An Interactive Industry Leadership Report from

CATEGORY

CAPTAINS

2025

Eggs

Salad Dressing

Coffee Creamers

Dry Packaged Dinners

Fresh & Deli

Frozen Foods

Peanut Butter

Viscous

Plant-Based Beverages

Specialty Foods

Confectionery/Chocolate

Yogurt

A Canadian Grocer exclusive, click below to find data and insights that identify trends and growth opportunities in these categories:

CATEGORY CAPTAINS TABLE OF CONTENTS

CULINARY SALT Captain: Windsor Salt

FRESH & DELI Tree of Life

PROTEIN SNACKS Jack Link's Canada

SPECIALTY FOODS Tree of Life

CHECK BACK FOR MORE CATEGORIES ADDED MONTHLY

SPECIAL PROMOTIONAL FEATURE

BREAKFAST Kraft Heinz

PEANUT BUTTER The J.M. Smuckers Co.

SALAD DRESSING Pure by J.L. Kraft

COFFEE CREAMERS International Delight

PLANT-BASED BEV. Silk

YOGURT Activia

Bread

Coffee

FROZEN FOODS Con Agra

EGGS Gray Ridge

COFFEE Van Houtte

CONFECTIONERY/ CHOCOLATE Ferrero

FROZEN FODS Con Agra

COFFEE CREAMER International Delight

PLANT BASED BEVERAGES Silk

VISCOUS Heinz

YOGURT Activa

PEANUT BUTTER Kraft

CATEGORY DATA

Sources: 1. NielsenIQ Discover, Total Chocolate, National GDM+ RFC + C&G + GMWC, L52W period ending December 28 2024 2. NielsenIQ Discover (XMAS INCL (EVDAY SEAS EXCL JR), National GDM + RFC+ C&G, 9 week period ending December 28 2024; EASTER SEAS CHOC, 12 week period ending April 6 2024, NATIONAL EX NFLD GB + DR + MM + RFC + C&G; VAL INCL (EVDAY SEAS), 5 week period ending February 24 2024, NATIONAL EX NFLD GB+ DR + MM + RFC + C&G; HLWN SEAS + EVDAY SEAS JR, 13 week period ending November 9 2024, NATIONAL EX NFLD GB+DR+MM + RFC + C&G) 3. Numerator Insights, Christmas Chocolate, Total Outlets, 9 week period ending December 28 2024 4. Suzy 2023– Christmas Survey n=300, Shoppers 18-65 who bought Chocolate at the Holidays 5. NielsenIQ Discover, XMAS INCL (EVDAY SEAS EXCL JR) BOXED Chocolate, National GDM + RFC + C&G, 9 week period ending December 28 2024 6. Suzy – Christmas Survey n=300, Shoppers 18-65 who bought Chocolate at the Holidays

The Canadian Chocolate market is well-established and a steadily growing industry, that saw +2% growth in $ sales in 20241. With Chocolate so synonymous during the holidays, key seasonal peaks, such as Valentine’s Day, Easter, Halloween, and Christmas contribute significantly to overall sales of the Chocolate market2. During these times, the Chocolate industry is often greeted with seasonally-specific graphics, limited-time formats, or limited-time offerings during key holidays.

Established Items

Source: Nielsen Market Track. XMAS INCL (EVDAY SEAS EXCL JR). 9 week period ending December 28 2024. NATIONAL EX NFLD GB + DR + MM + RFC + C&G

Boxed is the Biggest Format at Christmas with Shoppers Buying for Gifting, Hosting and Treat Occasions

Source: Suzy 2023 – Christmas Survey n=300, Shoppers 18-65 who bought Chocolate at the Holidays Q14 - Do you always give chocolate as a gift at the holidays? Q15 - Why did you decide to purchase Chocolate as a gift this year? Q13 - When gifting chocolate this Holiday Season, did you gift the chocolate with another item or just gift on its own?

Chocolate Continues to be a Key Gift at Christmas

Source: NielsenIQ Discover XMAS INCL (EVDAY SEAS EXCL JR), 9 week period ending December 28, 2024. NATIONAL EX NFLD GB + DR + MM + RFC + C&G EASTER SEAS CHOC, 12 week period ending April 6 2024, NATIONAL EX NFLD GB + DR + MM + RFC + C&G VAL INCL (EVDAY SEAS), 5 week period ending February 24 2024, NATIONAL EX NFLD GB + DR + MM + RFC + C&G HLWN SEAS + EVDAY SEAS JR, 13 week period ending November 9 2024, NATIONAL EX NFLD GB + DR + MM + RFC + C&G

Christmas Is The Biggest Season of the Year for Chocolate

Breakfast

Culinary Salt

Protein Snacks

Specialty/Global

Salad Dressings

Frozen Food

Personal Care

Canned Tomatoes

Plant-Based

CONFECTIONERY/SEASONAL CHOCOLATE

2025 CATEGORY CAPTAINS

KEY CATEGORY INFORMATION

1

3

2

BACK TO HOME PAGE

Nearly two-thirds of Canadian households purchase Chocolate during the Christmas holiday3, making Christmas the largest $ sales driver of category sales during the year. Chocolate remains a popular Christmas gift, with 1 in 2 people choosing to give it during the holiday season4. Boxed Chocolate represents 62% of total seasonal category $ sales5, making it the most loved form of Chocolate during the holidays. In particular, Boxed Chocolate is a favourite for gift-giving, for hosting or for sharing during a party, or even as a self-indulgent treat during the festive season6.

As a retailer, stocking up on leading-brand Boxed Chocolates will provide your shoppers with options for all their holiday special moments.

Top Reasons Why Shoppers Buy Boxed Chocolate at the Holidays

4

Non-Alcoholic Beverages

Source: Suzy – Christmas Survey n=300, Shoppers 18-65 who bought Chocolate at the Holidays Q4 – And now, for each of the reasons you just mentioned, please select the chocolate format/s you purchased for each of those occasions

Sales

8.3%

30.7%

21.5%

39.6%

$63.4M

$234.9M

$144.1M

$302.5M

Valentine's Day 2024 Easter 2024 Halloween 2024 Christmas 2024

85% gift Chocolate every year

Chocolate is Universal 67% gift because everyone likes it

1 in 2 people gift it on its own

Total Christmas $ Sales: $302.5M

$350M $300M $250M $200M $150M $100M $50M $0M

Boxed Novelty Pieces Bars Singles Multi Junior King Size

$1.9M (0.6% $ Shr)

$2.3M (0.8% $ Shr)

$6.6M (2.2% $ Shr)

$18.2M (6.0% $ Shr)

$39.1M (12.9% $ Shr)

$48.0M (15.9% $ Shr)

$186.5M (61.7% $ Shr)

$26.8M (8.8% $ Shr)

ADVENT

Gifting

Hosting

Self-Indulgence/ Gifting

62%

56%

41%

To give as a gift to adult family or friends

Hosting or sharing at large gathering/party

As a gift for myself

Confectionery

(Under $1 M)

2025 CATEGORY CAPTAIN

The Mayonnaise and Sandwich Spreads category represents a $423.5MM market, currently growing, with dollar sales up 4.5%, and sales pounds up 2.1%.1

Source: NielsenIQ Panel On Demand Homescan | CA - KRAFT HEINZ - MAYO & SPOONABLE DRESSING - 13 Facts of VISCOUS, MAYO (MAYONNAISE), SSD (SPOONABLE SALAD DRESSING) for Total Outlets in Total Canada during 3 52 Weeks Rolling, 2 Years, YTD - 34 w/e 23/08/25

Household Penetration, Viscous

Source: NielsenIQ Retail Measurement | CA - KRAFT HEINZ - VISCOUS - 5 Facts of 7 Products in NATIONAL EX NLFD GDM + GM+WC during 3 52 Weeks Rolling, 2 Years, YTD period ending July 26, 2025

Viscous $ Sales Growth

VISCOUS

$405,148,832

$423,552,434

$377,501,849

Mayonnaise remains the dominant segment with 83.0% of category share and has gained share each of the past two years. Much of the Mayonnaise category’s growth has been driven by the increasing importance of flavoured items (+74.7% sales pounds vs. 2023).1

Penetration of Mayonnaise is 69.1% and has seen consistent year-over-year growth in household reach.2 While inflation has contributed to Mayonnaise’s growth, the category’s slight increase in pounds per buyer indicates potentially stronger consumer engagement. Additionally, the repeat purchase rate has risen to 73.4%, reflecting improved loyalty and sustained demand.2

2024

2023

MAYO

SSD

+8.8%

+1.4%

+6.7%

-4.7%

+7.3%

+4.5%

66.2%

67.9%

69.1%

29.7%

27.8%

25.4%

78.5%

79.1%

78.4%

OVERALL VISCOUS

SSD: Spoonable Salad Dressing MAYO: Overall Mayonnaise

Sources: 1. NielsenIQ Retail Measurement | CA - KRAFT HEINZ - VISCOUS - 5 Facts of 7 Products in NATIONAL EX NFLD GDM + GM+WC during 3 52 Weeks Rolling, 2 Years, YTD period ending July 26, 2025; 2. 13 Facts of VISCOUS, MAYO (MAYONNAISE), SSD (SPOONABLE SALAD DRESSING) for Total Outlets in Total Canada during 3 52 Weeks Rolling, 2 Years, YTD - 34 weeks ending August 23, 2025 Demographic Total Panel People People Group

Source: NielsenIQ Retail Measurement | CA - KRAFT HEINZ - VISCOUS - 5 Facts of 7 Products in NATIONAL EX NFLD GDM + GM+WC during 3 52 Weeks Rolling, 2 Years, YTD period ending July 26, 2025

$ and $ Changes vs. YA

$423.5

MAYONNAISE

SPOONABLE SALAD DRESSING

TOTAL VISCOUS

BASE MAYONNAISE

FLAVOURED MAYONNAISE

$351.4

$72.1

$290.7

$60.7

$405.1

$329.5

$75.7

$280.9

$48.5

+3.5%

+25.0%

(in $ millions)

Sales Volume and % change vs YA

122.7

98.6

24.1

87.4

11.2

120.1

-5.2%

+2.1%

+4.1%

+1.7%

+27.1%

94.7

25.4

85.9

8.8

SPOONABLE SALD DRESSING

(in millions of sales pounds)

$ Share Per Segment

TOTAL MAYONNAISE 83%

SPOONABLE SALAD DRESSING 17.0%

BASE MAYONNAISE 68.7%

FLAVOURED MAYONNAISE 14.3%

OVERALL

$ Change L3Y

Household Penetration

$275,316,003

$245,674,252

$245,591,994

69.8%

Source: NielsenIQ Retail Measurement | CA - KRAFT HEINZ - PEANUT BUTTER - 5 Facts of 18 Products in NATIONAL EX NFLD GDM + GM+WC during 3 52 Weeks Rolling, 2 Years, YTD period ending July 26, 2025

CONVENTIONAL PB

NEXT TO FRESH & DELI

Source: 5 Facts of 18 Products in NATIONAL EX NFLD GDM + GM+WC during 3 L52W Rolling, 2 Years, YTD period ending July 26, 2025

PEANUT BUTTER

Peanut butter's role as a staple in Canadian diets is underscored by strong penetration at 66.5% of households,2 with equally robust repeat rates, with 71.4% of buyers returning, highlighting habitual consumption and loyalty across the category.2 According to NIQ’s Category Shopping Fundamentals survey, consumers are increasingly guided by health-oriented attributes, particularly: natural ingredient profiles, reduced or no sugar content, and the absence of artificial additives. These preferences are likely contributing to the sustained momentum in the Natural segment, signaling a gradual shift in consumer expectations toward cleaner labels and perceived better-for-you options.

The Canadian peanut butter category is valued at $347.6 million,1 holding steady in dollar sales with a modest -0.3% decline in pounds sold in 2025. Conventional peanut butter (excluding Natural) continues to anchor the segment with 78.3% share,1 though it faces gradual year-over-year dollar volume declines. Natural peanut butter remains a category growth driver, posting +3.3% in dollar sales and increasing share to 21.7%.1

$51,646,028

$53,010,882

$55,101,617

NATURAL PB

67.4%

66.5%

Sources: 1 NielsenIQ, NAT GB+DR+MM, L52W period ending May 18, 2025; 2 NielsenIQ Retail Measurement | CA - KRAFT HEINZ - PEANUT BUTTER - 5 Facts of 18 Products in NATIONAL EX NFLD GDM + GM+WC during 3 52 Weeks Rolling, 2 Years, YTD period ending July 26, 2025

Sources: 1 Caddle Cheese Shopping Insights, March 2023; 2 NielsenIQ, All Channels, Natl L52W period ending Dec 30, 2023; 3 Mintel Canada, Cheese, 2022

Canadians take their cheese seriously, with 86% saying that cheese is a planned purchase.1 Packaged cheese is by the far the largest segment within the category, representing a 60% dollar share or $3B and growing at +5%.2 Most consumers are making their cheese purchases at grocery stores – with an even split between channels: 48% of consumers buy at conventional grocery and 47% buy at discount. Within the grocery store, most consumers are purchasing from the dairy section, however 1/3 are also purchasing from the deli counter and another 1/3 are purchasing from dedicated cheese counters.3

FRESH & DELI

2024 CATEGORY CAPTAINS

Expanded occasions – the versatility of cheese will be its winning factor. The vast array of domestic and imported varieties fulfills all need-states and occasions.

Cheese has not been immune to ongoing pricing concerns, but the pièce de resistance of this category is its flexibility between nourishment and indulgence.

Source: NielsenIQ, All Channels, Natl L52W period ending Dec 30, 2023

Familiar flavours – flavoured cheeses are an important segment to the category, but consumers will reach for familiar before unique flavour innovation. Familiarity is a safe buying strategy, especially for specialty cheeses.

Variety for occasion – cheddar continues to hold a large share of our fridge deli drawers, but curious consumers are open to trying different varieties. Domestic artisanal brands are showcasing stellar cheeses. Meanwhile, access to imported cheese varieties from abroad allows for global exploration.

Base: 1,901 internet users who eat cheese Source: Kantar Profiles/Mintel April, 2022

Dairy section of grocery stores (i.e. where cheese is pre-packaged)

Deli counters in grocery stores

Dedicated cheese counters in grocery stores (i.e. sells artisanal cheese)

Where Cheese Is Typically Purchased

Cheese Ticks the Boxes on Both Nourishment and Indulgence

Cheese makes meals/snacks more nourishing

Cheese makes for an indulgent treat

% agree

As a category, one of cheese's biggest advantages is it meets a variety of needs. The vast majority of Canadians view cheese as being both a nourishing and indulgent option when deciding what to eat. As the category looks to grow in a heavily penetrated market, increasing frequency offers more opportunity. In this respect, cheese's versatility is its biggest asset.

NATURAL CHEESE - EXACT WEIGHT NATURAL CHEESE - EXACT WEIGHT DELI CREAM CHEESE - EXACT WEIGHT NATURAL CHEESE - RANDOM WEIGHT PROCESSED CHEESE SLICES COTTAGE CHEESE GRATED CHEESE PRODUCTS

3,073,162.1 909,617.7 353,842.6 249,813.7 248,764.4 144,349.6 100,667.7

+5% +6% +9% -7% +6% +18% -5%

433,464.0 107,491.0 74,454.3 7,187.5 49,873.1 28,905.9 10,524.7

+1% -1% 0% -9% +1% +9% -10%

Cheese Performance in Canada

$ (000)

$ Change vs YA

Units (000)

Unit Chg vs YA

90% agree

83% agree

2024 CATEGORY CAPTAIN

Source: Mintel Canada, Cheese, 2022

NEXT TO PROTEIN SNACKS

BACK TO CULINARY SALT

Sources: 1 Mintel, Future of Animal Proteins, 2024; 2 Canadian Grocer GroceryIQ Study, 2024; 3 Mintel, Snacking Motivations, 2024

Within the Protein Snack category, meat snacks have continued to demonstrate consistent year-over-year growth in Canada, fueled by consumers' desire to ensure they are getting enough protein in their diet.

PROTEIN SNACKS

Meat Snacks encompass more than just Beef Jerky. Although Jerky represents over 60% of the category, we continue to innovate to provide a variety of protein types, flavours and formats (meat sticks, tender bites, steaks & combos) to meet all consumer and shopper preferences.

Canadians are turning to snacks with protein in their quest for healthier food options.

46% of Canadian consumers agree they can't get enough protein without eating animal meat.1

Consumers are increasing their snacking, with 22% snacking 3+ times a day, and 63% at least somewhat agree that a few snacks can be more satisfying than a meal.3

Trends in product innovation, coupled with consumers’ focus on prioritizing nutritional snacking, will continue to fuel the growth of Meat Snacks in Canada.

Meat Snacks, as a Category, Continue to Deliver Sales Growth

$213 MM

$221 MM

$231 MM

$250 MM

2022

2026*

Source: NielsenlQ MarketTrack. National All Channels. Total Meat Snacks Trended sales L52W period ending July 13, 2024. * Projected Sales

Although consumers face mounting expenses, they prioritize categories offering potential long-term health benefits.

Protein is considered the most important nutrient, and most Canadians think of meat as the main source of protein.

Canadians are turning to snacks with protein in their quest for healthier food options.1

Meat Snack Segments and Formats

Jerky & Nuggets

Meat Sticks

Meat & Cheese Combos

Steaks & Bars

26%

64%

6%

4%

Source: 1 SimplyProtein/Maru Public Opinion online panel survey, February 8, 2023

Source: NielsenIQ. National Grocery, Drug & Mass Merchandise + Convenience WCGM. L52W period ending May 18, 2024

NEXT TO SPECIALTY FOODS

BACK TO FRESH & DELI

Nearly 1 in 4 health conscious grocery store shoppers indicated that they are interested in the protein content of the foods they purchase.2

Meat Snacks Continue to Attract New Shoppers

Meat Snacks attracted +200,000 additional Canadian households to purchase the category in 2023. Shoppers are spending more and putting Meat Snacks in their basket more often.

More Buyers

More $ Per Buyer

More Trips Per Buyer

3.4 Million Households

+200,000

Source: Nielsen Homescan. Market Summary. 52 weeks to Feb. 2024. Total Outlets. Total Meat Snacks

Sources: 1 Mintel Canada, August 2024

Base: 2,000 internet users aged 18+ Source: Kantar Profiles, August 2024

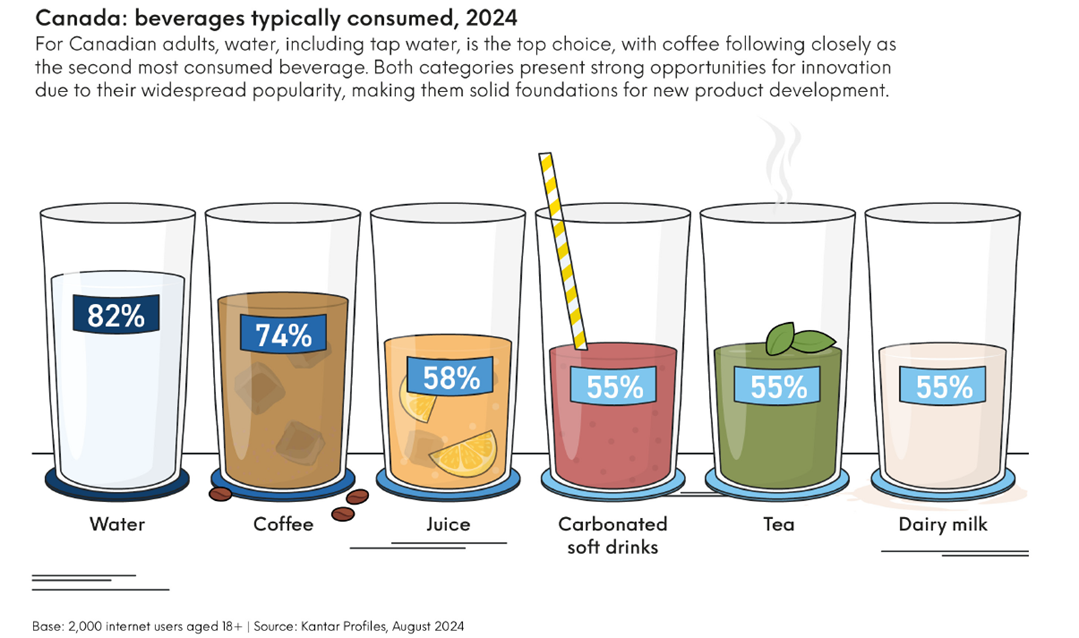

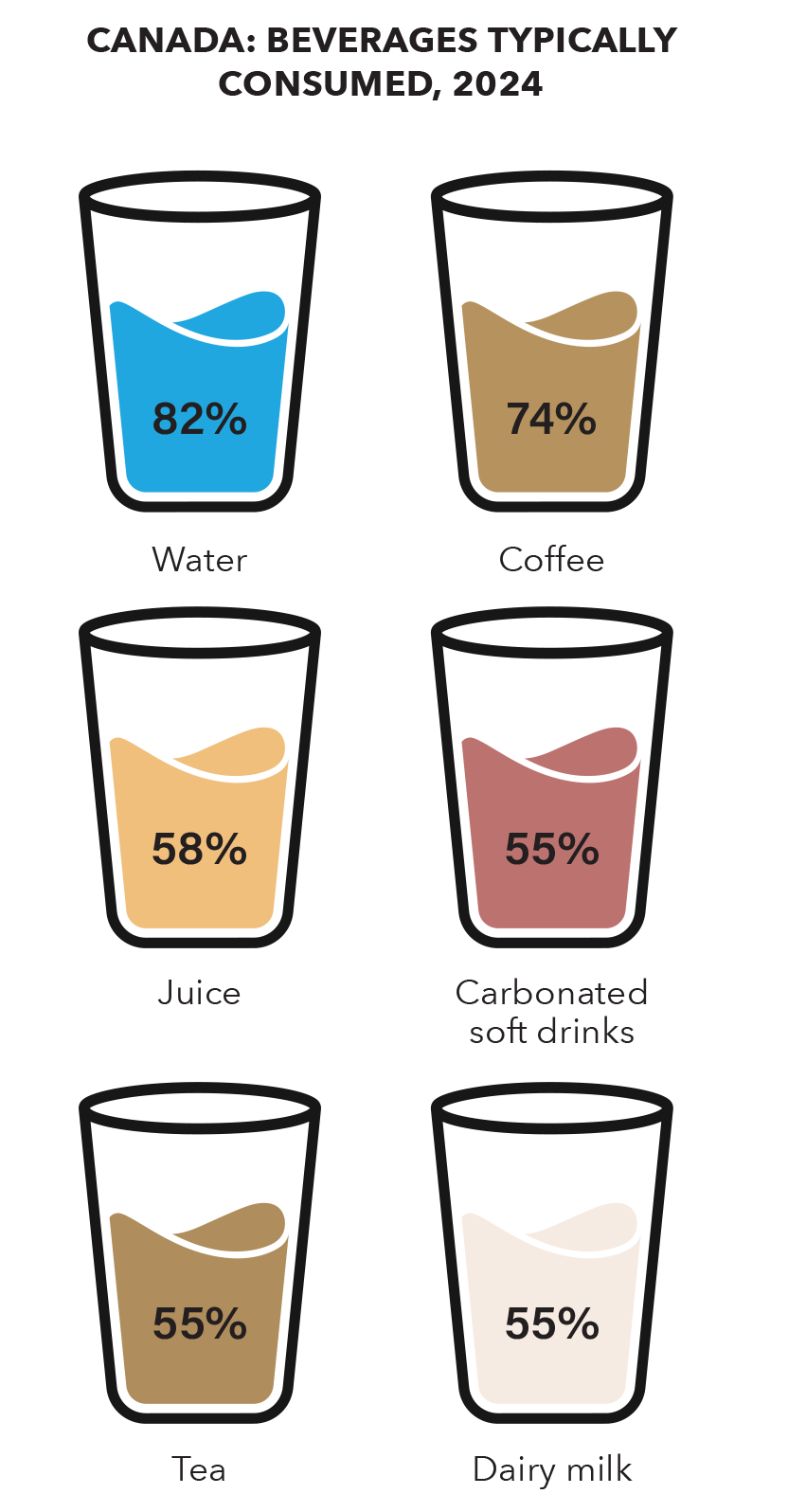

Canada: Beverages Typically Consumed, 2024

Beverage is a cornerstone category, continually evolving with the flow of culinary trends. Not surprisingly, water and coffee are the beverage of choice for almost all Canadians with near universal penetration.1 Despite consumers closely managing grocery budgets, they continue to make allowances for natural, healthier beverage options. The #1 beverage claim by Canadians is lower/no sugar, followed closely by “made with real ingredients”. Sharing stories about how ingredients are sourced and the people behind them provides an avenue to showcase such attributes and highlight brand authenticity as well as transparency.

This consumer demand has produced innovation focused on hydration, a back-to-basics approach of replenished electrolytes as part of overall healthy living. Building on this functional trend, consumers are seeking clean, quality and “real” ingredients that provide additional nutritional benefits. In response to the GLP-1 phenomenon the inclusion of added protein, macro nutrients and functional botanicals will fuel ongoing innovation.

Source: Mintel Canada, August 2024

Canada: Claims that matter when choosing non-alcoholic beverages to drink, 2024

Low/no sugar Made with "real" ingredients Low calorie Boosts energy Added vitamins Supports digestive health Strengthens immunity Promotes relaxation Added calcium Promotes focus Plant-based

percent of customers

42

32

29

28

22

18

16

12

9

percent of consumers

Water Hybrid/fusion drinks Sparkling water Energy drinks Sports drinks Non-dairy milk Tea Coffee Juice Dairy milk Carbonated soft drinks

More often

The same

Less often

45

31

30

26

25

20

19

53

54

59

49

55

61

63

66

64

68

24

14

15

13

Canada: Drinking beverages more often, the same or less often versus last year, 2024

BACK TO PROTEIN SNACKS

BEVERAGE

For Canadian adults, water, including tap water, is the top choice, with coffee following closely as the second most consumed beverage. Both categories present strong opportunities for innovation due to their widespread popularity, making them solid foundations for new product development.

0%

20%

40%

60%

80%

100%

58

10%

30%

Sources: 1. NielsenIQ, National All Channels, L52W Period Ending July 13, 2024; 2. NielsenIQ Panel On Demand Homescan Data, L52W Period Ending July 13, 2024; 3. Erickson Research, Peanut Bureau of Canada – Canada (2024)

With annual household penetration at 67.8%,2 Canadians continue to consume peanut butter in their diets, perceiving it as a healthy, convenient, on-the-go option that satisfies hunger and provides an energy boost.3 With multiple usage occasions, Canadians continue to use peanut butter as a spread (77%), ingredient in dishes (45%) or even straight out of the jar (28%).3 Peanut Butter continues to offer an affordable solution to evolving consumer needs, making it key for retailers to offer a variety of Brands to meet them.

Peanut Butter continues to be a household staple for Canadians, reaching annual sales of $351 million.1 While the total category has experienced inflationary dollar growth of 6%, tonnage volume has declined slightly by 2%.1 The category is led by Regular (Stabilized) Peanut Butter, accounting for 81% of sales across the category and experiencing dollar growth of 7% vs year ago, while the Natural Peanut Butter segment represents the remaining 19% of total category with annual dollar growth of 2%.1 Creamy Peanut Butter continues to be the preferred Peanut Butter sub-segment of consumers (68%), followed by Crunchy (19%), Light (12%), and Dark Roast (1%).1

Total Dollar Volume and % of Dollar Share

Source: NielsenIQ, National All Channels, L52W Period Ending July 13, 2024 Note: Creamy and Crunchy calculations exclude overlap of Light and Dark Roast Sub-Segments

Creamy

Crunchy

Light

Dark Roast

$236,792,526

$65,125,490

$42,663,009

$5,135,263

67.7%

18.6%

12.2%

1.5%

Peanut Butter Sub-Segments

Source: NielsenIQ, National All Channels, L52W Period Ending July 13, 2024

Total Peanut Butter Dollar Volume

80.6%

$283,176,854

19.4%

$68,026,059

$351,202,913

Natural Peanut Butter

Regular Peanut Butter

Peanut Butter Segments, Dollar Volume and Dollar Share

L52W 2YA

$306,018,347

$330,060,419

57,061,381

60M

40M

20M

0

$350M

$300M

$250M

$200M

$150M

55,771,549

54,421, 861

L52W YA

L52W

$ Volume

Tonn Volume (kg)

Peanut Butter 3-Year Trend

Sources: 1 NielsenIQ, TOTAL National - L52W period ending Aug 17 2024 & Cal-Year 2022 & 2023 2 NielsenIQ, TOTAL National - BMO TOTAL OUTLETS - L52W period ending Jul 27 2024 & Cal-Year 2022 & 2023 3 NielsenIQ, TOTAL National - L52W period ending Aug 17 2024 4 Ipsos FIVE 12ME February 2024 | % Occurrences – Total Food Universe

Pourable Salad Dressings are primarily consumed at meal occasions led by dinner, and routinely used with over 60% consuming it three or more times per week4. Since 2020, household penetration continues to decline as consumers are dissatisfied with the additives and lack of flavour in current offerings, turning to homemade dressings for simpler, customizable ingredients. While salads remain the top host food, consumers are expanding consumption to non-traditional occasions such as dipping with creamy dressings and marinating with vinaigrettes4.

Pourable Salad Dressings (PSD) is a $316MM1 mature category with a +3.4% 2-year CAGR and an average household penetration of 71.7% over the last 2 years2. The category is comprised of two major segments, refrigerated and shelf stable dressings (SSD), where SSD represents two-thirds of the category. In the last 52 weeks, PSD has seen a continued rise in dollar sales vs. prior year while overall product consumption declines (-3.0% pounds vs. last year)3 – this is due to two factors, rise of inflation and growth of premium smaller/restaurant brands.

2024*

*Note: Year to date, August 17, 2024 Source: NielsenIQ, TOTAL National - L52W period ending August 17, 2024 & Cal-Year 2022 & 2023

Dollar Sales ($)

$295,138,383

$315,264,376

$315,666,765

75,146,987

75,104,053

72,856,507

Volume in Pounds (lbs)

80M

70M

75M

$320M

$280M

Dollar Sales Growth But Decline in Pounds Due to Inflation & Premiumization

Importance in Both Shelf Stable & Refrigerated Segments

Shelf-Stable Share

Refrigerated Share

66.3%

33.7%

33.8%

33.5%

*Note: Year to date, August 17, 2024 Source: NielsenIQ, TOTAL National - BMO TOTAL OUTLETS - L52W period ending July 27, 2024 & Cal-Year 2022 & 2023

% of household penetration

2021

74.6%

72.5%

71.8%

70.8%

SALAD DRESSINGS

Sources: 1 Mintel, Dairy & Non-Dairy Milk - Canada – 2023 2 Mintel, Dairy & Non-Dairy Milk - Canada – 2023 3 Mintel, Milk and Non-Dairy Milk US Databook – 2023

Products that highlight high or added protein are especially appealing, as seen with launches that mix plant-based ingredients to boost protein levels and the continued leadership of soy as a plant-based protein.1 Soy, a high-protein plant-based food, considered a complete protein containing all nine essential amino acids, is leading the category with +1.9% $ sales growth in the latest 52 weeks. Plant-based offers reduced sugar and calories compared to dairy-milk, with reduced sugar being a commonly sought after attribute in new product launches.3

Nutritional quality of plant-based beverages is increasingly important, with consumers seeking products that offer added vitamins, minerals, and protein. Shoppers are motivated by the quality and presence of added nutrients and clean ingredient labels, and there is a growing expectation that plant-based drinks should match or exceed the nutritional benefits of dairy milk.1

Source: Nielsen, Marketrack, National Incl. NFLD GB +DR +MM, L52W period ending July 13, 2024.

Source: Nielsen, Marketrack, National Incl. NFLD GB +DR +MM L52W period ending July 13, 2024.

$ Share of Segment

Coconut/Almond 1%

Cashew 3%

Oat 27%

Dairy-Like 2%

Coconut 5%

Soya 15%

Almond 46%

Active Health 20.3%

Rice 1%

2012

2013

2014

2015

2016

2017

2018

2019

2020

L52 2023

Total Plant-Based Beverages

Almond

Oat

Soy

Blends

Dairy-Like

50%

PLANT-BASED BEVERAGES

Price continues to be a driving consideration—both as a motivator for purchase when it decreases and as a barrier when non-dairy options are perceived as too expensive.2

17.1% +1.2% $57,814,991

SOY

4.4% -0.1% $14,857,433

COCONUT

2.25% -0.2% $8,286,012

CASHEW

1.8% -0.2% $6,128,057

DAIRY-LIKE

1.0% +0.4% $3,261,056

ALL OTHER

44.2% -2.4% $149,361,432

ALMOND

28.5% +1.2% $96,404,225

OAT

0.6% 0.0% $1,972,862

RICE

Importance of Segment

Source: NielsenIQ Retail Measurement | CA - DANONE - SOYA & RICE DRINKS | Facts of ALL PLANT-BASED, 9 DA BASE in NATIONAL INCL NFLD GB +DR +MM during Latest 52 Weeks

Sources: 1 Mintel, Identifying New Opportunities for Coffee Creamers – 2025; 2 Nielsen MarketTrack, National Inc NFLD GB +DR +MM, L52W period ending August 9th, 2025; 3 Mintel, Coffee & Coffee Shops – Canada – 2025

Flavoured Coffee Creamers category growth of +8.4% $ sales ranks among the highest growth categories within Refrigerated Dairy, as the total Refrigerated Dairy department posts +4.9% $ growth in the Latest 52 weeks.2 Canadians are highly receptive to new coffee experiences, with a strong interest in flavoured creamers and unique flavour profiles. This openness is particularly pronounced among younger generations, who are more likely to experiment with new products and seek out creative coffee options, including flavoured and plant-based creamers.3

Overall, the growth of Flavoured Coffee Creamers in Canada is propelled by consumer demand for variety, innovation, plant-based and functional options, and the ability to customize the coffee experience, all amplified by urban lifestyles and social media trends.1

Segmentation & Shifting

Traditional

Dairy Cream 49.9%

Coffee Creamers & Flavourings 50.1%

68%

32%

Source: Nielsen, MarketTrack, National Incl. NFLD GB+DR+MM – L52W period ending September 7, 2024

July 2021

June 2022

June 2023

June 2024

28.8%

32.3%

33.1%

33.2%

L52W Growth: +4.7%

L52W Growth: +7.4%

L52W Growth: +3.5%

$391M

$393M

COFFEE CREAMERS

Refrigerated Coffee Creamers which hold a 90.4 $ shr of total creamers, are posting strong growth of +5.7% $ sales, with both Traditional +5.9% $ and Plant Based +5.1% $ sales. Non-refrigerated Coffee Creamers (9.1 $ share) are also finding success in the latest 52 weeks with +27.3% $ growth led by Barista Shelf Stable Creamers, posting gains of +25.2% in the last 52 weeks on increased Total Distrinbution Points (TDP’s) of +25.5% and increasing $ Sales per Point of Distribution (SPPDP) of + 21.9%.2

There is a notable demand for plant-based creamers, especially in provinces like Ontario and British Columbia, where consumers are more likely to prefer dairy alternatives. This trend is influenced by demographic factors, such as a higher population of individuals of Chinese background, who show a strong preference for plant-based options. Newer Canadians, in general, are more interested in plant-based and protein-enriched creamers compared to established Canadians.3

# OF BUYERS

VALUE PER OCCASION

# OF OCCASIONS

5,336,044

5,203,769

51,615,825

48,910,947

$7.88

$7.65

+2.5%

+5.5%

+3.0%

Facts on Coffee Creamers, Flavoured - Canada

Source: NielsenIQ Panel On Demand Homescan | CA - DANONE - COFFEE CREAMERS | 11 Facts of COFFEE CREAMERS - FLAVOURED for Total Outlets in Total Canada during L52W period ending June 9, 2025

L52W ending 6/9/24

L52W ending 6/9/25

Sources: 1 Nielsen MarketTrack, National Inc NFLD GB +DR +MM, L52W period ending August 9th, 2025; 2 Mintel, Yogurt and Yogurt Drinks – Canada – 2024

Yogurt has seen another breakout year in Canada fueled by increasing household penetration, hitting 88.9% in the latest 52 weeks +0.4 pts1 and growing consumer demand. The category has experienced a noticeable shift to premium segments providing value-added and functional benefits. The category is among the fastest growing within Refrigerated Dairy in the latest 52 weeks at +11.5% $’s and +6.0% EQ (equivalized tonnage).1

Rolling 52 w/e June 18, 2022

Source: Nielsen Homescan, National Incl. NFLD GB +DR + MM, rolling 52W period ending June 15, 2024.

88.2%

88.6%

Household Penetration (%)

90%

85%

Household Penetration Rate (Last 3 Years)

Source: Nielsen, National Incl. NFLD GB +DR + MM, L52W period ending September 7, 2024.

Light 4.2%

Indulgent 6.5%

Absolute Change in Sales $

Absolute $ Growth of the Segment

The primary motivation for increasing yogurt consumption among Canadians is the pursuit of a healthier diet. Consumers are seeking yogurts with specific health benefits, such as high protein, digestive health, and immune-boosting properties. Functional benefits and natural ingredients, including real fruit and locally sourced dairy, are especially appealing to health-conscious Canadians.2

Half of Canadian yogurt consumers are willing to pay more for yogurt that offers added health or functional benefits, such as high protein content.2 Younger consumers are driving this willingness to pay for extra benefits including functional health. Nearly half (45%) of Canadian yogurt consumers consider "high in protein" an important health-related factor when choosing yogurt or yogurt drinks. This demand is part of a broader trend where protein is prioritized for its role in supporting muscle health, satiety, weight management, and overall balanced diets.2 The two largest segments within the Yogurt category benefit from these trends with High Protein Yogurt hitting a 39.9 $ share, on +27.4% $ growth and Gut Health holding the #2 spot at 19.2 $ share with +1.8% $ growth.1

YOGURT GREEK INCL SKYR ACTIVE HEALTH KIDS REGULAR INDULGENT LIGHT ORGANIC PLANT-BASED ALL OTHER

113,720,886

164,727,754

14,674,871

1,655,685

12,285,629

17,883,297

-172,725

2,503,865

-281,161

2,457,408

Regular 15.8%

Kids 13.8%

Greek Including SKYR 34.5%

Plant Based 2.0%

Organic 2.5%

Other <1%

Rolling 52 w/e June 17, 2023

Rolling 52 w/e June 15, 2024

YOGURT

EVERYDAY NUTRITION

GUT HEALTH

INDULGENCE

KIDS

PLANT BASED

PROTEIN

Importance and $ Growth by Segment

$440,535,099 +$17,555,354

$415,636,943 +$5,060,992

$879,434,157 +$188,874,624

$41,571,901 +$2,725,506

$267,397,795 -$3,398,289

$140,144,976 +$15,642,365

40.9%

20.2%

19.0%

6.4%

1.9%

Source: NielsenIQ Retail Measurement | CA - DANONE - YOGURT | 3 Facts of ALL YOG, 8 DA SEGMENT in NATIONAL INCL NFLD GB +DR +MM during L52W period ending September 23, 2025

Sources: 1 NielsenIQ - NATIONAL EXCL NFLD GB +DR +MM - L52W Period Ending May 31, 2025 2 NielsenIQ – National All Channels - L52W Period Ending May 31, 2025

The Canadian egg market including shelled, hard-boiled, liquid, and liquid replacement products represents a $1.6 billion category in Canada.¹ Although shelled egg growth is the largest driver of egg performance, all forms of eggs such as hard-boiled and liquid eggs both grew +8% in dollars vs YA. (Figure 1)

Source: NielsenIQ - NATIONAL EXCL NFLD GB +DR +MM - L52W Period Ending May 31, 2025

Figure 3: Tonne Equivalent % Change

Source NielsenIQ – National All Channels - L52W Period Ending May 31, 2025

Figure 2: Total Eggs

Total Population

Figure 1: $ % Change vs. YA

BREAKFAST

Pickled

8%

1%

Liquid & Replacement Eggs

Shelled

PT. Chg. vs. 2022

+1.0

+0.6

-0.2

-1.4

% Chge

Pt. Chg. v. 2022

+0.3 -0.7 +1.1 +0.2 -0.6 -0.4 +0.2 +1.0 -0.6 -0.5 +0.7 0.0 -0.1 +0.5 -0.1

32% 25% 25% 19% 15% 12% 10% 8% 8% 7% 4% 4% 3% 3% 3%

6's

+0.5 -2.4 -3.1 +0.3 -2.3 +0.4 +1.0 +0.7 +0.5 -0.3 0.0 +0.4 +0.1 +0.1 +0.1

46% 14% 12% 2% 13% 12% 8% 7% 4% 2% 2% 1% 1% 1% 0.3%

EGGS

Shelled eggs has a wide consumer appeal as evidenced by over 92% of Canadian households purchasing a shelled egg product. 2 Despite being a mature sector, which typically experiences limited expansion, the category has shown significant growth of +$139MM or +9.5% vs last year. This trend is driven by shoppers increasing their amount spent on eggs by an average of 6.6% on each shopping trip. (Figure 2)

It's not just revenue that’s growing in the category. Canadian consumption of eggs has increased as tonnage (dozens) is up by 4%. Consumers are clearly moving to larger sizes as both 24 packs and 30 packs have grown tonnage by 37% and 33% respectively. Contrast that by declines in 6’s and 12’s at -15% and -5%. (Figure 3)

Another consistent trend in the category is the growth of specialty eggs. Conventional eggs have grown tonnage by +3% where specialty eggs grew +6% driven by all segments. (Free run +20%, Free range +9%, Omega +8%, Organic 12%) ¹

Unlike most categories, local / provincial brands are important and represent a sizable share of category dollars. Local / Regional egg brands represent a 29.9 dollar share of the shelled eggs category and are growing +9.9% vs nationally branded eggs which represent 12.1 share of dollars and growing at 2.6%. (Figure 4)

Figure 4: Dollar Share

Total Shelled Eggs

% Chge in Buyers

% Chge in $'s Buyer

% Chge in $'s Trip

% Chge in Trips/Buyer

12.1%

1.8%

10.1%

6.6%

-3.2%

8's

12's

18's

24's

30's

All Others

-15%

-5%

37%

33%

-38%

Regionally Branded Eggs

Nationally Branded Eggs

C/L Eggs

100

29.9

12.1

57.9

9.5%

9.9%

2.6%

10.9%

% $ Chg

Sources: 1. Shopper Intelligence, Coffee Category Decision Factors Importance, 12 months ending Q1, 2024. 2. Mintel, The Sustainable Consumer, Canada, December 2023. 3. Coffee Association of Canada, Coffee drinking trends, (n=1,503), December 2023.

The Coffee category has seen continued value growth over the past year, fueled by the rising demand for instant coffee, espresso capsules, and ready-to-drink beverages across grocery stores, drugstores, and mass merchandisers. While traditional coffee and K-Cup® pods remain key stable segments, meeting consumer needs for innovation1, sustainability2, and affordability1 is critical for driving further expansion. Over the last 52 weeks, larger K-Cup® pod formats have gained popularity as consumers navigate economic pressures and tighter budgets. The latest Coffee Association of Canada study reveals that many are stocking up on coffee to manage inflation3. Highlighting sustainability and promoting value-driven messaging will help unlock additional growth opportunities.

Source: 2023 Q4 Shopper Intelligence Grocery Survey, Decision factor importance rank 1 to 10

Rising Influence of Younger Coffee Drinkers (16-34 yrs.)

Source: Coffee Association of Canada, Coffee drinking trends, (n=1,503), December 2023

Coffee Shopper Behaviours

Source: Nielsen NATIONAL EX NFLD GB +DR +MM, L52W period ending June 15 2024, Espresso Caps are compatible Nespresso capsules sold at retail.

Coffee Annual Value

COFFEE

Coffee Disc

$563M

$500M

$73M

$35M

Espresso caps

K-Cup Pods

Traditional Ground

$168M

$233M

$81M

Total Coffee Annual Value $2,661M / +6%

Traditional Beans

Instant

Ready to Drink Coffee

This group is more likely to make unplanned purchases, with

of them indulging in spontaneous buys.

21%

61%

of consumers are stocking up on at-home coffee when it's on sale

of consumers started buying larger packages of at-home coffee to save money

42%

+0%

+39%

-17%

-2%

+2%

+7%

+6%

Sources: 1. Nielsen: Category Performance, National incl NFLD all channels, PE June 14, 2025, units per person = Total Frozen units / Canadian Population (41.8 MM) 2. IPSOS Canada Chats 2025, December 2024; 3. IPSOS Canada 5W, 5YR ending June 2025. Younger Generations = Gen Alpha, Gen Z, Millennials

Despite ongoing economic pressures and changing routines, Canada’s frozen food category continues to show remarkable resilience. In the latest 52 weeks, total tracked frozen food sales surpassed $8.8 billion, with per capita consumption climbing to 32 units per person per year1.

Source: Mintel, May 2025

Top 10 Frozen Motivations

Source: IPSOS FIVE R12ME August 2024 – % Food /Commercial Beverage Occasions; IPSOS Canada Chats, 2025, December 2024

Where Food is Sourced From

Source: Nielsen: Category Performance, National incl NFLD all channels L52W period ending June 14, 2025

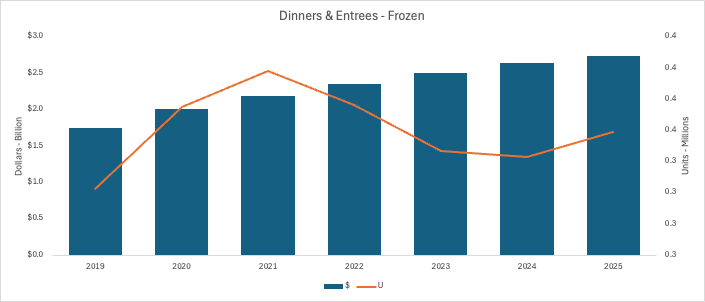

Dinner & Entrees – Frozen

Frozen dinners and entrées, the category’s largest segment, has surged with a 7.7% dollar CAGR, now reaching $2.7 billion in sales. In the latest 52 weeks sales rose +2.3% reflecting strong consumer demand for convenient, high-quality meals1.

A major driver is the shift in where meals are sourced. Retail accounts for over 84% of eating occasions, similar levels seen during the pandemic in 20202. While a 1% increase from 2023 may seem minor, it reflects a meaningful return to at-home dining. Frozen foods are well-positioned to meet this shift, offering value, convenience, and versatility—consistently cited as top purchase drivers3.

With overall frozen food sales and units rising, families with kids (43% of frozen occasions), multicultural households (27%), and younger generations (49%) remain key contributors to category strength, together accounting for a major share of frozen food occasions3.

Innovation is also driving excitement, with globally inspired meals and better-for-you options expanding the aisles. In fact, 24% of food occasions are motivated by a desire for healthy or nutritious choices2. Both Gen Z and Millennials tend to opt for more multiculturally-inspired dishes, underlining the appetite for exploratory taste preferences and cuisines2.

As Canadians continue to balance busy schedules and evolving tastes, frozen foods are set to remain a trusted staple in households from coast to coast.

FROZEN FOODS

Easy to prepare/little or no planning Satisfies my hunger Wanted something tasty Comforting Good value for the money Satisfies a craving Could be eaten quickly Wanted something all the household members... Good to share with friends/family Could be made with items on-hand

34%

27%

25%

23%

19%

18%

Sourced from Retail

Sourced from Foodservice/AO

70%

81%

84%

86%

83%

16%

14%

17%

Dollars - Billions

Units -Millions

$3.0

$2.5

$2.0

$1.5

$1.0

$0.5

0.4

0.3

$

Units

Sources: 1. Mintel Canada, May 2025 2. Nielsen, Exact Weight + Random Weight, NATIONAL EX NFLD GB +DR +MM L52W period ending July 26, 2025

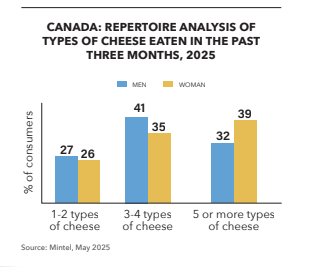

Underscoring its central role in Canadian diets, not only is Cheese consumed by 94% of households but the category continues to show strong growth year over year.1 In total, the category represents $3.7bn, with Exact Weight cheese representing a 94% share.2 Exact Weight, also known as Prepack, is growing +4% in dollars and +2% in volume.2 At least 2/3 of consumers have eaten at least 3 types of different cheese in the last 3 months, confirming that at-home deli drawers hold multiple varieties – and consumers are willing to add additional staples to their rotation.1

Source: Nielsen, Exact Weight, NATIONAL EX NFLD GB +DR +MM during L52W period ending July 26, 2025

Exact Weight, Dollars

Exact Weight – Top 8 Specialty Segments

Specialty cheese is the largest segment, representing 1/3 of the category. Specialty cheese is continuing to show robust growth of +9% in dollars and volume – an indicator that, despite consumers watching grocery prices, there is still significant demand for this segment.2 The top cheese specialty cheese types are Feta, Cheddar and Paneer – a clear reflection of Canada’s evolving demographic.

CHEESE

FETA CHEDDAR PANEER MOZZARELLA & BURRATA SPREADABLE BLOOMY/WASHED RIND PARMESAN GOUDA & EDAM

$111,655,469 $86,464,612 $69,188,378 $68,673,482 $66,093,072 $62,736,700 $45,623,403 $33,090,174

4% 10% 18% 8% 7% 7% 4% 15%

13,831,969 9,068,832 13,068,234 8,739,591 10,356,199 7,947,178 5,666,424 4,325,640

4% 7% 21% 8% 4% 8% 0% 15%

DOLLARS

DOLLARS CHANGE

UNITS

UNITS CHANGE

SPECIALTY

31%

13%

7%

BLOCK

SNACKING

SHREDDED

SLICES

SPREADABLE

DEHYDRATED

Canada: Repertoire analysis of types of cheese eaten in the past three months, 2025

% of consumers

1-2 types of cheese

3-4 types of cheese

5 or more types of cheese

Men

Women

27

41

35

39

Sources: 1. NielsenIQ - National EXCL NFLD GB +DR +MM - L52W Period Ending May 18, 2024 2. NielsenIQ – National All Channels - L52W Period Ending May 18, 2024

In Canada, Eggs in all forms (Shelled, hard boiled, liquid and liquid replacement eggs) is a $1.5B dollar category1. Mature categories rarely generate significant growth yet Canadian consumers have increased total Egg sales by $111.8MM (+8%) vs the same time last year. The value added segments are also contributing to total egg growth (Figure 1).

Source NielsenIQ - National EXCL NFLD GB +DR +MM - L52W Period Ending May 18, 2024

Figure 3 - Average Unit Price

Source: NielsenIQ - National GB+D+MM L52W Period Ending June 29,2024

Figure 2 - $ Sales, $ Share and $% Change

Source: NielsenIQ - National EXCL NFLD GB +DR +MM - L52W Period Ending May 18, 2024

Figure 1 - $ % Chg vs YA

More households are purchasing Shelled Eggs (buyers +2%) and those households who purchased last year are spending more ($’s per HHLD +5.8%).2 (see Figure 4) This trend isn’t surprising as consumers are looking to larger pack sizes in the category to find value. Both 18 Packs (+13%) and 30 Packs (+33%) have increased their share of Eggs significantly versus a year ago.1

Shelled Eggs are the largest segment accounting for 97% of total Egg sales and growing +8%.1 From coast to coast, Shelled Eggs are generating more revenue for retailers. (see Figure 2) It is important to understand segment development for the east vs west to address regional consumer demands.

Although Conventional Eggs (no additional claims) make up the largest share of Shelled Eggs (76.8 dollar share & +9%), Specialty Eggs have been growing significantly as well (23.2 dollar share & +6%).1 Free Run Eggs have been a primary driver of Specialty Eggs growing +14% vs year ago.1 This trend is positive for building bigger baskets in the category as Specialty Eggs retail at a higher price per unit vs Conventional Eggs. (see Figure 3) Optimizing the category requires keeping up with trends on larger packages while offering a strong range of specialty products.

Source NielsenIQ – Homescan - National All Channels - L52W Period Ending May 18 2024

Figure 4 - Shelled Eggs