Awareness

Report

Awareness

HOMEOWNERS COVERAGE

A home represents more than just a financial investment — it’s a source of pride, comfort and long-term security.

But as risks evolve, from lawsuits to cyber threats to inflation, protecting that investment often requires more than a standard policy. Meanwhile, many homeowners may not realize where gaps in coverage exist. That’s

KEY FINDINGS

Coverage defined

Umbrella

A form of liability insurance �that provides extra protection �beyond the limits of a home �or auto policy

Cyber

Insurance that helps individuals recover from financial losses �and other impacts caused �by cybercrimes

VALUABLES

Insurance that protects �high-value personal belongings — such as jewelry, art and collectibles — against loss, theft or damage

RECREATIONAL

VEHICLES

Specialized protection for a wide range of vehicles used for leisure — such as motorcycles, boats, off-road vehicles and collector cars

Awareness versus discussion

The survey started by establishing the level of customer awareness on four specific insurance coverage options: umbrella, cyber, valuables and recreational vehicles. This included determining how many have this coverage.

In the case of valuable items insurance, the survey showed a far greater number of homeowners were familiar with this coverage option (87%) than have the coverage itself (26%).

The next question in the survey was included to assess homeowners’ knowledge of how their valuables are protected without specialized coverage.

Awareness versus understanding

The survey also asked homeowners how they prioritize their insurance purchasing decisions, ranked from absolutely essential to not at all important.

Customer purchasing priorities

How familiar are you�with the following?

83%

23%

46%

7%

94%

20%

26%

87%

UMBRELLA

CYBER

VALUABLES

RECREATIONAL VEHICLES

Aware

Aware

Aware

Aware

"I have this insurance today"

"I have this insurance today"

"I have this insurance today"

"I have this insurance today"

With the exception of cyber, homeowners reported a high level of awareness of these insurance coverage �options. Nonetheless, awareness has not translated into wide-spread adoption.

The survey then asked a follow-up question to determine whether homeowners were approached by their agents or insurance companies to discuss these options.

Has the company/agent �you get your homeowners insurance from ever talked �to you about any of the �following coverage?

In each case, the majority of homeowners reported they have not discussed these options with their �insurance agent or company, despite the fact that each are designed to protect against risks nearly every modern homeowner faces.

These gaps highlight the importance of the expertise and guidance independent insurance agents can provide to homeowners.

61%

said no

87%

said no

55%

said no

45%

said no

UMBRELLA

CYBER

VALUABLES

RECREATIONAL�VEHICLES

Many homeowners appear to be under the impression their current policies offer more protection than they actually do. For example, only 19% understood how basic home coverage would apply in the scenario outlined above (partially covered after the deductible).

Misconceptions like this underscore the critical role agents play in educating homeowners about what is and is not covered under a standard policy. It also highlights the importance of adding valuable items to insurance policies instead of relying on standard home insurance coverage.

Basic homeowners insurance comes with an amount of �coverage for valuable items. �If you lost a $10,000 ring �in a house fire, how do you �think basic home insurance �would cover it?

13%

31%

8%

19%

29%

NOT COVERED�OR NOT SURE

PARTIALLY COVERED�AFTER DEDUCTIBLE

PARTIALLY COVERED�NO DEDUCTIBLE

FULLY COVERED�AFTER DEDUCTIBLE

FULLY COVERED�NO DEDUCTIBLE

While many factors play into a customer’s decision about coverage, customer service was the one most frequently considered important, followed by flexibility for coverage to be tailored to their unique needs.

These findings further reinforce the value homeowners place on having a single insurance company for all their policies, where homeowners can get a high level of customer service and work with one team for all their needs. This also provides other benefits, such as discounts for bundling policies, and the convenience of having one login and one number to call in the event of a claim. It also helps reduce potential gaps in coverage.

How important are each �of the following to you when selecting your personal �insurance? (Percentage �of responses of "absolutely �essential" or "very important")

81%

74%

58%

58%

EXCELLENT CUSTOMER SERVICE

ONLY PAY FOR�WHAT I NEED

CONVENIENCE OF ALL MY INSURANCE WITH ONE COMPANY

LOWEST PRICE

The importance of conversation

Homeowners face a growing number of risks that aren’t addressed by a basic home policy, making it all the more important for customers to talk with their agents about their evolving risks and build insurance plans that can help protect them, their income and their assets. Keeping coverage together with one carrier can also help more easily identify potential gaps, and provide a more consistent customer service experience.

THE DIFFERENCE

an independent insurance agent can make

Independent agents do more than recommend coverage — they serve as trusted advisers who build relationships with homeowners to understand the unique risks they face. When agents proactively discuss all available coverage options with homeowners, it helps them make informed decisions and avoid costly gaps in protection.

The best insurance companies go beyond offering coverage. They provide educational resources, partner with agents to raise awareness and offer solutions to ensure homeowners receive trusted guidance and total account protection for true peace of mind.

the right insurer can make

THE DIFFERENCE

The Hanover Insurance Group, Inc. is the holding company for several property and casualty insurance companies, which together constitute one of the largest insurance businesses in the United States. The company provides exceptional insurance solutions through a select group of independent agents and brokers. Together with its agent partners, The Hanover offers standard and specialized insurance protection for small and mid-sized businesses, as well as for homes, automobiles and other personal items. For more information, please visit hanover.com.

~ Daniel C. Halsey, President, Personal Lines at The Hanover

While there is high awareness of umbrella insurance among homeowners, a much smaller percentage (only 23%) currently have an umbrella policy.

The survey then sought to gauge the level of potential interest homeowners might have in umbrella insurance based on a deeper understanding of what it does.

Awareness versus interest

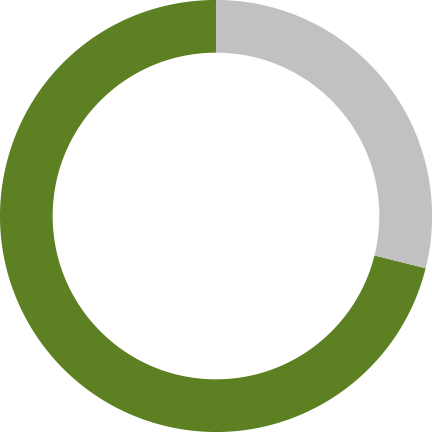

These results reveal that, with this additional context, 2 in 3 homeowners would be interested in umbrella insurance, and likely open to a conversation with their insurance agents about this coverage.

If there was extra insurance that could help protect your savings, income or home in case of a serious accident or lawsuit — beyond what your auto or home insurance covers — starting at $1 million in coverage for about $30/month, how interested would you be in adding it?

VERY �INTERESTED

SOMEWHAT�INTERESTED

NOT VERY �INTERESTED

NOT AT ALL�INTERESTED

24%

42%

23%

11%

The Hanover commissioned The Harris Poll to conduct a survey of U.S. homeowners1 ages 30 and up to gain greater insight into homeowners’ knowledge of personal insurance, including umbrella, cyber, valuable items and recreational vehicles coverage to determine the level of awareness they have of these insurance options.

These findings suggest consumers may find great value in the consultation offered by an independent insurance agent, who can serve as a trusted adviser and facilitate important conversations around risk and protection.

Service �IS VITAL

Customer service is a top priority when choosing insurance coverage.

False sense of security

Homeowners often believe they have more protection than they actually do, leaving them vulnerable.

Unaware of key coverage

Many homeowners don't recall hearing about essentials like umbrella insurance — even though they’re open to it.

~ Daniel C. Halsey, President, Personal Lines at The Hanover

Homeowners face a growing number of risks that aren’t addressed by a basic home policy, making it all the more important for customers to talk with their agents about their evolving risks and build an insurance plan that can help protect them, their income and their most valuable asset. Keeping coverage together with one carrier can also help more easily identify potential gaps, and provide a more consistent customer service experience.

Survey method

About The Hanover

This survey was conducted online within the United States by The Harris Poll on behalf of The Hanover from Aug. 12–14, 2025, among 991 adults ages 30 and older who own a house. The sampling precision of Harris online polls is measured by using a Bayesian credible interval. For this study, the sample data is accurate to within +/-3.8 percentage points using a 95% confidence level. For complete survey methodology, including weighting variables and subgroup sample sizes, please see below for press contacts.

Abby C. Ursoleo

aursoleo@hanover.com

508-855-3549

Press contacts

Emily P. Trevallion etrevallion@hanover.com

508-855-3263

All products are underwritten by The Hanover Insurance Company or one of its insurance company subsidiaries or affiliates (“The Hanover”). Coverage may not be available in all jurisdictions and is subject to the company underwriting guidelines and the issued policy. This material is provided for informational purposes only and does not provide any coverage or guarantee loss prevention. For more information about The Hanover visit our website at www.hanover.com.

where independent insurance agents play a vital role: offering personalized guidance and expertise that help ensure homeowners are fully protected, today and into the future.

ABOUT THE REPORT

1Defined as those who own a house.

71%

COVERAGE FOR AS MUCH AS POSSIBLE