumer demands.

Although Conventional Eggs (no additional claims) make up the largest share of Shelled Eggs (76.8 dollar share & +9%), Specialty Eggs have been growing significantly as well (23.2 dollar share & +6%).1 Free Run Eggs have been a primary driver of Specialty Eggs growing +14% vs year ago.1 This trend is positive for building bigger baskets in the category as Specialty Eggs retail at a higher price per unit vs Conventional Eggs. (see Figure 3) Optimizing the category requires keeping up with trends on larger packages while offering a strong range of specialty products.

Source NielsenIQ – Homescan - National All Channels - L52W Period Ending May 18 2024

Figure 4 - Shelled Eggs

Sources: 1. NielsenIQ Discover, Total Chocolate, National GDM+RFC+C&G+GMWC, L52W period ending December 28 2024 2. NielsenIQ Discover (XMAS INCL (EVDAY SEAS EXCL JR), National GDM+RFC+C&G, 9 week period ending December 28 2024; EASTER SEAS CHOC, 12 week period ending APRIL 06 2024, NATIONAL EX NFLD GB+DR+MM + RFD + C&G; VAL INCL (EVDAY SEAS), 5 week period ending FEB 24 2025, NATIONAL EX NFLD GB+DR+MM + RFD + C&G; HLWN SEAS + EVDAY SEAS JR, 13 week period ending NOV 9 2024, NATIONAL EX NFLD GB+DR+MM + RFD + C&) 3. Numerator Insights, Christmas Chocolate, Total Outlets, 9 week period ending December 28 2024 4. Suzy 2023– Christmas Survey n=300, Shoppers 18-65 who bought Chocolate at the Holidays 5. NielsenIQ Discover, XMAS INCL (EVDAY SEAS EXCL JR) BOXED Chocolate, National GDM+RFC+C&G, 9 week period ending December 28 2024 6. Suzy – Christmas Survey n=300, Shoppers 18-65 who bought Chocolate at the Holidays

The Canadian Chocolate market is well-established and a steadily growing industry, that saw +2% growth in $ sales in 20241. With Chocolate so synonymous during the holidays, key seasonal peaks, such as Valentine’s Day, Easter, Halloween, and Christmas contribute significantly to overall sales of the Chocolate market2. During these times, the Chocolate industry is often greeted with seasonally-specific graphics, limited-time formats, or limited-time offerings during key holidays.

Source: Suzy 2023 – Christmas Survey n=300, Shoppers 18-65 who bought Chocolate at the Holidays Q14 - Do you always give chocolate as a gift at the holidays? Q15 - Why did you decide to purchase Chocolate as a gift this year? Q13 - When gifting chocolate this Holiday Season, did you gift the chocolate with another item or just gift on its own?

Chocolate Continues to be a Key Gift at Christmas

Source: NielsenIQ Discover XMAS INCL (EVDAY SEAS EXCL JR), 9 week period ending December 28, 2024. NATIONAL EX NFLD GB + DR + MM + RFC + CG EASTER SEAS CHOC, 12 week period ending April 6 2024, NATIONAL EX NFLD GB + DR + MM + RFD + C&G VAL INCL (EVDAY SEAS), 5 week period ending February 24 2025, NATIONAL EX NFLD GB + DR + MM + RFD + C&G HLWN SEAS + EVDAY SEAS JR, 13 week period ending November 9 2024, NATIONAL EX NFLD GB + DR + MM + RFD + C&G

Christmas Is The Biggest Season of the Year for Chocolate

CONFECTIONERY/SEASONAL CHOCOLATE

Nearly two-thirds of Canadian households purchase Chocolate during the Christmas holiday3, making Christmas the largest $ sales driver of category sales during the year. Chocolate remains a popular Christmas gift, with 1 in 2 people choosing to give it during the holiday season4. Boxed Chocolate represents 62% of total seasonal category $ sales5, making it the most loved form of Chocolate during the holidays. In particular, Boxed Chocolate is a favourite for gift-giving, for hosting or for sharing during a party, or even as a self-indulgent treat during the festive season6.

As a retailer, stocking up on leading-brand Boxed Chocolates will provide your shoppers with options for all their holiday special moments.

Top Reasons Why Shoppers Buy Boxed Chocolate at the Holidays

Source: Suzy – Christmas Survey n=300, Shoppers 18-65 who bought Chocolate at the Holidays Q4 – And now, for each of the reasons you just mentioned, please select the chocolate format/s you purchased for each of those occasions

Sales

30.7%

21.5%

40.6%

$63.4M

$234.9M

$144.1M

$302.5M

Valentine's Day 2024 Easter 2024 Halloween 2024 Christmas 2024

85% gift Chocolate every year

Chocolate is Universal 67% gift because everyone likes it

1 in 2 people gift it on its own

Gifting

Hosting

Self-Indulgence/ Gifting

62%

56%

41%

To give as a gift to adult family or friends

Hosting or sharing at large gathering/party

As a gift for myself

Confectionery

Source: Nielsen Market Track. XMAS INCL (EVDAY SEAS EXCL JR), 9 week period ending December 28 2024. NATIONAL EX NFLD GB + DR + MM + RFC + CG

Boxed is the Biggest Format at Christmas with Shoppers Buying for Gifting, Hosting and Treat Occasions

Boxed Novelty Pieces Bars Singles Multi Junior King Size

(Under $1 M)

$1.9M (0.6% $ Shr)

$2.3M (0.8% $ Shr)

$26.8M (8.8% $ Shr)

ADVENT

$6.6M (2.2% $ Shr)

$18.2M (6.0% $ Shr)

$39.1M (12.9% $ Shr)

$48.0M (15.9% $ Shr)

$186.5M (61.7% $ Shr)

Total Christmas $ Sales: $302.5M

$350M $300M $250M $200M $150M $100M $50M $0M