Is cashflow-driven investing bettering the journey to endgame?

Summary

Liz Truss and Kwasi Kwarteng’s mini-budget in 2022 caused disruption in bond markets and plunged DB schemes into a sudden liquidity crisis.

The spike in gilt yields pushed some DB schemes into a liquidity corner, forcing them to sell assets to meet collateral calls on their hedges.

Our survey of DB pension scheme trustees explored how pension schemes absorbed vulnerabilities in their strategies, and if cashflows are better managed one year on.

The results showed the crisis prompted schemes to scrutinise investments and associated risks, with some schemes now taking a more hands on approach to investing.

The rise of strategies such as cashflow driven investing to manage liabilities reflects trustees’ efforts to manage risks and plan for endgame.

There is also a renewed effort to ensure liability risks are balanced for an era of ‘Black Swan’ style events, leading trustees to explore cash flow matching and other customised solutions.

Methodology

This report is based on the results of research conducted by Professional Pensions and Incisive Works into schemes’ attitudes around cashflow driven investing.

The research, which took place between November 2022 and April 2023, comprised a series of in depth qualitative interviews with several professional trustees, followed by a survey of 136 trustees of UK pension schemes.

A Black Swan on the Pensions Path

Brexit; Covid-19; the cost-of-living crisis - there is no doubt pension schemes operating today are investing in a time of elevated market volatility.

And one year on from another crisis centered on gilt movements, most trustees in the industry believe market disruption and macroeconomic instability will continue. This is a view held by all those operating a defined benefit (DB) scheme, with those not fully funded holding the strongest stance.

83

70

of respondents believe rolling economic crises are likely to be the ‘new normal’

66

of respondents say market volatility has become a bigger concern for their scheme over the past year

%

%

%

The crisis last year was predominantly focused on liquidity. It was a prompt to reassess how schemes are managing their cashflows. After all, schemes have been dealing with steadily declining gilt yields for over a decade. The impact of the Covid-19 pandemic in 2020 further compounded the decline to record lows. Over a ten-year period, this inflated the present value of DB scheme liabilities and caused scheme deficits to rise.

But last year this reversed very quickly, and as the value of UK government gilts fell, yields increased and schemes were forced to look at their liabilities in closer detail. In our survey, many trustees admit that they were prompted to take a closer look at what their schemes were invested in.

of respondents were prompted by the crisis to analyse their liability-driven investment (LDI) arrangements, trustees included

84

%

were prompted by the crisis to better understand their scheme's liquidity

79

%

say that the crisis prompted trustees to improve their understanding of what their scheme is invested in

66

%

The issue of cashflow is firmly on the table: over half (56%) of respondents state it has become a more important topic for their scheme over the past 12 months.

In particular, the journey to endgame, and ensuring schemes hold sufficient assets to meet future obligations to beneficiaries is the biggest concern and this has risen. For example, more than 50% of schemes that are less than fully funded are looking to cashflow-driven investment strategies specifically over the next five years. This becomes an even bigger focus as schemes are increasingly paying out significant cashflow to pensioners from scheme assets which may have fallen materially in size.

Concerns about cashflows

The decline of DB pension schemes and the increasing age profile of members means more consideration must be given to cashflows now

We need to consider cashflow-driven investments as the scheme is reaching a tipping point where the number of pensioners is outstripping non-pensioner members

With LDI taking up so much of the portfolio, given lower leverage and high liquidity buffers, we need to make sure the rest of the portfolio is either sufficiently liquid for cash withdrawals or provides us with ‘automatic’ cashflow when we need it

Cashflow-driven investing is an approach to investing which focusses on generating cashflows to meet objectives, rather than the traditional approach of just managing return and risk. And it is an effort to manage risks and plan for endgame, typically alongside liability driven investing (LDI). It has also proven useful for pension schemes battling ‘Black Swan’ style market events in recent years.

of respondents expect continued market turbulence for the next few years

Cashflow

after a Crisis

CDI Upsides

Generate cashflows

Better Certainty of Returns

Reduce funding level volatility

CDI is a broad term which in our view describes an investment strategy which focuses on generating predictable cashflows to help meet future liabilities. This covers a broad opportunity set typically investing in high quality assets across public and private credit and real assets. It is important to invest in high quality assets, that offer sufficient liquidity and a level of certainty on required cashflows to reduce reliance on selling assets in unknown future market conditions. Most assets are ‘safer’ in nature with lower default rates, lower overall portfolio volatility, and therefore offer improved certainty of meeting member benefits (the ultimate goal of a scheme) in comparison to pairing a traditional growth portfolio with LDI.

Many schemes approach CDI investing alongside a LDI strategy to ensure that all liability risks are hedged while generating cashflow to pay benefits. As is the case with any investment process, a successful CDI strategy is dependent on a scheme’s variables alongside portfolio diversification / portfolio allocations that are flexible and able to respond to unknown events including outflows.

“

How Are Trustees Approaching CDI in 2023?

Currently, 28% of schemes surveyed have adopted CDI. A further 18% are intending to following last year’s gilt crisis – and this figure rises to 27% for schemes that are not fully funded.

“

Our present investments have done very well over the past year, but we want a balanced investment strategy, and therefore CDI could be suitable for us

Although buyout is our preferred path to endgame, it is by no means certain we will be able to achieve it, even though we are fully de-risked. Therefore, CDI would be somewhat suitable for us as an investment strategy

Our scheme is very mature and liquidity is an issue. If we do not plan a buyout in the short-term a switch to some form of CDI would be suitable for us

We are aware there are changes in our investment strategy and part of that is hedging on cashflows; so there is some relevance to using CDI. However, we have not yet given it consideration at this stage

For some in our survey, however, there is optimism that a focus on growth investments is enough to keep cashflows in check.

“

We have a range of investments in place to generate cash and growth, but we are not driven by cashflow investment. We have faith in our investment consultants

The scheme is invested in a [diversified fund] which is heavily invested in the stock market. It is easy to sell units in this fund to generate cash so there is no need for CDI now or in the future

This could be a concern for schemes for several reasons.

Firstly, many schemes have been investing for growth in illiquid assets, which as we saw in last year’s gilt crisis has increased schemes’ vulnerability to market downturns and forced them to become asset sellers if they turn cashflow negative.

Every pension scheme should be reviewing the strategy as part of their journey plan, and particularly because of last year’s risk markets that placed schemes under pressure. Nearly every trustee will realise there are elements of CDI that have relevance to their scheme.

“

Alan Pickering,

Secondly, given the current rising interest rates, the impact on levered growth portfolios could also increase the need for liquidity if there is a higher requirement for collateral.

According to one accredited trustee interviewed for the survey, there are several reasons why CDI should be considered by schemes.

Another reason to consider CDI is because it promotes greater transparency and matching of a scheme's liquidity requirements. Often trustees are overloaded by 'spurious accuracy', which means they follow cashflow modelling projections too closely.

This can place schemes at risk, particularly as they may not have a cash buffer to cushion them against market events or ensure they have the cash to meet benefits payments alongside other unexpected outflows such as transfer values.

As more schemes become cashflow negative, then CDI becomes more and more important…to help with cashflow management [or to] help the strain on the sponsor for deficit repaid contributions. The other thing CDI does is it stops you being a forced seller, and invariably you will potentially build up a little bit of a buffer of cash to help at a later stage.

President, BESTrustees

“

George Emmerson

Professional Trustee, Capital Cranfield

Schemes in our survey are overwhelmingly being led by investment consultants (71%), however as last year’s crisis showed, the effort required to manage collateral and balance liabilities means faster and more innovative solutions are required. As a result, schemes surveyed that are using CDI are turning to fiduciary managers with close to half of respondents using this service.

Fiduciary management can cover everything from investment oversight and implementation to strategic asset allocation and can increase the flexibility and adaptability of schemes. In turn, it offers the trustee board time to focus on issues such as risk management and to strengthen internal operational processes or technical infrastructures – something they need the time to comprehend carefully in today’s markets.

The crisis showed how significant being nimble, from both the trustee and advisers side, in making decisions, understanding the problems and exploring a range of solutions is during an extreme event such as those experienced last year by UK DB pension schemes. For example, entering new types of assets such as private debt, means it is crucial to be closely tied with your asset manager. Those investments are notoriously difficult to receive updates on

“

Payam Kazemian

Professional Trustee,

Zedra Governance Limited

CDI on the Path to Endgames

On the one hand, CDI is well-suited for well-funded pension schemes, as there is naturally less reliance on generating higher returns. That is not to say CDI is not appropriate for schemes with lower-funding levels – and there are many different ways a CDI strategy can be implemented. In recent years, the availability of pooled pension vehicles has made CDI much more accessible for smaller schemes too.

55% of DB schemes in our survey say they are targeting a buyout vs 39% intending to run on. Those targeting a buyout tend to be the better-funded schemes.

Due to improved scheme funding levels and buyout feasibility - the UK’s 5,000-plus corporate DB pension schemes are now estimated to have sufficient assets to ‘buy out’ their pension promises with insurance companies - a tidal wave of demand is expected over the coming years. Accordingly, most schemes in our survey believe their buyout will happen in the next 5 years.

40

of schemes aiming for a buy-out think they will be bought out within the next 3 years

%

%

of schemes aiming for a buy-out think they’ll be bought out in the next 5 years

67

In fact, some trustees note that one reason they are considering cashflow-driven investing ahead of a buyout is because the insurance market has a finite capacity each year, and the recent surge in demand could see pension schemes jostling for a spot in the priority queue. In fact, there could be over £1trn of assets chasing perhaps £50bn of annual capacity in the insurance market .

If demand outstrips supply, schemes may find themselves standing in the buyout ‘queue’ for longer than they anticipate; and members’ liabilities will need to be paid for longer than originally anticipated. In this scenario, schemes may also be more exposed to future market turbulence.

In 2022 total bulk transfers amounted to just

£28bn , so it is going to take a while for insurers to get through that. Most insurers are going to be focused on large schemes where they make the most profit or manage the best economies of scale.

Because schemes have had a funding boost in 2023, the queue for buyout is longer. These schemes need to think of a way of running their scheme on a self-sufficiency style basis until there is an opportunity for them to do that risk transfer

“

Sophia Harrison

Professional Trustee, Punter Southall

£28

bn

£28

bn

£28

bn

Should these schemes be considering CDI in the interim to manage cashflow and maintain improved funding levels?

The overall sentiment among schemes surveyed is that CDI works better in the context of self-sufficiency (28%) than when pursuing a buyout. There it provides a degree of future proofing that enables a much more comfortable journey for both the employer and trustee, in a way that few other strategies do. More than three-quarters of respondents did also admit it equally suited both, however.

For some, at the point of risk transfer the scheme needs to have access to liquid investments in flexible strategies. Even on the journey to buyout there is a need to understand cashflow requirements, review contribution levels in relation to risk transfer levels, and ensure managers can match outflows with investment income on a short or long-term horizon. CDI also helps in terms of governance, noted one survey participant, whilst another said “cash is required for both a buyout and on the path to self-sufficiency – one is [to meet] the need for liquidity for a buy-out and the other to pay for benefits, as a scheme matures.

CDI is designed to generate a series of cashflows that meet end payments – that is also the ultimate end game for schemes running on a self-sufficiency basis because they have a longer pathway ahead of them to end game.

“

Kevin Wesbroom

Professional Trustee, Capital Cranfield

Case Study: CDI Use Case in Self-Sufficiency

Self-sufficiency

Following a robust risk management program alongside returns from growth assets, the scheme was able to achieve a fully funded position in 2021

A long-term objective of buyout within a 10-year period (over a quicker buyout)

A reduction of risk immediately to lock-in strong funding position

Pivot investment strategy immediately to a cashflow-focused approach

Funding position

Endgame path

Scheme objective

Scheme size

c£400m

The solution

The Trustee partner, GSAM, proposed a portfolio with a bespoke CDI strategy with 3 elements blended

An LDI “completion” portfolio. While the CDI portfolio will match off some cashflows the interest rate and inflation exposure for remaining cashflows will still need to be hedged

A lower-risk growth portfolio with risk exposure diversified across a balance of risks, with a particular focus on incorporating tail-risk hedging strategies

Manage ESG risks and implement guidelines aligned to clients requirements

Use in-house metrics to manage ESG risks within the credit portfolio, key in ensuring maximising potential of receiving all cashflows

• Further security / buffer against demographic changes

• Target of settlement into the future

• Manage risks to minimise reliance on sponsor

• Keep a high level of liquidity

Target return with a blend of income, growth and LDI

Retain high hedge ratio while maintaining a high collateral headroom buffer

Growth portfolio to include awareness of downside risks and explicit tail risk management and thoughtful use of alternative

Retain flexibility

The portfolio is buy-out aware with an implicit hedge to insurance pricing, while retaining liquidity and flexibility for any potential changes in strategic objectives (or to take advantage of market opportunities)

All sterling implemented at outset, but the CDI allocation has flexibility to invest in a broad global opportunity set should conditions change

Residual illiquid exposure in run-off

Pay benefits recognising slowing company contributions and increase in annual outgoings

Invests in a solution which matches the majority of the first 10 years of annual benefit payments, minimising sales needed for cashflows in adverse outcomes

Portfolio objectives/ Solution implications

Hover on a cell to view the solution implications

Invested over a 2-3 month period

Portfolio timeframe

alongside a growth portfolio allocation built with explicit downside risk management strategies to manage liability funding risks

As the scheme has adopted a self-sufficient CDI approach, the metrics and KPIs against which the mandate is reviewed have been broadened. In addition to our standard transparency in performance breakdown between SAA, manager alpha and dynamism, there is a need for cashflow-specific metrics including credit quality and migration, expected versus realised income and positioning relative to guidelines.

On an ongoing basis, we continue to support the trustee and advisors with regular updates and information. Over time, depending on the scheme’s objectives and market conditions the mandate has the flexibility to expand to cover a greater proportion of future benefit payments opportunistically.

Long-term asset monitoring

Sufficiency

A CDI portfolio of high-quality liquid credit optimised to match a significant proportion of liability cashflows over 10 years

Growth

CDI

LDI

issuer

Diversification to manage risks and costs across:

Diversification factors

sector

geography

Summary

1

A Black Swan on the Pensions Path

2

How Are Trustees Approaching CDI in 2023?

3

CDI on the Path to Endgames

4

Case Study:

CDI Use Case in Self-Sufficiency

5

Select a chapter

The rise of CDI

The Trustee View

The Trustee View

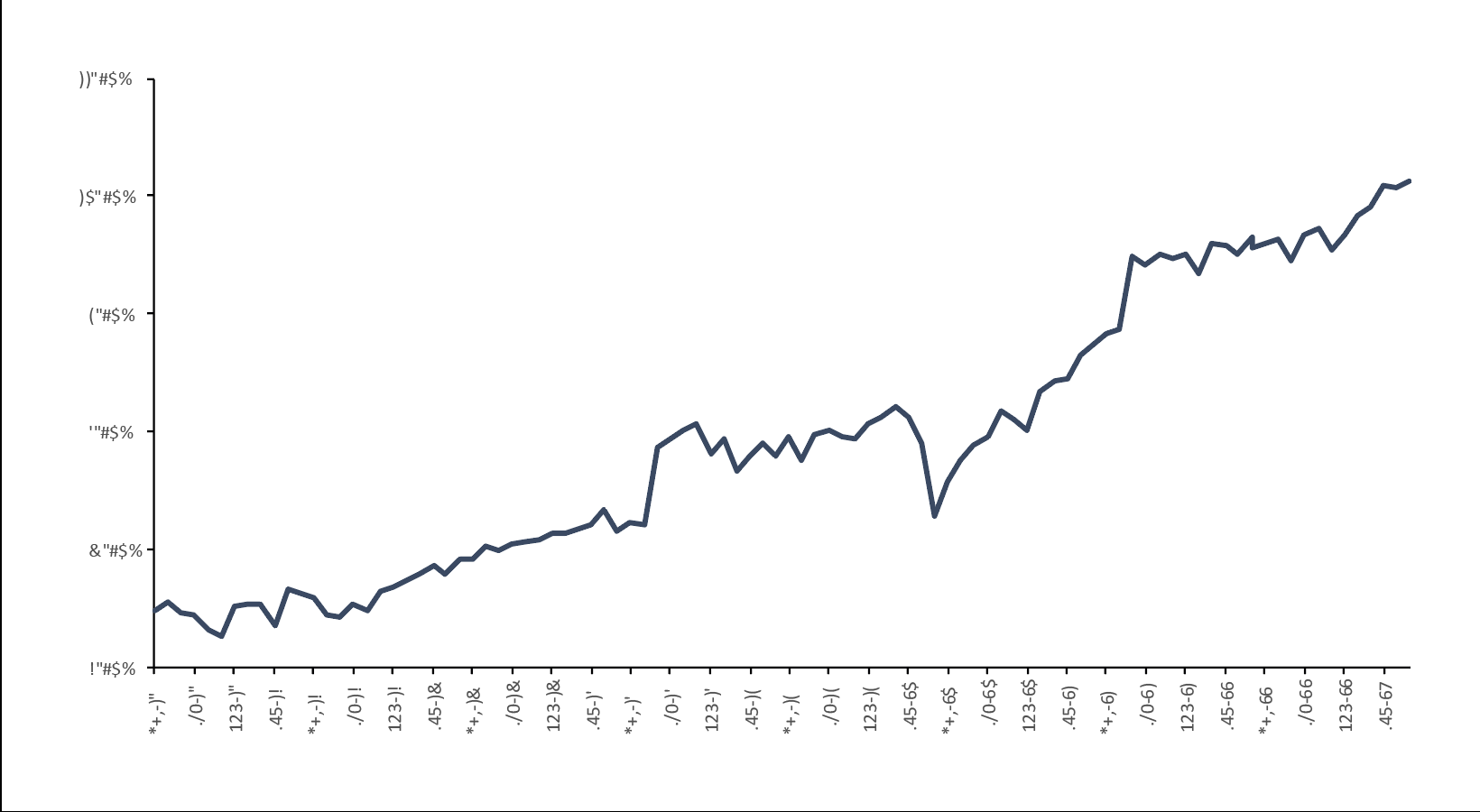

Self Sufficiency Funding Level

April 15

April 16

April 17

April 18

April 19

April 20

April 21

April 22

75%

85%

95%

105%

115%

65%

Hover for details

Protect and grow the funding level:

alongside a growth portfolio allocation built with explicit downside risk management strategies to manage liability funding risks

issuer

sector

geography

1

2

Sources:

1.

PwC; 'UK pension schemes reach record collective funding level'; October 2022

2.

Risk Transfer Report 2023; Hymans Robertson