HOVER OVER IMAGES FOR DETAILS

Contact Us

Investmentweek.co.uk

Professionaladviser.com

MORE INFORMATION

Read more from Capital Group

Past results are not a guarantee of future results. The value of investments and income from them can go down as well as up and you may lose some or all of your initial investment. This information is not intended to provide investment, tax or other advice, or to be a solicitation to buy or sell any securities. Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. All information is as at the date indicated unless otherwise stated. Some information may have been obtained from third parties, and as such the reliability of that information is not guaranteed.

This material, issued by Capital International Management Company Sàrl (“CIMC”), 37A avenue J.F. Kennedy, L-1855 Luxembourg, is distributed for information purposes only. CIMC is regulated by the Commission de Surveillance du Secteur Financier (“CSSF” – Financial Regulator of Luxembourg) and is a subsidiary of the Capital Group Companies, Inc. (Capital Group), also authorised and regulated in the UK by the Financial Conduct Authority. © 2024 Capital Group. All rights reserved.

FOR FINANCIAL PROFESSIONALS ONLY

This material is a marketing communication

Regular insights on an asset class reborn

Scroll

Brought to you by

Six reasons for an active approach to emerging market debt

Read the article >

Emerging markets

Asset allocation

Fight not flight: history suggests switching from cash to bonds

Fixed income:

the renaissance

The stage is set: four sectors for those targeting income

Income investing

Four compelling strategies for a high-rate world

Attractive opportunity to add duration in non-USD rates

Global relative value

Global corporates: investors should focus on idiosyncratic opportunities

Corporate bonds

Four lessons from 50 years of bond investing

Asset management

VIDEO

Discover what has made us stand out from the crowd over the past 50 years

Hard and local currency bonds: a ‘cautiously constructive’ outlook

Professionalpensions.com

Is government spending offsetting monetary policy?

Macro insight

Distorted perceptions: high yield has vastly improved in quality

High yield

Don’t try to call the pivot – increase duration now

Watch the video >

FIXED INCOME

The best combination of return potential and resilience?

The signs on inflation are ‘really encouraging’

‘We’re expecting interest rate cuts to come in Q2 next year’

When peak rates create historic investor opportunities

Corporate and mortgage bonds offer compelling income opportunities

Asset outlook

‘Powerful income potential’: did you miss the healthy returns in high yield?

A tale of two markets: investing in a bifurcated EM universe

‘Rolling recessions’ and the implications for interest rates

Macro outlook

What a more dovish Fed means for emerging market debt

Fixed income tends to outperform cash when rate cycles have peaked, says Haran Karunakaran

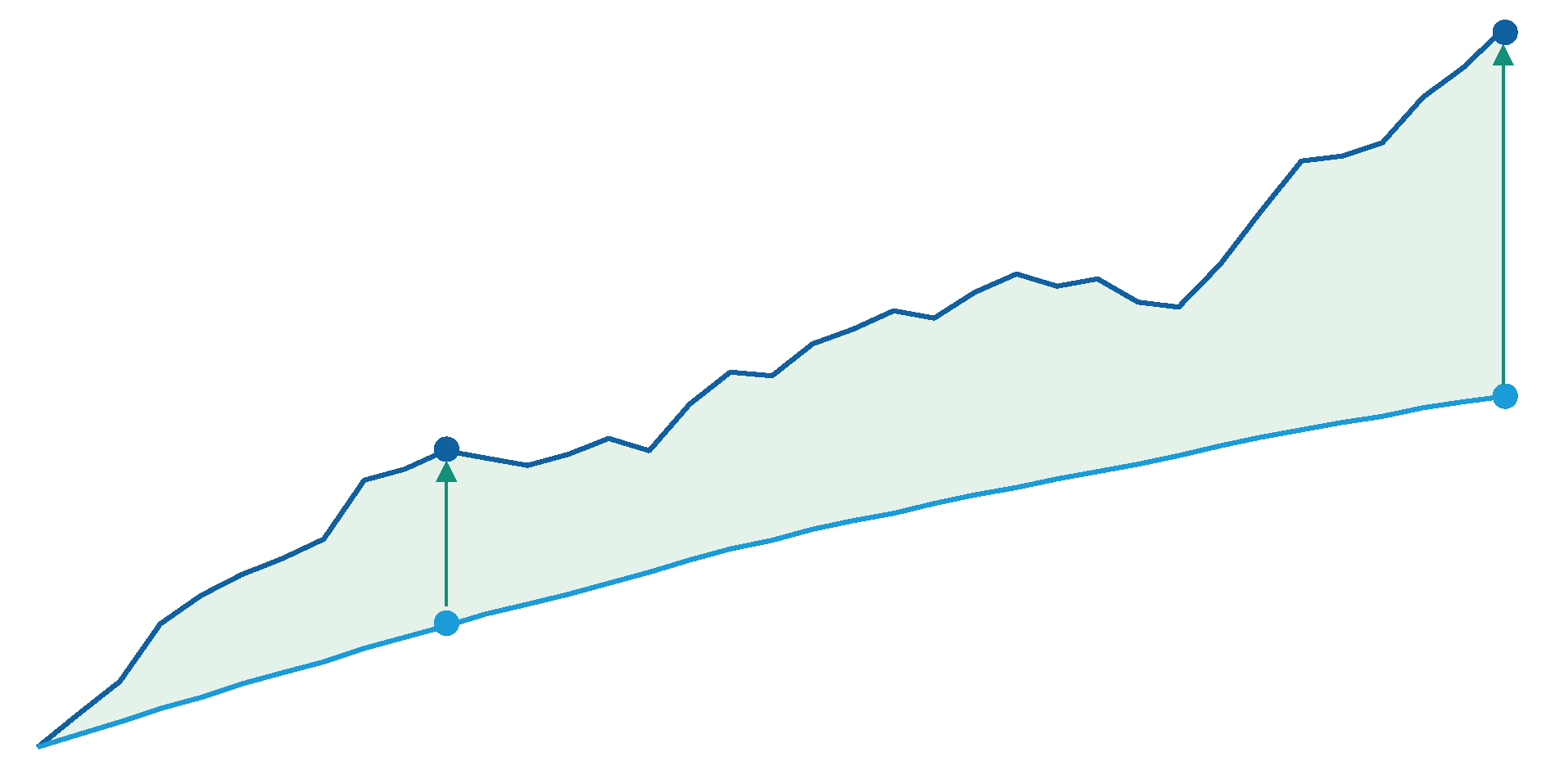

Historical analysis can provide useful guidance on how bonds and cash perform through different parts of the market cycle. As 2022 illustrated, a rising rate environment is bad for bonds; investors were clearly much better off in cash. But as rate cycles around the world move towards their peak, are we at an inflection point where it makes sense to shift back into fixed income? History would suggest the answer is yes. An analysis of every sustained US rate hiking cycle since the 1980s highlights some interesting patterns.

“Yields on cash-like instruments have tended to decay very quickly following the last interest rate rise of a hiking cycle”

Fixed income: the renaissance

Past results are not a guarantee of future results. Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. The information provided is not intended to be comprehensive or to provide advice.

Investment Director, Capital Group

Haran Karunakaran,

Lessons from history

2. Across all the periods in this analysis, the average time between Fed pausing further hikes to right before the first cut is approximately eight months.

1. ‘Cash’ yields decay quickly after the peak in Fed Funds rate The first point to note is that yields on cash-like instruments have tended to decay very quickly following the last interest rate rise of a hiking cycle. Over the last five rate hiking cycles, the JPMorgan Cash Index USD three-month yield was an average of 2.2% lower 18 months after the last US Federal Reserve (Fed) hike. This is because central banks typically step in with rate cuts to dampen any slowdown in the economy. As a result, investors in cash-like instruments such as term deposits and money market funds see their returns diminish quickly at this stage of the cycle.

“The key lesson for investors is to avoid the temptation of perfect timing and get invested sooner rather than later”

2

High inflation, geopolitical tensions, collapsing banks and ongoing concerns about recession have all combined to create a highly uncertain environment for investors. In the face of all this, it is no surprise that some may want to opt out of markets altogether. Sitting on the sidelines can feel like the safer option, particularly when “cash” is offering yields not seen in over a decade. However, this may be a detrimental strategy. Our analysis suggests that, over a multi-year horizon, investors are better served by a “fight” than “flight” response. Fixed income is the perfect tool for that fight. Indeed, it is in recessions when bonds shine: at such times, fixed income benefits from central banks cutting rates and can provide a powerful defensive hedge within a broader portfolio.

October 2023

2. The end of a rate hiking cycle is good for bonds High-quality fixed income has, on average provided stronger returns than cash-like investments following the peak of a rate cycle. Over a three-year time horizon, the gap between high-quality bonds (proxied by the Bloomberg US Corporate Bond Index) and a cash-like investment (proxied by the JP Morgan USD three-month cash index) is a cumulative 16%. That was the cumulative gain to an investor from shifting out of cash and into fixed income.

As central banks cut rates, high-quality bonds should deliver strong returns due to two positive forces:

Yield advantage: High-quality fixed income typically offers investors a higher yield than cash-like investments. Today, the yield advantage for US corporate bonds is between 0.5% and 1.5% (depending on which cash proxy you use). Over multiple years, this yield advantage compounds into a significant wealth difference for investors. Capital appreciation: As central banks shift from hiking to cutting rates, fixed income instruments benefit from price gains. For example, US corporate bonds today have a duration of around seven years. This means if yields were to fall by 1%, the bonds would generate a 7% capital gain. This is on top of the yield advantage the bonds may continue to earn.

• •

Essentially, by investing toward the peak of a rate cycle, bond investors can lock in attractive yield levels, which typically drive strong returns for years to come. By contrast, rates cuts are negative for investments in cash-like instruments. Consider an investor who can today access a three-month term deposit paying 4% per annum. As central banks rate cuts are priced in, this term deposit rate will likely fall — based on previous cycles, the initial 4% p.a. offered could end up at just 1.8% p.a. The term deposit investor’s realised return over a multi-year period will be much less than what they may have anticipated at the outset.

1

1. Based on the US Fed Funds Rates. Rates cycles captured 1988-89, 1994-95, 1999-2000, 2004-06, 2015-18.

Applying these lessons to the current environment

History rhymes but does not repeat. When we look forward, discussions among our fixed income portfolio managers and analysts tend to cluster around two potential scenarios, both of which are positive for high-quality bonds:

3. Time in the market matters With perfect foresight, an investor could align their shift into fixed income exactly with the peak point in the rate cycle. But our experience suggests this sort of market timing is difficult, if not impossible. Knowing this, is an investor better off being “too early” or “too late” in shifting out of cash and into fixed income? In prior rate cycles, the bulk of gains for bond investors came in the first 10 months after rates had peaked. This makes intuitive sense — rate cycles typically hit their peak when recession looms. Central banks react quickly to this, cutting rates (often aggressively) to dampen the economic downturn. This front loads a significant portion of the return advantage of fixed income. Our earlier analysis highlighted an average three-year cumulative return benefit of 16% from being in fixed income over cash. Half of this uplift happens within the first 10 months after the peak in rates (see previous chart) — waiting on the sidelines for too long risks missing this investment opportunity. The key lesson here for investors is to avoid the temptation of perfect timing and get invested sooner rather than later.

The economy remains resilient and central banks leave rates higher for longer. In this case, bond investors will continue to benefit from the current elevated yields and the premium offered over cash. The economy enters a significant recession and central banks aggressively cut rates in response. In this scenario, bonds would be expected to receive an additional return boost from falling rates.

2. 3.

A more negative scenario in the back of our minds is a re-acceleration of inflation, which could lead to rates rising and spreads widening — essentially a repeat of 2022. This is likely a lower probability outcome, however. While still above central bank targets, inflation is on a clear downward trajectory and the full impact of the past 18 months of interest rate hikes has not yet flowed through the economy. Additionally, weakness in the financial system has likely raised the bar for further significant hikes. While another hike or two from the Fed is certainly a possibility, another 500 basis points is less likely. Additionally, it is worth noting that, if this low-probability scenario did occur, the impact on fixed income returns would likely be more muted than in 2022. This is because yields are much higher today than at the start of 2022, providing a strong cushion against falling bond prices.

Data as at 30 July 2023. Sources: Bloomberg, US Federal Reserve. Chart represents the average decline in the JPMorgan Cash Index USD three-month yield starting in the month of the last Fed rate hike in the last five transition cycles from 1989 to 2018.

Average change in yield on “cash” after the peak in the Fed Funds Rate in previous hiking cycles

-2.21%

Cumulative returns from investing at the peak in the Fed Funds Rate in previous hiking cycles

For illustrative purpose only.

Source: Bloomberg. As at 30 June 2023 High quality bonds: Bloomberg US Corporate Bond Index, Cash proxy: JP Morgan USD three-month Cash Index Rate cycles captured 1988-89, 1994-95, 1999-2000, 2004-06, 2015-18.

SHARE THIS

CONTRIBUTOR

Back to hub

Read more

Learn about our distinctive, high-conviction approach

Upgrade your fixed income to a world leader

An effective multi-sector approach can incorporate US, emerging market and securitised credit, say Damien McCann and Flavio Carpenzano

In this article, we consider the outlook of four key sectors. The distinctive characteristics of each sector tend to complement each other; combining them could help target reliable income with an attractive risk/return profile.

“Higher-quality credit offers a potential cushion against any spread volatility ahead”

Securitised credit – under-researched, providing alpha opportunities

Although securitised credit is one of the smaller credit sectors, there are compelling opportunities within the asset class. Furthermore, securitised credit acts as an important diversifier given it has a lower correlation with corporate credit. Our preference for securitised credit exposure is within the higher quality space, with a focus on AA and A rated issuers. ABS is offering select investment opportunities. Valuations in certain segments of the market (subprime auto, rental car) appear to be pricing in a moderate recession while the more senior tranches can withstand a more severe downturn in the economy. While near-term volatility remains high, the current levels appear attractive with a focus on shorter duration bonds. Other areas of opportunity include residential mortgage-backed securities (RMBS), collateralised loan obligations (CLOs) alongside select exposures to auto and student loans. Concerns around fundamentals in the commercial real estate sector, particularly in office space, means we are more defensive on commercial mortgage-backed securities (CMBS) with a focus on AA and A rated tranches. We expect declining underlying property values to create attractive income- and total return-generating investment opportunities in 2023 and 2024.

1. As at 31 July 2023. US high yield market measure by Bloomberg US Corporate High Yield 2% Issuer Cap. Index.

“Securitised credit acts as an important diversifier given it has a lower correlation with corporate credit”

As rate cycles around the world move toward their peak, we could now be at an inflection point for fixed income. Credit markets offer fresh opportunities across sectors and with starting yields at levels between 5.5% and 8.5%, the stage is set for positive total returns over the longer term.

US high yield – potential for a higher level of income

Our focus in the US high yield market is currently on higher quality names given the potential for additional softening of economic growth. However, there are several technical factors supportive of the sector. The first is the absence of near-term large-scale refinancing requirements has meant new issuance is relatively low. This is coupled with higher credit quality; more than 50% of the US high yield index is in BB rated bonds. In addition, in absolute terms, yields currently on offer in the high yield market are at elevated levels compared with history. Proprietary, fundamental research is particularly crucial in navigating the risks within higher yielding sectors. We invest issuer-by-issuer and where we believe outcomes could be better than market pricing indicates. For example, exposure to high cash-generative and capital-lite business models that could benefit through the current rate environment, such as asset managers, financial exchanges, and brokerages. These companies have transaction-based revenue streams with attractive cash flow generation. The recurring revenue models from selected issuers within this segment would have the potential to do better than more cyclical issuers in a soft economy or a rising rate environment. The resilience of the US consumer has surprised some market commentators. We have seen this resilience play out through persistent strength in consumer spending in travel and leisure, which has supported issuers in cruise lines and the gaming sector. We also see strong potential for “rising stars” in the high yield market. These are issuers that currently hold a high yield credit rating but are expected to graduate to investment grade. We have identified companies in the automotive and pharmaceuticals sectors, where we believe select companies are poised to re-gain their investment grade rating over the coming 12 months. These rising stars offer attractive risk-adjusted returns due to the level of yield and associated risk.

US investment grade – higher quality though more sensitive to rates

Macro uncertainty has increased the potential for volatility for across investment grade markets. Credit spreads have tightened since March 2023, when the banking sector led spreads wider. With higher interest rates and expected slowing growth, credit fundamentals will likely be weaker over the remainder of 2023 and could elevate spread volatility. There remains, however, attractive opportunities within the sector and higher-quality credit offers a potential cushion against any spread volatility ahead. Defensive industries and issuers will likely outperform in more challenging economic conditions. An example is the pharmaceutical sector, which historically has outpaced the broader market in periods of market weakness. We anticipate that this relationship will continue to hold, with stable revenues and earnings across the sector. Idiosyncratic opportunities are also arising from greater spread dispersion. An area currently in focus is banking. Valuations of select global financial institutions and better-capitalised, larger US regional banks in senior tranches are not necessarily reflecting the underlying fundamentals and are priced at wider spreads than our analysis suggests is warranted. Select opportunities also present themselves in the utilities sector. This sector benefits from stable profitability due to regular and visible earnings. Furthermore, the investments utility companies have made to strengthen their distribution networks against natural disasters, such as wildfires, are being rewarded.

Emerging market debt – diversified sources of income and return

Bifurcation remains a theme within emerging market debt and warrants a selective approach. We tend to view investment grade rated EM countries as overvalued in the current environment as spreads look less attractive relative to investment grade corporates, as an example. We are currently finding more value in high yield-rated EM issuers. While there are some distressed EM credits, there are also many countries which are well positioned to navigate this environment and, in certain cases, valuations already reflect these risks. We’re finding value in Latin America where central banks have been more proactive than developed market counterparts in hiking rates to tackle inflation. Examples include several Latin American sovereigns in the high-quality investment grade rating cohort such as Mexico, as well as high yield rated issuers including the Dominican Republic, Colombia, and Paraguay. In addition, we see value in idiosyncratic stories such as Oman where we expect an upgrade in credit rating from BB to investment grade as the three rating agencies moved the country to a positive watch. This is alongside Oman’s progress on fiscal consolidation, debt reduction and continued efforts to increase non-oil revenues. In current markets, drawing on multiple views across the credit spectrum can be particularly powerful. In addition, flexibility in allocation is essential to balancing return and risks in different market environments.

8.0%

6.7%

7.8%

4.5%

Past results are not a guarantee of future results.

Yields and returns as at 31 July 2023 in USD terms. Sources: Capital Group, BloombergData goes back to 2004 for all sectors. Based on average monthly returns for each sector when in a +/- 0.3% range of yield to worst. Sector yields above include Bloomberg US High Yield Corporate 2% Issuer Capped Index, Bloomberg US Corporate Index, JPMorgan EMBI Global Diversified Index and Bloomberg CMBS Ex AAA Index.

Average five-year forward returns at recent yield levels (%)

Income opportunities have returned to fixed income

Fixed Income Investment Director

Flavio Carpenzano,

CONTRIBUTORS

Fixed Income Portfolio Manager

Damien McCann,

There are a variety of investment opportunities on offer as economies and central banks near a pivotal phase, say Damien McCann and David Daigle

Yields soared and bond prices tumbled in 2022 as elevated and persistent inflation pushed the Fed to raise rates at a breakneck pace. So far in 2023, volatility hasn’t been nearly as dramatic, but stubborn inflation has pressured the central bank to continue with more gradual rate increases. However, despite lingering uncertainties about the economy, one thing is clear: The rise in rates has created many paths to strong income and return potential in bond markets. That’s because starting yields have been a good indicator of long-term return expectations.

“If inflation continues to ease and economic growth remains sluggish, rates will likely decline somewhat from here, while remaining higher than investors have become accustomed to in recent years,” McCann notes. In that context, fixed income sectors may be attractive since bond prices rise when yields fall. And since the total return of a bond fund consists of income and price changes, “falling yields would be a tailwind for returns on top of the hefty coupon payments from bonds,” he adds. The surest path to falling yields — and potential price appreciation — is via rate cuts by the Fed. That could happen if inflation continues to fall, the economy enters a significant downturn, or central banks seek a “neutral” policy rate that neither restricts nor stimulates economic growth, according to Daigle. Falling Treasury yields would help offset the negative impact of wider credit spreads, or the incremental yields that bonds typically pay over Treasuries.

“Consumers continue to power the US economy, and while there has been some softening, trends remain encouraging”

1. Seek to capture attractive yields before rates fall

3. Look to high-yield bonds where stars appear aligned

For investors with a time horizon of at least a year, some risks may appear worth taking. So far this year, starting yields of around 8% have provided a buffer against bond market volatility tied to the Fed’s rate path. That in turn has helped support solid returns for the year-to-date period ended 29 August 2023, with the Bloomberg US Corporate High Yield Index posting a 6.81% gain. “Many companies in the high-yield market have adapted fairly easily to higher rates,” Daigle says. For example, several companies have paid down debt, thereby reducing interest expense. Lower leverage and improved operations have increased the number of “rising stars”, or companies that have been upgraded out of high-yield territory. According to Daigle, that trend is likely to continue.

“Many companies in the high-yield market have adapted fairly easily to higher rates”

David Daigle,

2. Consider investment-grade bonds while fundamentals are strong

The recession that was supposed to be here by now appears to be on hold. To be sure, there are weaknesses in various parts of the economy, but even areas sensitive to rising rates, such as housing, may be stabilising. “Consumers continue to power the US economy,” McCann says, “and while there has been some softening, trends remain encouraging with firm labour markets and steady consumer spending for leisure and travel activities.” Delinquencies for credit cards edged higher in the second quarter compared to the first three months of the year, but are not worse than pre-pandemic normalised levels, according to an August 2023 report from the Federal Reserve Bank of New York. Many companies have been able to pass on costs to consumers, which has bolstered corporate fundamentals, including profits. These companies have also worked to reduce operating expenses and are managing their cash conservatively. “That strategy should allow these companies to continue to refinance or repay their debt as earnings growth slows or contracts in a downturn,” McCann says. More opportunities are emerging across industries in investment-grade bonds. One area of potential value is large money-centre banks, where spreads are well above historic averages and the credit quality is excellent. “Recent troubles in the banking sector seem to be contained, and while banks overall have dialled back on lending, the contraction hasn’t yet been severe enough to push the economy into a recession,” McCann adds.

One challenge ahead is the potential consequence of high borrowing costs on companies. At some point, higher rates may lead to weaker credit profiles and lower valuations. “This process could be gradual rather than abrupt and investing in high-yield bonds today may help offset future volatility associated with a slowdown,” Daigle says. Any issuer facing a combination of higher funding costs and deteriorating earnings will likely have a difficult time refinancing its debt, underscoring the importance of a selective investment strategy. “This is not really an industry-level phenomenon,” Daigle concludes, “although there are issuers within the communications sector that appear particularly exposed.”

4. Diversify your income investments

A common investment strategy applies, even when rates are this elevated: diversify your holdings. For income-seeking investors, this includes investing across bond sectors that have been hard hit, such as emerging markets and securitised debt. Returns across investment grade, high yield, emerging markets and securitised debt vary over time. McCann believes a diversified, multi-sector approach can help investors navigate headwinds that impact parts of the economy unevenly. Several countries are having a tough time in this high interest rate, slow growth environment, but the net is wide in emerging markets and many issuers have been able to navigate these circumstances, according to McCann. For example, Oman has benefited from higher oil prices. Additionally, Latin American countries proactively lifted rates well before major central banks, which helped insulate economies by easing inflation and currency pressures. As markets continue to react to Fed moves, inflation and shifting narratives about the economy, investors should focus on long-term financial goals. “You can’t predict the future, so I always advocate for both a multi-sector approach and a long-term perspective,” McCann concludes. “I’m optimistic as rate hikes have set the stage for much stronger income and return from bonds in the years ahead.”

Sources: Bloomberg Index Services Ltd., RIMES. Data shown from July 31, 2013, to August 25, 2023. Sector yields above include U.S. aggregate represented by the Bloomberg U.S. Aggregate Index, investment-grade corporates represented by the Bloomberg U.S. Corporate Investment Grade Index, high-yield corporates represented by the Bloomberg U.S Corporate High Yield Index and emerging markets debt represented by the 50% J.P. Morgan EMBI Global Diversified Index/50% J.P. Morgan GBI-EM Global Diversified Index blend.

Yields of major fixed income sectors (%)

Strong income potential may persist as yields stabilise at elevated levels

Source: Capital Group, J.P. Morgan Global Research as of August 5, 2023

The stars are rising for high yield companies

Value of corporate debt that has been upgraded from/downgraded to high-yield status (USD billions)

Past results are not predictive of results in future periods.

An active approach to local currency emerging market debt offers no less than six potential advantages, say Edward Harrold and Jeremy Cunningham

“India is the last major emerging market country to not be included in JPMorgan’s local currency index”

Fixed income Investment Director

Edward Harrold,

“Local currency debt returns are driven by both duration and currency risk. An active approach can allow investors to separate and isolate these risks”

An allocation to emerging market debt (EMD) can offer investors a range of potential benefits – not least its low correlation with other sub-asset classes of fixed income. The growth dynamics and strengthening economic fundamentals of many emerging market (EM) countries are attractive to investors seeking growth, income and diversification. Here we discuss the potential benefits of an active allocation to local currency EMD. These include access to a wider source of returns, given the ability to take off-benchmark exposure and use multiple levers to capture different drivers of return and manage risk, and a more deliberate allocation of capital, which could mitigate unintended consequences of index construction. By contrast, an allocation to passive or smart beta strategies can provide an effective and low-cost way to access the broad market. However, these approaches can lead to exposure biased towards countries that are increasing their level of indebtedness and can also restrict opportunities to capture relative value through market movement. Interest rate and exchange rate volatility can at times be high. The following are a more detailed look at what we believe to be the six key benefits of an active approach in this area.

2. The ability to access off-benchmark exposure

India is the last major emerging market country to not be included in JPMorgan’s local currency index. As a result, foreign ownership levels are low. If added, India could represent 9.2% of the JPM GBI-EM Global Diversified Index, making it the second largest country in that index, after China. The impact of such high domestic ownership levels tends to be reduced volatility as the market is less prone to shifts in international capital flows. Furthermore, it is not only the level, but also the composition, of foreign ownership that can influence market risk and return characteristics. India has a higher percentage of ‘non-dedicated’ EM holdings, i.e. while dedicated EMD investors hold relatively less India exposure, global bond investors hold more. This is an interesting technical that, when considering the relatively low correlation of these markets to other local currency sovereign debt markets and currencies, can mean exposure to these markets acts as an effective diversifier within a local currency strategy.

3. A more deliberate allocation of capital

The starting point for the construction of an EMD benchmark remains the level of sovereign debt outstanding; exposure is typically to those countries with the most outstanding debt. While the diversification method applied by JPMorgan in its Global Diversified index mitigates this to a point, the level of debt remains its foundation and the index provider’s diversification methodology could even be considered to be an ‘active’ decision of itself. Furthermore, as index composition evolves and is rebalanced over time, the exposure provided by a passive strategy will shift accordingly. A passive investor therefore has limited control over the composition of exposure taken. For an active manager, this represents an opportunity to potentially increase exposure to the devalued market; a passive approach, however, is less able to capture such short-term dislocations.

Chart 2 highlights the range of FX volatility. As we have seen, while FX movement can have a significant impact on return, its contribution to volatility is commensurately high; and whilst rates volatility has declined recently, FX volatility has increased. As active management gives investors the ability to both choose the degree of exposure to selective currencies, and also to manage that through hedging, it becomes an effective tool in times of rising volatility.

1. Access to a wider source of returns

Perhaps the most important point is that adopting an active strategy to gain access to local currency EMD provides investors with the broadest possible investable universe. Certain benchmarks restrict the opportunity set available due to construction methodologies and constraints; this is logical, and indeed serves to facilitate active management by providing a useful reference point for risk management. The presence of widely adopted benchmarks also enables the comparison of results across managers in support of manager selection. However, a large proportion of the investable universe – close to 90% – is excluded as a result. This can be to the detriment of passive investors, as they are (perhaps unintentionally) restricted to exposure to only a limited sub-set of the local currency debt market, which has been pre-selected by the benchmark providers.

4. The technical impact of index criteria and rebalancing

The movement of countries into and out of both emerging market and global bond indices can have dramatic effects on the balance of market demand and supply. For example, since 2019, China has been pulled into the mainstream emerging market and developed market bond indices with a commensurate increase in foreign investment. The opening of a deep and liquid bond market, with positive real yields and low correlation to other major bond markets, offers investors potential opportunities to enhance returns as well as diversification. The Chinese market could represent both a broad opportunity set for active investors and a useful addition to an investor’s portfolio construction toolkit, offering relatively defensive and diversifying exposure. However, in order to provide the optimal mix of risk management and potential return generation, it is crucial to be able to take an active position on the level of exposure, and the most appropriate way to access opportunities.

5. Ability to use multiple levers to capture different drivers of return and manage risk

Local currency debt returns are driven by both duration and currency risk. An active approach can allow investors to separate and isolate these risks. While it might be expected that common factors would drive returns in both, there has been a divergence between the bond and currency components of the JPMorgan GBI-EM Global Diversified Index in recent years. Having the ability to take currency hedging positions on a case-by-case basis enables the investor to capture currency appreciation, manage exposure and mitigate potential depreciation. Even if a manager expects weakness in a particular currency, it still may not be the best approach to hedge because of the cost. A strongly positive view on a bond market combined with a moderately negative view on the currency may be more conducive to unhedged local exposure. A fully hedged or unhedged strategy would not always give the optimal outcome given the variation of returns within EM.

6. The ability to manage volatility and capture the opportunities that presents

With volatility more elevated across global rates markets since 2022, the enhanced ability to manage volatility offered by active strategies has assumed ever greater importance. While a focus on volatility at the market level can be helpful, it is interesting to note the wide range in shifts in volatility across individual markets. Chart 1 compares changes in volatility by local bond markets, over three months and one year.

As at 6 September 2023. Chg: change. Source: BlackRock Aladdin. ARS = Argentine peso, BRL = Brazilian real, CLP = Chilean peso, CNH = Chinese yuan, COP = Colombian peso, CZK = Czech koruna, EGP = Egyptian pound, EUR = euro, GBP = pound sterling, GHS = Ghanaian cedi, UF = Hungarian forint, IDR = Indonesian rupiah, ILS = Israeli shekel, INR = India rupee, JPY = Japanese yen, KES = Kenyan shilling, KRW = Korean won, MXN = Mexican peso, MYR = Malaysian ringgit, PEN = Peruvian sol, PLN = Polish zloty, RON = Romanian leu, THB = Thai baht, TRY = Turkish lira, UYU = Uruguayan peso, ZAR = South African rand, ZMK = Zambian kwacha.

Chart 1: 10-year local yields volatility – % change over 3 months and 1 year

Chart 2: FX volatility – % change over 3 months and 1 year

As at 6 September 2023. Chg: change. Source: BlackRock Aladdin.

% Change in 3M

% Change in 1Yr

Investment Director

Jeremy Cunningham,

These two types of emerging market debt are offering different routes to return, says Jeremy Cunningham

Hard currency Emerging market hard currency bonds are essentially a credit asset, typically offering a yield pick-up over US Treasuries (in the case of US dollar bonds) as compensation for taking on additional risk. Investors seek this extra yield to help cover losses that may arise from default and mitigate the risk of losing a portion of their initial investment. This yield differential includes a liquidity premium, which acts as insurance against not being able to easily convert the asset into cash as quickly as a US Treasury holding. As with investment-grade corporate bonds, this yield spread is chiefly influenced by changes in the credit profile of the issuing entity and by global fluctuations in investor appetite for risk. As emerging market economies evolve into developed markets, we can expect credit ratings to generally trend upwards (over the long term) and for spreads to come down. This has already happened with many emerging markets, especially those in Eastern Europe, while the more frontier markets, many of which are in Sub-Saharan Africa, tend to have lower levels of development, often higher idiosyncratic risks and generally higher spreads.

“We believe that emerging market currencies are well positioned to deliver positive returns relative to the US dollar due to undervalued exchange rates”

Drivers of return

We have developed a proprietary fundamental exchange rate model where a currency’s fundamental fair value is based on long-run trends in consumer prices and the relative price of non-tradable to tradable goods within each country. Based on this Fundamental Equilibrium Value Exchange Rates model (FEVER), we believe that the US dollar is overvalued. Although we have experienced some USD weakness in recent months, the big global picture dollar story remains unchanged until we see evidence of stronger global growth.

“Relatively strong macroeconomic fundamentals in the major EM countries, combined with high starting yields and undervalued exchange rates, should provide a buffer to any volatility”

Emerging market (EM) bonds are a strategic holding for many investors. But the desired result from an allocation to emerging market debt cannot be achieved without first considering the attributes of hard- and local currency-denominated bonds — the two broad sets of investments available in the asset class — and understanding some of the benefits each can bring to a portfolio.

Local currency Changes in domestic interest rates and shifts in the shape of the yield curve are the key drivers of return in local bond markets. Improving creditworthiness is a less prominent contributor to returns. Local currency bonds can carry added risk through currency exposure. As the chart shows, returns have been driven by income and the capital gain associated with yield compression rather than currency gains In other words, currency has been a major driver of volatility but not of long-term returns for the asset class. EM foreign exchange (FX) movements have generally reflected the US dollar cycle and risk sentiment rather than structural EM stories. Since the 2013 taper tantrum, EM FX has generally weakened against the US dollar, and has brought higher volatility with it.

An active approach to investing in local currency bonds can allow for hedging positions on a case-by-case basis, potentially allowing investors to capture currency appreciation, manage exposure and mitigate potential depreciation. Hedging costs need to be taken into account. A strong positive view on a bond market combined with a moderately negative view on the currency may be more conducive to unhedged local exposure if hedging costs are high. There are a few reasons why currency appreciation can potentially be a key source of return in the longer term. Emerging markets’ rising productivity and growth relative to the developed world, their improved terms of trade and their exposure to rising global commodities can be expected to serve as a magnet for investment inflows over the medium to long term.

Opportunities within dollar debt

Opportunities within the dollar-denominated space tend to be more idiosyncratic. While the current macroeconomic backdrop warrants caution as EM sovereign credits could be more vulnerable to a US recession, we find more attractive valuations among the higher-yielding countries on a selective basis. We are focused on issuers where we believe the risks may be overpriced or exposure could look to provide stability and resilience as part of a diversified fixed income portfolio, such as the Dominican Republic. Though valuations are less attractive across investment-grade sovereigns, we continue to find value in select lower-beta credits as a counterbalance to high yield positions, such as Mexico.

Local currency bonds look particularly attractive

We currently see the most value in Latin American countries, such as Mexico and Brazil, where interest rates have been raised early. This has helped keep inflation under control and has supported exchange rates. That said, select European sovereigns are starting to look attractive. We also believe that emerging market currencies are well positioned to deliver positive returns relative to the US dollar due to undervalued exchange rates and the Federal Reserve’s potential pivot away from additional policy tightening.

Our analysis has identified many exchange rates that appear fundamentally undervalued based on our FEVER model. A stable US dollar is a tailwind for investors allocated to local currency EM, as the strong carry characteristics serve to generate an attractive level of return.

An active approach

Looking ahead, the outlook for EM debt remains cautiously constructive. Global factors such as inflation and monetary policy, as well as US recession risks, are likely to continue driving emerging market debt for the remainder of 2023. While the global backdrop continues to look uncertain and could be a headwind for EM debt markets, relatively strong macroeconomic fundamentals in the major EM countries, combined with high starting yields and undervalued exchange rates, should provide a buffer to any volatility. In volatile market environments, an active, research-based approach to investing can really show its benefits. Our analyst notes that in the past, when restructuring has occurred (usually as part of an International Monetary Fund programme), the restructured debt has done well over the long term. That is because the final haircut is often far less than originally implied by the price action. Thus, selling in the downturn can lead to higher losses. This is especially problematic with passive strategies.

Data as at 9 August 2023. “Index” represents JPMorgan GBI-EM Global Diversified. Source: Bloomberg.

EM exchange rates versus the US dollar (January 2003 = 100)

Exchange rate valuations are near their cheapest levels since inception of the EM local currency index

Data is from 31 December 2002 to 7 August 2023. Returns in US$ terms, rebased to 100 as at 31 December 2002. JPMorgan GBI-EM Global Diversified Total Return Index, in unhedged US dollar terms. Source: JPMorgan.

Income has been the major source of returns for local currency bonds

As at 23 August 2023. Exchange rate valuation is using our proprietary FEVER model. COP: Colombian peso, MYR: Malaysian ringgit, MXN: Mexican peso, PLN: Polish zloty, KRW: South Korean won, ZAR: South African rand, BRL: Brazilian real, INR: Indian rupee, SGD: Singapore dollar, CLP: Chilean peso, THB: Thai baht, IDR: Indonesian rupiah, CNY: Chinese renminbi, CZK: Czech koruna, ILS: Israeli new shekel. Sources: Macrobond, Capital Group.

Real carry and exchange rate valuations

Many exchange rates seem undervalued on a fundamental basis

Bond yields are likely to remain higher for longer as the Fed stands firm, say Pramod Atluri and Anmol Sinha

“The market’s attention has seemingly shifted from falling inflation to the large fiscal deficit”

Portfolio Manager

Pramod Atluri,

“The deficit could be lower in 2024 than it is today, but it is still expected to remain near record-high levels”

In November, the US Federal Reserve (Fed) kept its benchmark interest rate unchanged for the second meeting in a row. That’s despite resilient economic data highlighting a stronger growth environment and the risk that inflation remains well above 2% for an extended period. Treasury yields have risen sharply since September after the Fed updated its “dot plot” forecast to show two fewer rate cuts in 2024 than the market had been expecting. Longer-dated bonds have taken the brunt of the pain: The benchmark 10-year Treasury yield has risen nearly 50 basis points since the dot plot was released on September 20 and briefly eclipsed 5% in October for the first time since 2007. So, what is driving this shift in yields? Surprisingly resilient growth has been a contributor, along with technical factors relating to higher expected Treasury issuance and stagnating demand. Markets are increasingly pricing in a view that the Fed will maintain a higher for longer stance — that is, rates broadly may remain at these higher levels for an extended period. Portfolio manager Pramod Atluri argues that high deficits, along with challenges to tighter monetary policy filtering through to the real economy, have helped bolster growth more than expected. Growth may continue to remain resilient as a function of more dominant fiscal policy, leading the Fed to maintain policy at restrictive levels for longer than markets expect. Importantly, investors should be mindful that financial market volatility likely persists even with resilient underlying economic growth. This should be an attractive market for fixed income, as higher yields can offer compelling income and return potential while also buffering against potential price volatility. There is also an opportunity for meaningful price appreciation should rates fall due to a growth shock. “The biggest risk to continued economic growth could be a combination of higher interest rates and a rapid decline in the Federal deficit,” Atluri says.

November 2023

Putting recent shifts in context

The market’s attention has seemingly shifted from falling inflation, which helped pull interest rates lower earlier in the year, to the large fiscal deficit and the government borrowing needed to finance it. These higher expectations for the supply of Treasuries have been exacerbated by constrained demand. The Fed’s ongoing quantitative tightening programme has reduced its holdings of Treasuries and other bonds while other traditional buyers of government debt such as banks, sovereign wealth funds and other non-US buyers may have also stepped away from the market for a variety of reasons. These factors are all contributing to higher term premiums and outsized moves on the longer end of the yield curve. The deficit is not only contributing to the increased supply of Treasuries, but also strong economic growth.

Getting fiscal: Is government spending offsetting monetary policy?

While the Fed has been moving to tighten policy rapidly, the federal budget deficit has increased from around 4% of gross domestic product (GDP) to around 8%. This is among the largest deficit increases in history, aside from COVID-19, World War II and the 2008 financial crisis, and it's happening when GDP is already growing. With fiscal and monetary policy moving in opposite directions, the net impact can be challenging for investors to discern. The extent of the increase in the deficit, along with the sheer size of it, have bolstered growth even as some sectors of the economy may have been — or are currently in — recession. Fiscal policy’s impact has also been bolstered because the traditional channels through which monetary policy impacts the real economy — housing, autos, household wealth effects and bank lending — may not be responding as expected to higher interest rates. In housing, demand fell with higher interest rates, but supply fell even more as a significant number of existing homeowners have mortgages well below prevailing levels. The result has been house prices actually rising, leading to robust construction activity. A similar dynamic has played out in autos, where the expected drag to this highly important economic sector has been less severe than expected given the amount of pent-up demand for autos post-Covid. Home prices rising and real wages growing (as inflation has fallen) have also helped support consumers instead of the usual household wealth effect, where rising rates lead to falling asset prices that constrain household wealth and ultimately consumer spending. Finally, bank lending has been affected less than expected as the large fiscal deficit from recent stimulus bills is helping boost household incomes and corporate profits, unlike typical cycles where rising delinquencies and defaults lead banks to increase reserves and reduce lending. To be sure, monetary policy works through “long and variable lags” in affecting the economy, but Atluri believes we should have already seen much more significant signs of stress in the most interest-rate-sensitive sectors of the economy. “If the transmission channels are impaired in the ways described above, it may help explain why economic growth has surprised to the upside and why the Fed may need to maintain restrictive policy for longer,” Atluri says.

Deficit-related spending likely to grow

The large fiscal deficit is likely to remain an important economic driver. The deficit could be lower in 2024 than it is today, but it still is expected to remain near record-high levels. The Congressional Budget Office (CBO) estimates that US budget deficits will continue to expand from there as the Infrastructure Investment and Jobs Act (IIJA) and Inflation Reduction Act (IRA) take effect. And this could even be an underestimation as the CBO assumes previously implemented tax cuts will be reversed in-line with legislation. The reality is these assumptions have rarely been accurate. Furthermore, the economic impact of upcoming fiscal spending could be even more dramatic as the composition of that spending changes. More money is earmarked to directly fund capital expenditures (capex), which has tended to operate with a multiplier effect on economic activity as it has a downstream impact on jobs, services and productivity growth.

Anmol Sinha,

Source: US Bureau of Economic Analysis. Data as of August 31, 2023.

Federal surplus/deficit as a percentage of GDP (%, 12-month moving average)

Federal deficit widens in 2023

Navigating a “higher-for-longer” world

With economic growth boosted by large fiscal deficits, interest rates could remain at levels the market has not been accustomed to seeing over the past 15 years. The 10-year Treasury could trade near the upper level of a range between 3.5% and 5.5% for an extended period as the Fed seeks to maintain growth consistent with inflation trending down to 2%. Ultimately, financial markets may prove more volatile over the next few years even if underlying growth dynamics remain more stable. “Higher interest rates for longer will eventually be successful and growth will ultimately fall, but it may take more time than the market currently expects,” Atluri says. “This may keep volatility elevated as portfolios may once again have to reposition for yet another changing macro environment.” While volatility should lead to dislocations and attractive opportunities, investors may need to be cautious with the amount of risk they take. Another scenario that could hurt the economy is the deficit falling quickly in the near term. “A large part of my thesis is that an 8% deficit is propping up growth and leading to higher-than-expected interest rates,” Atluri says. “But if the deficit should fall, this would have dramatic implications for the market.” Growth would likely decline, and the risk of recession would rise significantly. In that scenario, Atluri believes the Fed would need to cut rates significantly to recalibrate monetary policy for an economy with a significantly smaller deficit. Given the large size of today’s fiscal deficit and its importance to both monetary policy and economic growth, investors need to remain vigilant on how it may evolve in the coming years. The good news is that in a world where rates stay higher for longer, higher yields can offer attractive income and return potential, while also buffering potential price declines. What’s more, the price appreciation potential is meaningful should rates fall due to a sharper-than-expected slowdown or other external shock.

5

0

-5

-10

-15

-20

1960

1970

1980

1990

2000

2010

Nearly half of the US high yield market is now rated BB, says Flavio Carpenzano

“The pandemic and subsequent collapse in oil prices led to an influx of fallen angels while many of the weakest issuers defaulted”

“High yield can help to diversify income within a multi-sector income strategy”

Originally a home for “fallen angels” − companies that have lost their investment grade rating − the modern high yield bond market took off in the 1980s as a funding vehicle for companies undertaking merger and acquisitions (M&A) and leveraged buyouts (LBO). Today, it is a $1.793bn mature marketplace for companies to achieve their capital financing needs. Nonetheless, the more colourful origins of the sector can sometimes still negatively distort investor’s perceptions of the asset class. As the high yield bond market has matured, the overall quality of the investible universe has seen an evolution. Nearly half of the US high yield market is now rated BB − the highest end of the quality spectrum. At the same time, the weighting for bonds rated CCC and below has fallen from 22% in 2008 to a little over 12% today. This is demonstrated in the following chart, which shows the composition of the Bloomberg US Corporate High Yield Bond Index over the past decade.

Investment takeaways

As we approach the end of the current hiking cycle, yields across high yield are once again high. The high level of yields now available, and the relatively low correlation to more interest rate sensitive areas of the bond market, mean that high yield can help to diversify income within a multi-sector income strategy. Starting yields of around 9% also mean that high yield can now deliver high single to low digit returns over the long term. The rise in credit quality of the overall high yield market means there is now a much wider pool of high-quality names in which to invest. Thanks to the rise in yields, attractive returns can now be sourced in such bonds, reducing the overall level of portfolio risk potentially required to achieve the return objective. The rise in yields also means there is sufficient carry to offset any likely volatility. The increase in quality of the high yield market makes clear our point that not all high yield bonds are created equal. Appreciating this development gives investors the chance to exploit a broad range of investment opportunities that can potentially help them to achieve a durable source of income.

Source: Bloomberg. Exposures are calculated using the index amount outstanding of the ratings sub- indices, being Bloomberg Ba US High Yield Index for the BB-rated weighting and the Bloomberg Caa US High Yield Index for the CCC-rated weighting.

The BB rated component of the high yield market has increased, as CCC has fallen

Five factors have contributed to the improvement in the credit quality of the high yield market. 1. Changing funding models for LBO and M&A Riskier M&A and LBO funding have moved away from the high yield market into the leveraged loan market. This shift reflects the changing macro-economic and regulatory environment post the global financial crisis (GFC). These changes have led LBO and M&A sponsors to pivot toward the potentially lower transaction costs and time frames available in the loan markets. 2. The pandemic caused more angels to fall The amount of BB-rated bonds in high yield indices accelerated in 2020, climbing to a record high of more than 50%. The sharp increase was because of a surge in fallen angels impacted by the pandemic. Data from Barclays shows over $200bn of bonds were downgraded to high yield, entering a market which at that time was around $1.3 trillion in size. The sectors most directly affected by the shuttering of economies saw the largest falls. This included automotive, oil and gas and transportation companies. Fallen angels tend to be larger multinational companies compared to the typically smaller high yield company. Shorn of their access to the relatively low funding rates in investment grade, fallen angels have a strong incentive to repair their balance sheets and return to investment grade. This can present significant investment opportunities, as fallen angels often outperform new issue high yield bonds. We saw this in 2022 with the large increase in rising stars.

3. Energy down Alongside the improvement in credit quality, the sectoral composition of the high yield market has also evolved. The weighting of the energy sector, which has historically been the largest and most volatile component of high yield indices, has fallen from approximately 15% in 2018 to around 12% in 2023. Importantly, just as occurred in the wider high yield index, the pandemic and subsequent collapse in oil prices led to an influx of fallen angels while many of the weakest issuers defaulted. There was also an increase in M&A activity within the energy sector. Many of these transactions involved investment grade companies buying high yield issuers. The combined entity was often awarded an IG rating by the credit rating agencies. 4. Survival of the fittest − the weakest leave the index The pandemic caused a surge in defaults, which removed the weaker credits from indices. This included some energy companies and some retailers such as the US-based JC Penney. Just as fallen angels can return to investment grade, so too can defaulted companies return to high yield following a restructuring of their debt. This will typically mean the credit quality of the issuer has improved, although not always. 5. Manageable maturity walls Allied to the strength of underlying credits is the tenure of debt outstanding. High yield companies have been prudent over the past decade and have taken advantage of the period of low interest rates to term out their debt. As a result, the maturity profile of the market over the next few years remains manageable.

1. As of 30 September 2023. Market value of the Bloomberg Global High Yield Corporate index

From the power of bond coupons to knowing when to surrender, in this article four Capital Group stalwarts reflect on key learnings in their careers

“Xxxxxxx xxxxxxxx xxxxxxxx xxxxxx xxxxxxxxx xxxxxx xxxxxx xxxxxxxxxxxx”

“Xxxxxxxxxxx xxxxxxxxxxxx xxxxxxxx xxxxxxxxxxxx xxxxxxxx xxxxxxxxx xxxxxxxx xxxxxxxxx xxxxxxxxx xxxxxxxx xxxxxxxxx xxxxxxx”

Imagine an economy plagued by persistent inflation and a Federal Reserve determined to fight it with aggressive, equally persistent interest rate hikes. While this might sound similar to what investors have experienced in recent times, it also describes 1973. That year, which marked one of the most turbulent economic environments since the Great Depression, Capital Group began actively managing fixed income portfolios. Over the past 50 years, our portfolio managers have navigated a multitude of market ups and downs, booms and bubbles, crashes and crises We asked four of our most tenured fixed income portfolio managers — two retired and two current — to provide insights and lessons learned over their long careers.

Source: Bloomberg Index Services Ltd. As of 30/12/22. Past results are not predictive of results in future periods.

Historically, income has dominated long-term total return

1. Don’t forget the simple power of bond coupons

Kirstie Spence, fixed income portfolio manager I joined Capital Group through our undergraduate programme. At the time, a seasoned portfolio manager told me, “Your most important job in fixed income is not to lose money.” From there, it became clear that, in many ways, the concept of fixed income is simpler than people think. One of the things that gets forgotten with bonds is simply the power of a coupon. In most bond structures, you earn an interest rate that is paid out over a specified period. That payment is very important in contributing to the total return you’re going to make on the investments. And certainly, in emerging markets debt, the capital appreciation or the value of the bond can move a lot over its life. Some things at the macro level are out of your control, but that coupon is a powerful cushion in terms of protecting that investment. And in the emerging markets bond sector where I specialise, it has always been the heart of the annual return and is often underestimated. People forget about that a bit when the headlines focus on interest rate changes, and they start worrying about technical terms like duration. But the coupon is a very powerful thing.

2. Know when to surrender

Mark Brett, retired fixed income portfolio manager I remember early in my career before coming to Capital Group I came up with what I thought was a brilliant currency trade. Let’s just say, it wasn’t going well. So I approached my supervisor at the time. He asked me, “Do you know the first rule of trading? Surrender.” As humans, we often cling to bad ideas that we know should be dismissed. Part of being a good investor is knowing when to surrender a bad idea and move on. One example of a bad idea is continuing to fuel an asset bubble. And that leads to another important lesson: Don’t ignore the obvious. Consider the tech bubble in the late 90s. A lot of investors looking at it thought it was a bubble, but they didn’t know how it would turn out or think through the consequences. The same is true of the 2007 housing bubble. It was obvious that there was a bubble in residential real estate. But how would it end? That one turned out to be a huge deal, as we all now know, due to the implications for money and credit. Pointing out the obvious and surrendering a bad idea might seem like basic concepts, but you would be amazed at how tricky they can be for some investors.

Sources: Capital Group, ICE Benchmark Administration Ltd, London Bullion Market Association (LBMA), NASDAQ, Nikkei, NYSE Arca, NYSE, Refinitiv Datastream, Standard & Poor’s, Stock Exchange of Thailand (SET). Figures reflect cumulative price changes over 8-year periods in which the asset’s price increased at least 250% before falling at least 50 percentage points. Benchmarks used: gold bullion price per troy ounce as quoted by the LBMA (gold); Nikkei 225 Index (Japan); Bangkok SET Index (Thailand); NASDAQ Composite Index (US tech); S&P Homebuilders Select Industry Index (US housing); NYSE Arca Biotech Index (biotech); NYSE FANG+ Index (US large cap internet). As of 31 December, 2022.

Some notable asset bubbles over the last 40 years

3. Company relationships are key in credit markets

David Daigle, fixed income portfolio manager In active management, cultivating strong connections with the C-suite of the companies we invest in is essential. And I’ve always felt that if I can build a mutually symbiotic relationship with a management team, I’m providing value to them and they’re providing value to me Our relationship can benefit a company’s management team by sharing our insights with them about how we think as investors. Our discussions help them to understand what the investment community is looking for and sometimes what the rating agencies are looking for. What we get as investors is a better understanding of their strategy and whether they are good candidates for our portfolios. They can share how they see their competitive positioning and what they think of their competitors. They may explain how they think about the regulatory structure in which they operate, or what their aspirations are over different time horizons.

4. Collaborative research is crucial

John Smet, retired fixed income portfolio manager I’m struck by what I’ve experienced since retiring. Now I am a fund shareholder instead of a fund manager. The contrast is remarkable when I try to assess investment opportunities on my own. Just think about where we are today with markets and fixed income. There are questions in many investors’ minds: Has the Fed stopped raising rates? Is inflation here to stay? What about a recession? Is the dollar going to strengthen? These questions are difficult to answer for professional investors with vast resources. But they’re near impossible to answer as a shareholder in my kitchen, reading the newspaper or listening to the news trying to figure all this out. By contrast, at Capital Group, I had hundreds of analysts that I was able to interact with, along with other colleagues and outside specialists. It was really a stunning amount of information. The thing that strikes me is how blessed I was to have all those resources as a fund manager and the value of collaboration.

John Smet in the trading room, 1986

1990-1999

2000-2009

2010-2019

7.7

6.6

3.8

Coupon return

Price return

Total return components of the Bloomberg U.S. Aggregate Index (%)

Gold

Japan

Thailand

U.S. tech

U.S. housing

Biotech

U.S. large-cap internet

Cumulative return of select asset bubbles (%)

Valuations are not compelling at index spread levels, but there are opportunities to be found

Global corporate bond spread movements were muted over Q3. Broader risk sentiment was negatively affected by slower-than-expected growth, doubts about China’s recovery and central banks’ monetary policy. However, this was countered by relatively sound corporate fundamentals and demand for the asset class. The credit spread on the Bloomberg Global Aggregate Corporate Index narrowed to 127 basis points (bps) before widening in the second half of the quarter, ending the quarter at around 135 bps, around five bps tighter than end of June levels. European credit spreads tightened overall during the quarter, whereas US credit spreads widened marginally.

Data as at 29 September 2023. Percentiles from August 2000 for US/Europe and August 2001 for Global. IG: investment grade. Indices: Bloomberg Euro Aggregate Corporate Index, Bloomberg US Corporate Investment Grade Index, Bloomberg Global Aggregate Corporate Index. Source: Bloomberg

Global, US and European corporate bond spreads have widened from the 2021 lows

Market participants started to realise that interest rates are likely to stay higher for longer, causing financial conditions to tighten with the US yield curve steepening as yield rose. In this environment, total returns were negative, with the Bloomberg Global Aggregate Corporate Index returning -2.73% in US dollar terms on an unhedged basis, although both US and European corporate bonds generated marginally positive excess returns. Financials bonds outpaced bonds issued by industrials and utilities companies, with banks expected to benefit from a longer-than-expected high interest-rate environment. Looking ahead, the environment and outlook for corporate credit spreads is mixed, with central bank tightening, the ongoing uncertainty around growth and recession and expected softer corporate fundamentals weighing on the market. Valuations are not compelling looking at index spread levels, but there are pockets of opportunities: spreads on European corporate bonds are wider than US corporate bonds and valuations for financials bonds are more attractive than industrials. The “all-in” yield on global corporate bonds also looks attractive after the recent sell-off in government bond markets and the steepening in yield curves. The demand for the sector, which has kept spreads relatively compressed since the wides earlier in the year, should also continue to be supportive going forward. Given the uncertainties, our focus is on finding idiosyncratic opportunities at the company and sector level, in areas such as in banking, utilities and chemicals.

Europe and the UK represent the most attractive relative value

The third quarter was painful for global rates markets, with global government bonds returning around -4.2% . Curves steepened as the ‘higher for longer’ narrative began to take hold and US and European longer-dated yields moved higher. While the UK curve also steepened, this was driven more by falling front-end yields as expectations of further rate rises faded. Market expectations are for the current level of rates to be maintained into 2024 with a pivot to looser monetary policy pushed into the second half of the year.

Data as at 30 September 2023. Chart shows 2s10s curves for major markets. Source: Bloomberg

Curve inversion reduced in Q3, led mainly by more elevated longer yields

The divergence in global growth and inflationary conditions has become more pronounced. While we believe developed market central banks to be at, or very close to, the end of their hiking cycles, the US economy’s resilience stands out. In contrast, a weaker growth outlook, compounded by increased interest-rate sensitivity and greater exposure to the slowdown in China, means the transition to a less restrictive policy environment is likely to come sooner in Europe. We see this as an attractive entry point for global rates exposure, given the uncertainty around the global macroeconomic outlook alongside higher yield levels. Should inflation continue to trend down, the need to maintain elevated rates will decline and it is likely that central banks will ease to avoid passively tightening real rates. In our view, Europe and the UK represent the most attractive relative value, with curve steepener positions potentially benefiting as front-end yields adjust and term premium potentially increases. In contrast, we are underweight Japan rates as an exit or relaxation of yield curve control may be painful for Japanese duration. We find it challenging to reach a consensus view on currencies. Real rate differentials and a potential flight to safety are positive for the US dollar. However, this is offset by current high valuations and a potential Federal Reserve dovish pivot which could soften relative carry and undermine dollar strength.

Data as at 30 September 2023. Chart shows foreign exchange returns for major currencies vs USD, and DXY. DXY (=US Dollar Index), GBP (=British pound sterling), CHF (=Swiss Franc), JPY (=Japanese yen), CAD (=Canadian dollar), EUR (=Euro), CNY (=Chinese yuan). Bps: basis points. Source: Bloomberg

US dollar richness returned in Q3 as it regained strength versus most major currencies

1. As at 29 September 2023. Index: Bloomberg Global Aggregate Treasuries Total Return Index Value Unhedged USD. Source: Bloomberg

In this wide-ranging discussion on the prospects for fixed income, we hear viewpoints from the asset management, adviser and pensions fields

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. The information provided is not intended to be comprehensive or to provide advice.

December 2023

The conversation has shifted to how long rates will stay at this level, according to Ed Harrold

You can view the full webinar here

The fall in inflation will be volatile rather than serene but we’re heading in the right direction, according to Ed Harrold

Investment grade corporate bonds are offering attractive yields and potential protection in the event of a severe downturn, according to Ed Harrold

Now is the right time to incrementally increase bond duration, according to Ed Harrold

A pivot ought to be beneficial though uncertainty remains, says Robert Burgess

Portfolio Manager, Capital Group

Robert Burgess,

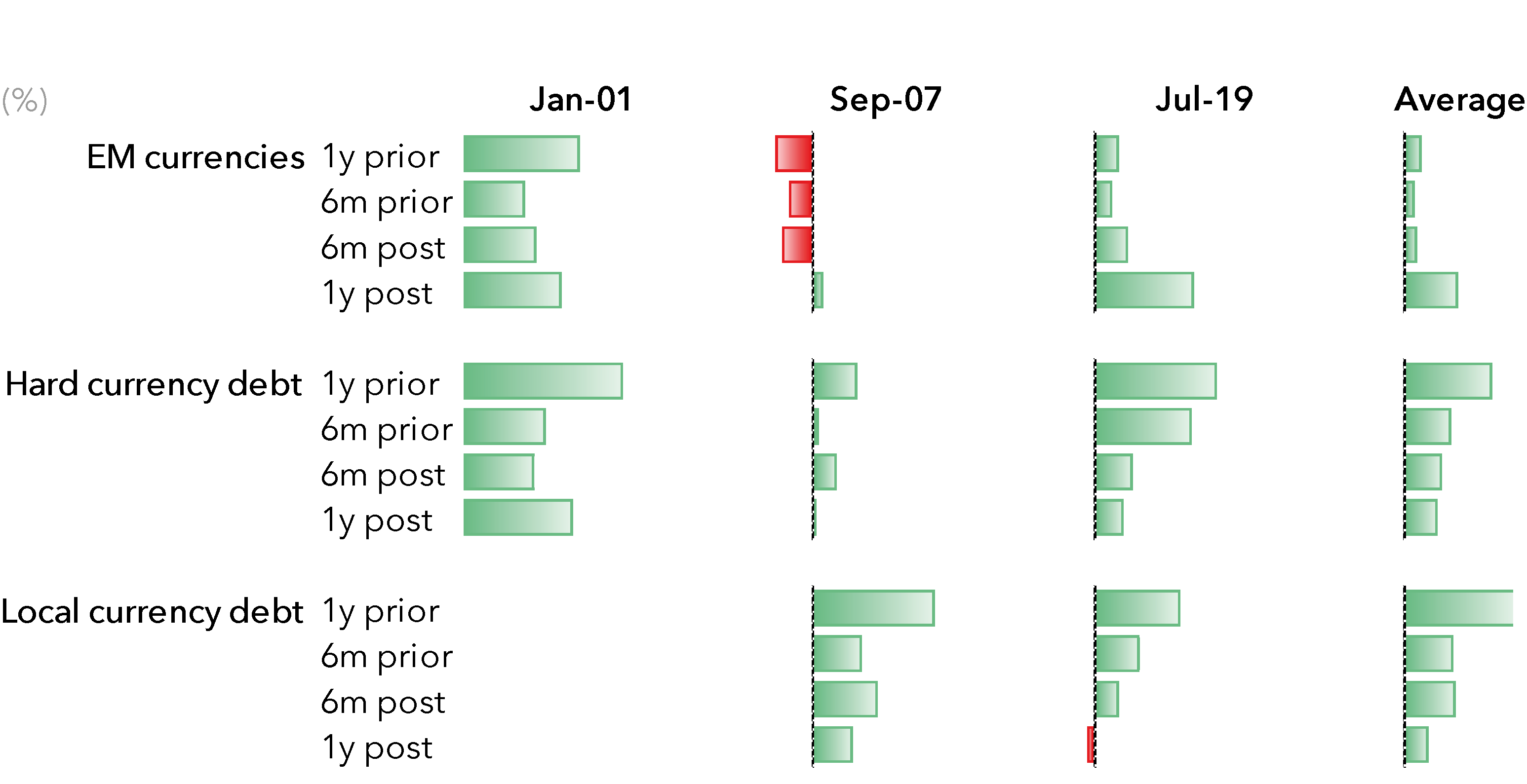

The US Federal Reserve (Fed) made a surprise dovish shift from previous policy on 13 December. The Federal Open Market Committee (FOMC)’s statement signalled the end of the hiking cycle and opened the door to a discussion on rate cuts. In the post-meeting press conference, Fed Chair Powell said: “We believe that our policy rate is at or near its peak for this tightening cycle.” Meanwhile, the median dot for next year is now 50 basis points lower than the September projection, with Fed Funds futures now pricing a full cut by the March 2024 meeting. If supported by incoming inflation data, a more dovish Fed will clearly be positive for EM debt, although it is important to note that US rates are still likely to remain significantly higher than the near-zero levels of 2021. Furthermore, if inflation were to re-accelerate or prove to be stickier than expected, we are likely to revert back to the higher-for-longer US rate environment. The table below shows how EM currencies, hard currency and local currency debt have performed 1 year and 6 months prior to and 6 months and 1 year post Fed rate cuts in previous Fed cutting cycles. Both local and hard currency bonds have rallied the most in the run up to rate cuts, while EM currencies have performed better after the rate cuts have taken place.

January 2024

Hard currency debt represented by JP Morgan Emerging Market Bond Index Global Diversified (EMBI). Local currency debt represented by JPMorgan Global Bond Index Emerging Markets Global Diversified (GBI-EM GD). EM currencies represented by EM currencies weighted by GBI-EM GD versus the US dollar. Exact dates are as follows: 03/01/2001, 18/09/2007 and 31/07/2019. Returns in USD. Sources: Bloomberg, JPMorgan.

How EM has performed in previous Fed rate cutting cycles

Support for the dollar should start to fade

While EM currencies recovered somewhat in 2023, the strength of the US dollar and weak EM currencies have broadly been a drag on local currency bond returns over the past decade, despite the fact that the dollar looks overvalued on most fundamental metrics. This could change with lower US rates, although the process of unwinding dollar strength is likely to be a slow and gradual one given that the real rate level is still supportive of the dollar over other developed currencies and growth outside the US remains relatively weak.

The US may escape recession, but global growth is set to remain weak

While the US has so far managed to avoid a traditional recession, different sectors have been experiencing downturns at different times. The US looks set to slow further from its current pace given both the lag from a tightening in financial conditions and a lower fiscal impulse in 2024. We already see evidence of slowing labour market activity and a normalisation in some measures of consumer credit performance. The path for EM has historically been highly correlated with US growth, as shown in the following chart, and taken very different paths depending on whether the US manages to have a soft landing or not. The fact that the US experienced the less-severe “rolling recession” in 2023, suggests that it may avoid a traditional recession in 2024 as well.

As at 30 November 2023. Sources: JPMorgan, Bloomberg. Left vertical axis: Emerging Market Bond Index (EMBI) spreads (bps). Right vertical axis: Fed Funds rate (%). Shaded periods are National Bureau of Economic Research (NBER) US recessions.

EMBI spreads during US rate cycles and recessions

Outside of the US, growth is expected to remain relatively weak. Compared to the US, Europe was hit more heavily by the energy shock and the region has seen and still faces some of the most difficult policy challenges with the trade-off between inflation and growth. The latest business surveys show a stabilisation in eurozone economic activity at weak levels, and there remains a significant risk of contraction in some economies. In China, the latest PMIs (Purchasing Managers’ Index) were consistent with an economy continuing to expand at a very slow rate. The government has shown some willingness to use both fiscal and monetary policy to support growth, and while there might be a cyclical pick-up in growth in response to these measures, China is likely to have to adjust to a deceleration in its longer-term trend in growth over the next several years. Elsewhere in EM, we can expect an acceleration of growth in EM Asia (outside of China), a deceleration in Latin America and broadly stable growth in Europe, Middle East and Africa (EMEA).

The US could avoid recession, supporting fixed income yields to remain high

“I’m optimistic that consumers will continue to carry the economy, even as rates remain higher for an extended period”

Economist

Jared Franz,

Why didn’t the US fall into recession in 2023, as so many pundits predicted? The recession did happen, just not all at once. Over the past year and a half, different economic sectors experienced downturns at different times —a phenomenon economists call a “rolling recession.” Thanks to this rare event, it’s possible the US won’t experience a traditional recession before the end of this year or even the next, despite the burden of high inflation and rising interest rates. For example, US residential housing contracted sharply after the Federal Reserve started aggressively raising interest rates. At one point in 2022, existing home sales tumbled nearly 40%. Now there are signs that the housing market is recovering. The chart illustrates several sector-based examples. If these contractions and recoveries continue, the US could avoid the most widely predicted recession in history, says Capital Group economist Jared Franz. Citing a strong labour market and resilient consumer spending, Franz believes the US economy could grow at an annualised rate of roughly 2% in 2024. “This has been Godot’s recession —we’ve all been waiting for it,” adds portfolio manager Chris Buchbinder. “But in my view, the probability of a severe downturn is now well below 50%.”

Higher rates for an extended period