august 2025

Key risks The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested. Important information Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass. This is not an advertisement for pension members or employees. It’s intended for professional financial advisers and pension trustees classified as Professional Clients and should not be relied upon by pension plan members, employees, or any other persons. Legal & General Assurance Society Limited. Registered in England and Wales No. 00166055. Registered office: One Coleman Street, London EC2R 5AA. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. About L&G Retirement America L&G Retirement America, as an active participant in the US Pension Risk Transfer market, receives and analyzes in the normal course of its business certain information provided to it and other market participants. All non-aggregated statistics presented herein are available in the public domain. The inputs for US aggregated statistics are widely available in the market but may be subject to individual confidentiality obligations. Although believed to be reliable, information obtained from third party sources has not been independently verified and its accuracy or completeness cannot be guaranteed. Legal & General Retirement America is a business unit of Legal & General America, Urbana, MD. Legal & General America life insurance and retirement products are underwritten and issued by Banner Life Insurance Company, Urbana, MD and William Penn Life Insurance Company of New York, Valley Stream, NY. Banner products are distributed in 49 states, the District of Columbia and Puerto Rico. William Penn products are distributed exclusively in New York; Banner Life is not authorized as an insurer in and does not do business in New York. The Legal & General America companies are part of the worldwide Legal & General Group. CN08132025-1

scroll

UK view

US view

Rest of the world

Investment outlook

Key takeways

Global PRT Monitor

For professional investors only. Capital at risk.

Defined Benefit pensions – a global engine for growth The theme of growth has been a consistent thread throughout recent editions of the PRT Monitor, and it remains very much intact. Despite facing some headwinds from historically tight credit spreads and geopolitical uncertainty, insurers have reacted, evolving towards new, more diversified and dynamic investment strategies and continue to deliver attractive pricing and increased capacity to pension plans. With pension plan funding levels at historic highs, we estimate that approximately £1 trillion of pension liabilities could be insured across global markets in the next decade. Over this time horizon, we are projecting up to £0.5 trillion of activity in the UK, £0.4 trillion in the US and £0.1 trillion in Canada, with potential for more in other new markets. Insurers are thinking globally about this opportunity - both in terms of scaling their operations to meet growing demand from pension plans, and in supporting companies to de-risk their balance sheets, draw a line under their historical obligations and focus on their core businesses. This presents a significant opportunity to support both pension plan members and society at large. Insurers not only offer long-term financial security to millions of pension plan members, but also reinvest premiums into socially beneficial assets such as housing and infrastructure. While the market continues to grow and evolve in new and exciting ways, client and customer service remain at its heart. In our latest edition of the PRT Monitor, we analyse the global market dynamics and economic trends shaping today’s DB (Defined Benefit) pensions industry and examine the PRT (Pension Risk Transfer) landscape across the UK, US and rest of the world.

Sponsored by Natwest Insurer Rothesay

Infographic here

For more detail on investment strategies and endgame options please read our article below.

Read article here

Source IPE Research 2023.

Article 1 standfirst goes here

The last few years have been particularly notable not just for the increase in annual volumes, but the significant increase in the number of transactions completed each year.

UK PRT market sees record transaction numbers Total UK transaction volumes amounted to £47.8 billion in 2024 – the second-largest year ever – with a record 299 buy-in and buyout transactions completed. For the first time, six insurers each wrote volumes of more than £5 billion. This is a great example of the healthy competition that exists in the UK market and the variety of options currently available to pension plan trustees. Buy-in and buyout activity continues apace in 2025 with robust activity across all segments of the market. We announced in our half year results for 2025 that we have written or are in exclusive negotiations on £5.2 billion of global PRT in the year to date. Growth across the whole market The last few years have been particularly notable not just for the increase in annual volumes, but the significant increase in the number of transactions completed each year. Data from Hymans Robertson shows that transactions involving plans under £100 million made up almost 80% of all transactions in 2024. Insurers have innovated to deliver streamlined solutions for smaller plans, including L&G’s own Flow proposition, which supports plans on a collaborative journey all the way through to buyout. At the larger end of the market a record 14 buy-ins of over £1 billion were completed last year. Today this is seen as business as usual, but prior to 2015, the UK market had completed just seven transactions of over £1 billion in its entire history.

Subhead Lorem ipsum dolor sit amet, consectetur adipiscing elit. Donec pulvinar massa a justo lacinia, ut mattis lectus blandit. Aliquam gravida dictum justo.

£6,075m

c

b

Publicly announced transactions in 2025 Among the largest publicly announced transactions so far in 2025 are L&G’s £800 million buy-in with the Honda Group UK Pension Scheme and a £785 million buy-in with Anglo American. Other pension plans to have completed transactions so far this year include those sponsored by Rolls-Royce, National Grid, MMC UK, and Baker Hughes. Additionally, 2025 has seen further multi-billion-pound cases come to market, with most expected to transact in the second half of the year. New entrants and market developments Alongside growth in the market, an evolving panel of insurers writing PRT business is providing increased choice to trustees and sponsors. Utmost and Royal London wrote their first transactions last year and in recent developments, Athora and Brookfield have announced agreements to acquire Pension Insurance Corporation (PIC) and Just Group respectively. In addition L&G unveiled long-term strategic partnerships with Blackstone and Meiji Yasuda aimed at accelerating L&G’s growth ambitions in the PRT sector.

Source: hymans.co.uk/media/gm1om4m4/bulk-annuity-and-longevity-hedging-h2-2024.pdf 2025 estimate - based on L&G analysis

Increasing focus on member experience and customer service In the UK PRT market there is a growing emphasis on customer service and the support available to members before and during retirement. With a range of insurers in the market, pricing is competitive, and providers are looking for new ways to differentiate themselves. As a result, service quality - both before and after buyout is becoming an even more important facet of insurer propositions. Market growth and greater capacity are significant positives for pension plans but also present operational challenges. Pension plan administrators and insurers’ post-transaction teams alike face increasing workloads. Insurers will need to demonstrate their propositions are not merely focused on completing a buy-in transaction, but on working with trustees and administrators to guide the plan to buyout and then providing market leading service to policyholders. A recent Aon survey revealed that as the number of pension plans offering additional member options and support increases, so too does the appetite for insurers to keep these options and support in place post-transaction. The Pension Schemes Bill The UK Government has recently released the first draft of a new Pension Schemes Bill which will aim to make it easier for well-funded DB plans to release surplus, when ‘safe to do so’. These measures have the potential to provide sponsors and trustees with greater choice, for example through opportunities to enhance member benefits, provide for DC benefits and invest in the UK growth agenda. In June, L&G launched a pioneering solution that enables DB pension plans to transfer surplus funds into DC arrangments, including our award-winning Mastertrust. By facilitating surplus transfers, we help employers reduce ongoing contribution costs or enhance member outcomes in DC plans, without impacting existing DB liabilities. This solution also supports long-term retirement adequacy and reflects our commitment to joined-up thinking across pension strategies.

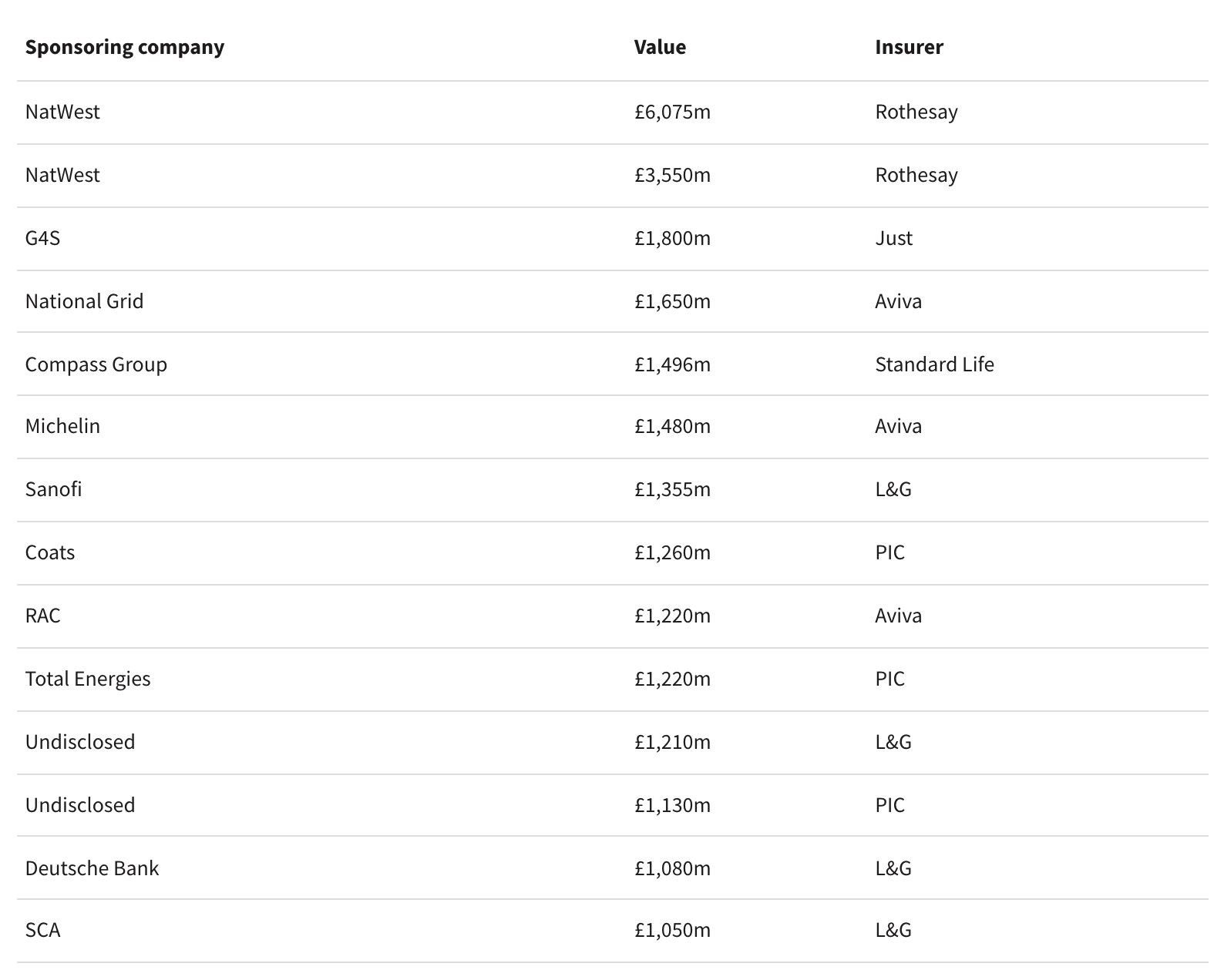

Buy-ins and buyouts above £1bn in 2024

Historical UK PRT Volumes (£bn)

A record 14 buy-ins and buyouts above £1bn in 2024

Source: Bulk annuity and longevity hedging – H2 2024 | Hymans Robertson

Sponsoring Company

Compass Group

£1,496m

G4S

£1,800m

Natwest

Rothesay

£3,559m

Coats

£1,260m

pic

Total Energies

£1,220m

Undisclosed

£1,130m

National Grid

£1,650m

Michelin

£1,480m

RAC

Sanofi

£1,355m

£1,210m

SCA

£1,050m

Deutsche Bank

£1,080m

l&g

aviva

rothesay

just

standard life

Buyout, run on or both The developments around surplus extraction have led to increased discussion as to whether some trustees may wish to run-on their plans for longer. Conversely, we expect some pension plans may accelerate their move to buyout so that they can crystallise their surplus. . Our view is that it doesn’t need to be a binary choice - a point highlighted in the latest episode of The PRT Pod where guests Rosie Twist, Origination and Execution Director at L&G and Laura Amin, Partner at LCP explore the range of endgame strategies available. The option remains open for plans to run-on for a period before completing a buy-in at an optimal point in the future. This can afford time to, for example, generate further surplus, run off illiquid assets or prepare for a buy-in transaction. Objectives will depend on individual circumstances and with deep expertise in both investment and insurance, L&G is uniquely positioned to guide plans through this evolving landscape. Using DB pensions to catalyse economic growth We support the Government’s UK growth agenda and believe that insurers are well-placed to deliver the vision of pensions as an engine for economic growth. Typically, insurers invest significant proportions of the buy-in premiums they receive into ‘direct investments', which include areas such as housing, infrastructure and renewable energy. Transferring pension plan assets to an insurer is therefore likely to unlock significantly more capital to be invested in productive investments than if the assets had remained on the pension plans’ balance sheets. This is supported by data from the Association of British Insurers which shows that UK annuity providers have already invested around £178 billion into productive investments, with nearly two thirds of their total investment being into the UK economy. With annual PRT market volumes of between £40 to £50 billion expected for the coming years, our analysis suggests that over the next decade the UK PRT industry will be able to invest over £100 billion in productive assets. Market outlook Based on our pipeline and the annual baseline of around £45 billion of DB pension liabilities transferred to insurers in the past couple of years, we expect that the market will achieve volumes within the range of £40-50 billion in 2025, with heightened demand persisting across the next decade. Data from The Pensions Regulator estimates that roughly half of all DB plans are fully funded or better on a buyout basis, bringing to life the scale of the market opportunity in the years ahead. For a comprehensive overview of L&G’s UK PRT business, we invite you to read our accompanying half-year market update. It highlights our new business performance in H1 2025, explores how synergies across our Group enable us to deliver bespoke solutions for clients, and shares updates from our Customer Service team - recently honoured as the UK Customer Service Team of the Year at the CCA Global Excellence Awards.

Objectives will depend on individual circumstances and with deep expertise in both investment and insurance, L&G is uniquely positioned to guide schemes through this evolving landscape.

US PRT Market Update The US market also saw its second-largest year for PRT on record in 2024 with transaction volumes totalling $51.8 billion, only slightly behind the all-time record of $51.9 billion set in 20221. Market volumes in the US continue to be driven by jumbo transactions over $1 billion. In 2024, seven such transactions closed for a combined total of approximately $22 billion, representing a significant portion of the annual market volume. In 2025, activity has remained high in terms of the overall number of PRT transactions coming to the US market. However, the number of jumbo transactions has been lower in H1 compared to last year, which has impacted overall premium volumes. The first quarter of the year totaled $7.1 billion2, a decrease of over 50% when compared to the first quarter of 2024’s total volume of $14.6 billion3. A similar story is expected for the first half market volume. We estimate the first half of the year to close at around $11 billion compared to $26 billion4 in 2024. One jumbo transaction closed in the first half of the year for around $1 billion, whereas five of the largest transactions in H1 2024 totaled around $15 billion. If you remove the jumbo transactions, the first half of 2024 and 2025 would both be around $10 billion, highlighting the impact that jumbo transactions have in any year on total market volume.

US View

Source: LIMRA Secure Retirement Institute Group Annuity Transfer Survey. 2025 figure based on Legal & General Retirement America’s estimation.

Market Outlook As is typical in the second half of the year, we expect US PRT activity to pick up through the rest of 2025, with a few more large transactions coming to market. These jumbo transactions will significantly impact the total premium volume, which we are currently estimating to be between $35 and $45 billion. In February, we announced the creation of a long-term strategic partnership with Meiji Yasuda, a market leading Japanese mutual life insurance company. This partnership will allow us to drive growth in the US PRT business, while Meiji Yasuda will expand its established partnership with L&G in asset management by outsourcing the investment management of US PRT and protection assets to L&G. In addition, we announced a long-term partnership with Blackstone in July. Through this partnership, we’ll gain access to a broader range of high-quality investments, predominantly in the US, using Blackstone’s private credit platform. We plan to invest up to 10% of our new annuity business through this collaboration. Together, we’ll also develop new investment products that combine public and private credit, helping us reach more global wealth and wholesale markets.

Historical US PRT Volumes ($bn)5

1. https://www.limra.com/en/newsroom/news-releases/2025/limra-u.s.-single-premium-pension-risk-transfer-sales-leap-14-to-$51.8-billion-in-2024 2. https://www.limra.com/en/newsroom/news-releases/2025/limra-first-quarter-u.s.-pension-risk-transfer-sales-top-$7-billion/ 3. https://www.limra.com/en/newsroom/news-releases/2024/limra-u.s.-pension-risk-transfer-sales-post-record-high-first-quarter/ 4. https://www.limra.com/en/newsroom/news-releases/2024/limra-u.s.-pension-risk-transfer-sales-jump-14-in-first-half-of-2024 5. https://www.limra.com/siteassets/newsroom/fact-tank/sales-data/2025/1q/u.s.-group-annuity-risk-transfer-activity--buy-out-sales-2025-first-quarter.pdf

Market developments With increased economic uncertainty, some companies have shifted their focus away from de-risking their DB plans to focus on their core businesses but should pick back up again as the markets steady. As illustrated by the chart of US PRT volumes below, we saw a similar dynamic in the global pandemic, where the total market volume dropped slightly in 2020 and then quickly regained its momentum to have the three largest years on record from 2022 to 2024. The long-term outlook remains very positive. Between 2022 and 2025 we witnessed an aggregate c.$60 billion of deal flow for the first half of the year, compared with c.$33 billion for the three-year period before this. One trend we are seeing in the US is a significant increase in the number of buy-in transactions coming to market. Though common in the UK, buy-ins are a newer trend in the US where traditionally, nearly all transactions have been buyouts with the plan sponsor transferring full responsibility of the plan to an insurer, including participant administration. We have seen a slow increase in buy-in transactions over the past few years, but we anticipate an over 50% increase this year compared to any prior year. The majority of these buy-ins are for full terminations, where the plan sponsor looks to lock in pricing early on in their termination process and transition to buyout when ready. Like the UK, the number of insurers participating in the US PRT market continues to rise, with more than 20 insurers now providing PRT de-risking solutions to plan sponsors.

One trend we’re watching in the US is a significant increase in buy-in transactions coming to market.

Source: The Purple Book 2024, PPF7800 Index as at 30 November 2024, including restated data from 31 March 2023 to reflect revised calculation methodology.

With global interest rates increasing across the board, pension plans on both sides of the Atlantic are enjoying their highest funding levels on record, which will doubtless serve as a catalyst for increasing PRT activity. However, when it comes to the potential of the global PRT market, how does the rest of the world compare? Aside from Canada, PRT markets elsewhere are in an earlier stage of development. Despite this, we see potential for global growth in the Netherlands, Ireland and – in the longer term – Japan. Canada After the UK and US, Canada is the next most well-established PRT market by a substantial margin. Indeed, 2024 constituted a record year for this market, with transaction volumes of over CAD $11 billion. As in UK and US markets, Canadian pension plans have seen an improvement in their funding positions driven by interest rate increases and positive asset returns, making PRT solutions more viable. 2024 saw a significant increase in inflation-linked plans coming to market, with over $3 billion of such transactions occurring. This demonstrates that PRT solutions are viable for all plans. Like the US and UK, the Canadian PRT market is competitive, with seven insurers currently serving as active market participants.

Canadian PRT Market Growth

Another characteristic of the Canadian market that is common in the UK and US is that market activity tends to skew significantly towards the second half of the year, as major transactions and increased transaction volumes are typically completed towards the year’s end.

IMAGE

Ireland While not the largest European market, the Irish DB sector is still considerable, comprising around 500 plans that total around €60 billion of liabilities. Recent analysis by Mercer2 of Irish Stock Exchange listed companies also suggested that plans were now over €1.1 billion in cumulative surplus, after many years of deficit. Mirroring the trends of the other global markets we have covered above, funding levels have improved as interest rates increased. Plans have de-risked and reduced the likelihood of significant deficits from future market volatility. Despite this, the PRT market in Ireland is currently small. Transaction volumes each year are low and focused on retiree-only populations. Despite this, green shoots of growth are visible – where solutions can be found for deferred members and Irish inflation-linked benefits, making the market’s progression is possible.

Mirroring the trends of other global markets covered, funding levels have improved as interest rates increased.

Japan The DB sector in Japan is well established and accounted for nearly ¥70 trillion of the total Japanese retirement market in 2024, according to recent research by the Nomura Research Institute. With the yield curve steepening in Japan, it has provided an economic backdrop for pension plans to consider the potential of PRT in the medium term. As Japanese industries evolve, we have seen a rise in M&A activity across Japan’s leading companies in automotives and electronics, which has in turn drawn a sharper focus on how their pensions liabilities are managed. While PRT is currently not permitted in Japan, it is a sector Japanese companies and their plans are familiar with, especially those multi-nationals with presence with US and the UK, some of whom have transacted with insurers already such as the Honda Group – UK Pension Plan. The Japanese insurance industry has been lobbying government to provide legislative reforms that would facilitate the potential for meaningful sector in Japan. While proposals have not yet been made into law, the issue is watched keenly by industry and corporate customers alike, who may be eager to transfer liabilities from a pension plan to an insurer. Through the creation of our long-term strategic partnership with Meiji Yasuda, we will continue to explore markets with PRT potential and will be monitoring developments as the sector in Japan evolves.

1. https://www.pensioenfederatie.nl/website/the-dutch-pension-system-highlights-and-characteristics 2. https://www.mercer.com/en-ie/about/newsroom/growth-bolstered-iseq-listed-companies-db-pension-plan/.

The Netherlands The Dutch PRT market emerged relatively recently and is driven by the long-awaited pension reform. Following the introduction of the Future Pensions Act (the “Act”) in 2023, the whole Dutch pension system is in the process of shifting from a DB-style model to a model with Defined Contribution (DC) characteristics, for both past and future benefits. The local market is in a transition period, with the pension transition for all plans set to have been completed by 1 January 2028. In between now and then, plans must establish new structures for future service, develop a transition plan for accrued benefits and overhaul administration systems so that they can comply with the Act. In the new system, if pension plans want to continue to offer guaranteed benefits for some of their members, this is typically only possible via an insurance solution (i.e. a buy-in or buyout). As with the UK and US, pension plans in the Netherlands are now often well-funded and many would be able to afford these guarantees. The Dutch PRT market is anticipated to unfold in multiple waves, with estimates of its ultimate size varying considerably, from as small as €20 billion to as large as €70 billion – regardless, its transition will be complete by the start of 2028. The first wave of transactions, involving smaller plans opting for buyouts rather than transitioning to the new system, is expected to conclude by the end of 2026. Between then and 2028, we also expect activity to involve plans transitioning accrued DB benefits into the new DC pension system under the flexible option (and seeking to offer some of their membership guaranteed options). After the transition period, we expect there still to be a PRT market for those plans that choose to run off their DB pension plan as their transition plan. While the trajectory and growth of the market is not yet completely clear, with €1.4 trillion1 in Netherlands-based pensions assets, it only takes a small percentage of pension plans to choose an insurance solution for a viable market to be created.

Macroeconomic headwinds aplenty Since the beginning of 2025, there have been a number of macroeconomic tremors, such as the release of Germany’s debt brake and a challenge to US leadership in AI technology. However, none has been more significant than April 2, ‘Liberation Day’, when US President Donald Trump introduced a new set of tariffs on global markets. This included a universal, reciprocal 10% tariff that was partially reversed a week later. The US economy has increasing projections for CapEx spending, despite tariff uncertainty. This has been reflected in the stock market following a period of underperformance earlier in the year. We expect tariff effects to become clearer likely in the Q3/Q4 timeframe and mostly affect consumer retail and energy space. Observers continue to keep a close eye on the performance of US assets, and in particular US bond prices. Given the influence of US bond prices on global markets, these market events will already have been impactful for the funding positions of UK pension plans given the consequent rises in UK bond yields and therefore UK market interest rates). Regarding the outlook, our economists had already made some significant adjustments to their US growth forecasts in anticipation of these tariffs. While we continue to believe that the US will narrowly avoid a recession, the headwinds to growth of trade disruption, uncertainty and reduced confidence could all potentially combine, resulting in a far larger impact to both the global economy and investments than has been suggested by estimates of the direct cost of tariffs alone. The political noise surrounding the EU–US trade negotiations was far from empty rhetoric. The Trump administration’s assertive tactics appear to have delivered results. The EU’s concessions, including the agreed tariff and substantial commitments on energy and defence procurement, reflect a pragmatic decision to avoid a more damaging outcome. For investors, we believe the short-term outlook has improved. The removal of the immediate uncertainty, alongside the recent agreement with Japan and ongoing negotiations with China, is providing greater clarity around the United States’ relationships with its major trading partners. Equity markets have recovered from their April jitters, and the target of 1% growth in the United States for the second half of the year now appears more achievable.

Following the gilt crisis in 2022, the resilience of LDI portfolios to interest rate rises has increased markedly

What does this mean for DB pension funds, including those looking to de-risk? While the broader narrative for DB plans in recent years – especially following widespread interest rate rises in 2022 – remains one of elevated funding levels, macroeconomic challenges in 2025 have often encouraged trustees to adjust their investment approaches to more closely align with insurer portfolios. Pension plans are currently more effectively hedged and de-risked than ever before, which supports the expectation that funding levels will remain strong. In terms of interest rate exposure, UK DB pension plans are on average around 80% hedged. This means that recent rises in rates are likely to have benefited plans on the basis that they are still 20% unhedged, as higher interest rates reduce the value of long-dated pension liabilities. Following the gilt crisis in 2022, the resilience of LDI portfolios to interest rate rises has increased markedly (thanks to higher hedge ratios and lower leverage), meaning that portfolios have been better able to accommodate the ongoing bond market volatility. Elsewhere in the world, DB plans have also navigated headwinds. With the US equity market dipping in early 2025 and plan liabilities increasing somewhat due to lower discount rates, average funding ratios of US plans fell initially in 2025. However, with US equities bouncing back over the early summer months and bond yields remaining high in a longer-term context, funding levels remain elevated compared to previous years. Similarly, Canada was initially impacted by developments in US equity markets and the broader geopolitical uncertainties of US tariff policy, with some Canadian DB plans adjusting their investment strategies to reduce their exposure to equities and favour fixed income.

While plans are affected by international macroeconomic factors, trustees’ responses are shaped by their own particular national contexts. For example, the transition of the Dutch pension system from a DB-style model to a DC-style model by 2028 mentioned above is driving changes to the investment approaches within the Dutch pension industry, rather than shorter-term macroeconomic trends. In Ireland, the combination of plans’ elevated funding levels and an uptick in the nation’s cost of living are intensifying calls for the approval of discretionary increase requests, while also enhancing the attractiveness of buyout. How DB plans should respond to macroeconomic factors, both in the short and medium term, depends on their circumstances, including their endgame planning, hedging levels and asset allocation of their investment portfolio. With interest rate levels currently high relative to recent history, pension plans that are not fully hedged may wish to consider increasing hedge ratios to ‘lock in’ any potential funding gains they have experienced. For some pension plans, the increase in yields is likely to have improved their funding positions to the point that a buy-in is now affordable.

While some DB plans may be less immediately impacted than others by market movements, we believe that monitoring markets and maintaining a strategic investment position that supports their endgame goals is fundamental. Pension plans should be prepared for ongoing elevated market volatility caused by the potential impacts of US tariffs, as well as wider debt and fiscal dynamics, and should ensure that they are ready to act appropriately. At L&G, our investment mantra remains to prepare, not predict.

Get in touch

If you have any questions about this report or would like more information about our products and services, please don’t hesitate to contact us.