Signals

Q4 2025

Global cybercrime estimated cost 2029 | Statista Global cybercrime estimated cost 2029 | Statista

1. 2.

Sign up for Mastercard Signals

Building a new value grid

Sources

The digital money trifecta

Executive summary

A convergent future

Strategic outlook

Conclusion

next

home

Navigate issue below

Share your feedback

New rails, digital infrastructures and digital currencies are evolving at breakneck speed. where once we had a singular system now we have a wide variety of technologies, platforms and players. The boundaries between traditional and digital finance are dissolving, unlocking possibilities that were unimaginable just a few years ago — and challenging every established rule.

Explosion of choice

Two powerful forces are reshaping the global landscape of value exchange.

listen to this section · 3:50 min

force one

Visionary interoperability initiatives will increasingly stitch together this emerging architecture, laying the foundation for a seamlessly connected global ecosystem. These efforts are essential to transform today’s patchwork of innovation into an intelligent infrastructure where value moves securely and intelligently across borders and platforms.

Convergence

force two

We go beyond the technologies and business models to explore the deeper implications for commerce, trust and opportunity. As agentic AI and programmable money take center stage, “intelligent interoperability” will define the next era.

This edition of Signals is your guide to the transformation.

At the heart of the transformation are three related phenomena:

The evolution of stablecoins, tokenized deposits and central bank digital currencies (CBDCs) is rewriting rules, unlocking speed, widening choice and realizing potential on an unprecedented scale.

Public and private rails are being enhanced and connected, forging a dynamic, multi-layered grid where value can flow instantly, securely and intelligently.

Alternative infrastructure

Autonomous agents are a catalyst for change, reinventing payments as proactive, programmable experiences where transactions happen in real time, with zero friction and infinite possibility.

AI-DRIVEN COMMERCE AND PROGRAMMABILITY

Global payments are entering a transitional era characterized by innovation across six vectors.

Money will move:

Real-time, 24/7 settlement.

Faster

across more cross-border corridors, rails and reaching more endpoints.

Further

Adapting to purpose and context.

Smarter

Fewer intermediaries, lower costs, smarter routing.

Cheaper

Stronger identity, fraud prevention, resilient rails.

Safer

Auditable, traceable and atomic transactions.

Verifiably

2-5 years

In the context of money movement, this period will be defined by the key topics of this analysis: stablecoins, tokenized deposits, CBDCs, new public and private payment rails and the application of programmability and artificial intelligence. These initiatives will often complement a financial institution’s core business but possess the potential to transform or even replace it.

Emerging technologies, business models and adjacent opportunities will be nurtured, piloted and scaled.

While the near future is about emerging infrastructure, the longer-term outlook is about creating viable options for a radically different future.

Genuinely new business models and market structures could be built entirely upon the technological foundations currently being laid.

5+ years

At present this is creating a market paradox: while user-facing payment experiences are becoming simpler and more intuitive, the underlying technical, regulatory and strategic architecture is becoming more complex. But in the future the imperative of interoperability will drive convergence in a way destined to transform how money moves and the global economy works.

The central argument of this Signals is that the myriad innovations defining the near future will not remain isolated or independent phenomena. Instead, they’ll converge to form a new ecosystem.

Agentic commerce

The big change starts with the transformation of money itself. Three forms of digital money are emerging as the foundational settlement assets for new payment rails. Each is associated with a different institutional actor and each is optimized for different use cases. Understanding their mechanics and their interplay is crucial to grasping the future of value transfer.

Stablecoins have quickly evolved from a niche tool for crypto traders into a powerful new instrument in the digital payments landscape — combining the stability of traditional currency with the speed, programmability and global reach of on-chain settlement. This programmable nature enables smart contracts, peer-to-peer transfers and decentralized financial services to operate in familiar units like dollars — making crypto’s infrastructure usable while avoiding its volatility.

Signal

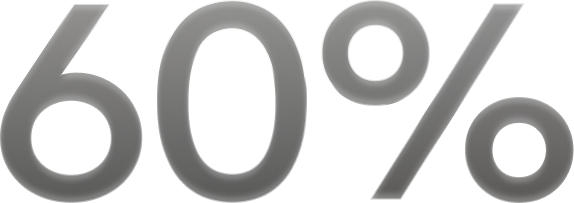

Stablecoins account for over 60% of on-chain transaction value with more than 1.5 million daily transfers.1

Market momentum

The U.S. GENIUS Act and the European Union’s MiCA are setting global benchmarks for stablecoin compliance.3

Regulatory clarity

Stablecoin supply grew by $4 billion in the single week after the GENIUS Act’s passage in July 2025.2

Rocketing growth

Stablecoin: Key characteristics

1 2 3 4

Price stability Reserve-backed Blockchain-native Always-on settlement

Pegged to fiat Backed by cash or other assets Issued on public or private blockchains Enables 24/7 near-instant transfers

MiCA's Stablecoin Regime and Its Remaining Challenges: Part 1 - Chainalysis European crypto-assets regulation (MiCA) | EUR-Lex https://www.cointribune.com/en/stablecoin-supply-surges-2025-genius-act/ Top Fiat-backed Stablecoins by Market Cap | CoinGecko Top Fiat-backed Stablecoins by Market Cap | CoinGecko Stablecoin-Payments-The-Trillion-Dollar-Opportunity.pdf Digital Cross-border Remittances to Reach $428 Billion in 2025 | Press Tokenized financial assets: From pilot to scale | McKinsey Central Bank Digital Currency Tracker - Atlantic Council https://www.atlanticcouncil.org/cbdctracker/ CBDC Transactions to Reach 7.8 Billion by 2031

1 2 3 4 5 6 7 8 9 10 11

previous

Mechanics

Stablecoins are blockchain-based digital tokens built to hold steady by pegging their value to a reference asset — usually a major fiat currency like the U.S. dollar. The model gaining most traction is the fully collateralized, fiat-backed stablecoin. Examples like Circle’s USDC and PayPal’s PYUSD operate much like digital money market funds: Every token is backed by liquid reserves such as cash and short-term government treasuries, with regular audits and public disclosures. This 1:1 backing lets issuers confidently promise redemption at face value, keeping the peg secure and trust intact. However, there’s a key difference with money market funds: Stablecoin operators earn interest on the reserves backing their tokens, but this revenue is not shared with holders. As a result, users who hold stablecoins miss out on the interest they could earn from traditional deposits or money market funds, creating an opportunity cost that should be considered when choosing stablecoins for payments or savings.

Regulatory clarity is turbocharging the stablecoin market. Frameworks like the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act and the Markets in Crypto-Assets (MiCA) regulation in the European Union have created clear rules for issuance, reserve management and consumer protection. This regulatory scaffolding is a critical catalyst, giving mainstream financial institutions and corporations the confidence to integrate stablecoins into their operations. Since the GENIUS Act’s passage, all of the biggest stablecoin issuers have applied for U.S. banking licenses.

Regulation

Stablecoin: Key points

Adoption is accelerating Suitable for on-chain payments Traction in cross-border transfers Merchant payments via stablecoin-linked cards

Driven by clearer regulation, broader use cases and insitutional uptake Offer a native 24/7 payment method for tokenized assets on public chains Remittances and disbursements are growing where traditional rails cost more and face more friction Stablecoins are increasingly used for payments to merchants via linked cards

The stablecoin market has achieved significant scale, with a total market capitalization now exceeding $300 billion.4 While the market has been historically dominated by Tether (USDT), regulatory pressures and institutional demand have propelled Circle's USDC to prominence as a more compliance-focused alternative. The entry of major payments players is a clear signal of mainstream acceptance: PayPal has launched its own stablecoin, PYUSD, while Mastercard has integrated stablecoin capabilities into its network.

Market outlook and key players

Stablecoin by market cap5

Tether (USDT)

Stablecoin

pegged to

type

USD Coin (USDC)

Ethena (USDe)

USDS (USDS)

USD

Fiat-backed

Crypto-backed

~$176B

~$74B

~$15B

~$8B

MARKET CAP

Largest stablecoin, widely used for crypto trading and cross-border payments.

Issued by Circle. Known for transparency, monthly reserve attestations; trusted by businesses.

Operates under a different framework than fiat-backed stablecoins.

Primarily crypto-collateralized.

Key features

Stablecoins are shaking up cross-border payments by making them fast, frictionless, cheap and transparent.

Stablecoin use case now: Cross-border payments

Predicted stablecoin share of cross-border payments by 2030.6

Growth in remittance transaction value 2021-257

Traditional cross-border transfer: Correspondent bank system

Time required: >3-5 DAYS

Company A, in the U.S., needs to send money to Company X, in France. It initiates a series of transactions across partner banks.

Expense

Each bank charges a fee.

Uncertainty

Exchange rates can fluctuate during the process.

Lack of transparency

Tracking money can mean calling or emailing banks.

Savings

Fee-charging partners are reduced or eliminated.

Company A converts fiat to the USDC stablecoin, then moves the USDC across the blockchain to the recipient, which can convert it back into fiat.

Time required: SECONDS

Stablecoin transfer: Cutting out the middlemen

Certainty

Speed cuts exchange rate risk.

Transparency

Full visibility on blockchain.

EFFICIENCY

No need to maintain cash in bank accounts.

Company A’s wallet

Company X’s wallet

Blockchain

Time required: Seconds to days

With on-ramp/off-ramp partners to handle fiat conversion:

Company A

On-ramp partner

Off-ramp partner

Company X

Stablecoins’ predictability makes them useful for recurring financial flows like payroll and lending, but their real breakthrough lies in conditional settlement — where payments settle automatically once a verified trigger occurs. This is enabled when digital currency is programmed with built-in logic so it behaves like software — executing actions based on code rather than human approval. For example, it can release or transfer funds only when delivery is verified. It also can route itself to different recipients, divide payments or interact with other systems like smart devices or financial platforms. We'll explore programmable payments in depth later in this report.

Stablecoin use case next: Programmable payments

"The future of payments will be shaped by the convergence of digital assets and programmable money. As we bridge traditional finance with blockchain-powered solutions, we’re building a foundation for commerce that is borderless, secure and infinitely adaptable to the needs of tomorrow’s digital society.”

Raj Dhamodharan Executive vice president, blockchain and digital currencies

A ride-hailing platform in Dubai pays workers every hour in a UAE Dirham-based digital token. Workers set a simple rule in their app — “send 30% of every payout to my family in Pakistan.” Funds are converted instantly to rupees and delivered to a linked wallet.

Instant income and sending money home

A look ahead

Plausible future

Faster, programmable payouts reduce churn and improve workforce loyalty while eliminating the need for third-party remittance processors. Workers receive more of what they earn, and platforms reduce payout overhead.

The upshot

Stablecoins are not the only vehicles for programmability. Tokenized deposits are the banking industry's own version of stablecoins, bringing the core product of banking — the commercial bank deposit — into the 21st century. As digital blockchain representations of traditional bank deposits, tokenized deposits inherit the full regulatory and trust framework of the traditional banking system, including deposit insurance schemes which protect account holders. They let banks offer the benefits of blockchain — such as programmability and real-time settlement — without requiring customers to move their funds outside the secure banking system.

Predicted size of asset tokenization market by 2030.8

Tokenized deposits are poised to have their most significant impact on domestic, high-value payment ecosystems, particularly in business-to-business (B2B) and corporate treasury contexts. By enabling 24/7 real-time transfers on a shared digital ledger, they can bypass the operational constraints of legacy, batch-based systems like Automated Clearing House (ACH) in the U.S. or the Single Europe Payments Area (SEPA) in Europe. Their most powerful capability, however, is atomic settlement. Traditional settlement processes are sequential, creating a window of counterparty risk where one party could default after receiving an asset but before making payment. Tokenized deposits can eliminate this risk by making the exchange an all-or-nothing event. This is a game-changer for corporate treasury functions, enabling ultra-efficient interbank lending, automated collateral management and real-time liquidity optimization across a firm's various accounts.

Modernizing B2B and treasury operations

Use case deep dive:

A multinational retailer holds tokenized deposits across several global banks. When FX rates shift or regional demand spikes, liquidity rebalances instantly across subsidiaries — 24/7, across currencies and institutions — using shared programmable ledgers. Transfers are atomic and compliant, replacing end-of-day sweeps with continuous optimization.

Treasury moves to real-time liquidity orchestration, achieving global visibility and instant redeployment of working capital across the enterprise.

Continuous, multi-bank liquidity orchestration

The development of tokenized deposits is being led by some of the worlds largest financial institutions, which see them as a way to modernize their core infrastructure. J.P. Morgan's JPM Coin is one of the most prominent early examples, used to facilitate instantaneous payments and settlement between the bank's institutional clients. Most current pilots and consortiums concentrate on wholesale and high-value B2B transactions, where the benefits of instantaneous settlement, reduced operational risk and enhanced liquidity management are most tangible and can justify the infrastructure investment.

Industry adoption and pilot programs

The third major form of digital money, the CBDC, represents the state's direct entry into the digital currency arena. A CBDC is a digital form of a country's fiat currency. It’s a direct liability of a central bank, making it the digital equivalent of physical cash.

CBDCs are a global phenomenon. Some 130 countries are at various stages of CBDC exploration.9 While only a handful of nations — primarily smaller economies like the Bahamas, Jamaica and Nigeria — have fully launched a retail CBDC, dozens of others are in advanced pilot or development phases. These include major economic blocs and nations whose actions will have global implications, such as China with its expansive digital yuan (e-CNY) pilot and the European Union, whose Central Bank has been preparing to launch a digital euro.

Global state of play

Digital yuan transaction volume rose

from 2023 to 2024.10

Forecast: Annual CBDC transaction numbers globally (billions)11

When a flood or earthquake is declared, a government issues CBDC-based relief directly to verified residents’ digital wallets — even if they’re offline or temporarily displaced. The funds are spendable on approved essentials such as fuel, food or shelter. Expiry dates prevent hoarding and unused balances return automatically to the relief fund.

Aid reaches citizens within minutes rather than days, with reduced fraud and lower delivery costs. Governments gain accountability and real-time visibility, while recipients gain dignity and immediate support.

Instant emergency aid

While retail use cases are some of the most compelling, CBDCs are pivoting from retail-focused ambitions to wholesale banking use cases, driven by practical challenges and strategic opportunities. Initially, retail CBDCs were promoted as tools for financial inclusion and cash reduction, especially in emerging markets. However, uptake has been slower than expected, and concerns around privacy, scalability and bank disintermediation have tempered enthusiasm. In contrast, wholesale CBDCs — designed for interbank settlements, cross-border payments and securities transactions — have gained traction due to their potential to modernize financial infrastructure and improve efficiency. This shift reflects a growing recognition that CBDCs may deliver the most immediate value by transforming the back-end plumbing of the financial system rather than the consumer-facing front end. In this context, the world’s largest economy stands out. Citing concerns around privacy and the potential for government surveillance, U.S. policymakers have so far resisted the development of a digital dollar, instead favoring a private-sector-led approach centered on regulated stablecoins.

The quiet pivot: Why central banks are betting on wholesale CBDCs

Despite the intense global activity, the path to widespread CBDC adoption is one of challenges and unresolved debates over privacy, control and systemic risk. Central banks face tough questions: Will CBDCs destabilize commercial banks by draining deposits? Can they scale securely without becoming surveillance tools? Public trust remains fragile — especially in countries where early launches have seen lukewarm adoption.

The unresolved debate

Each form brings distinct strengths — tokenized deposits preserve the integrity of the banking system, stablecoins offer agility and global reach and CBDCs provide sovereign trust and policy control. But rather than competing, these instruments will coexist within a shared digital infrastructure, enabling a more resilient, programmable and inclusive financial ecosystem. Together, they form a trifecta that redefines value in the digital age, unlocking new possibilities for commerce, settlement and monetary innovation.

These three digital monies — stablecoins, tokenized deposits and CBDCs — are not mutually exclusive.

Digital currencies compared

Dimension

Stablecoins

CBDCs

Tokenized bank deposits

Private issuer; claim on issuer/reserves

Issuer / liability

Regulatory status

Evolving; varies by jurisdiction

Split across many blockchains and issuers; bridges needed

High (smart contracts, DeFi composability)

Variable; on/off-ramp friction

Strong crypto primitives; weaker consumer protection

Mixed; issuer/wallet dependent

Wallet setup, gas, address risks; improving via custodial wallets

Promising but fragmented; FX & compliance hurdles

Very high; open global development ecosystems

Interoperability

Programmability

Speed & cost

Security & recourse

KYC/AML

Consumer experience

Cross-border

Innovation potential

Central bank; direct claim on the state

Public-policy instrument; bespoke legal framework

Commercial bank; same legal claim as a deposit, represented as a token

Fully regulated

Design-dependent

Medium-high (policy-driven programmability)

Near-instant, low cost

Strong operational resilience; public recourse frameworks

Strong, policy-mandated

Could be embedded in existing apps; policy choices shape UX

Potentially strong via central bank corridors (in pilot stage globally)

High; programmable by design but policy bounded

High within banking ecosystem; on-/off-ramps connect to blockchains

Medium-high via smart contracts; aligned with bank compliance/controls

Near-instant on permissioned rails; predictable fees

Bank-grade fraud prevention; established dispute and recourse rules

Strong; banks' existing controls extend to tokens

Familiar banking UX with "on-chain" features; abstracted keys via custody

Uses correspondent networks; tokenization streamlines transfers but remains policy-bound

High; large capability surface for trusted programmability

Key hurdles still exist, however. On-ramp and off-ramp partners are needed to handle conversion from fiat into stablecoin and back again. This takes longer, costs more and runs the risk of exchange rate volatility. At present there is also limited integration with the current financial system.

CORRESPONDENT RELATIONSHIP

BORDER

The second big change, after money itself, is the infrastructure it moves on. For decades, the global payments system has relied on a few well-defined routes — the underlying rails that move money. These include domestic batch systems like Automated Clearing House (ACH), card networks for consumer transactions and correspondent banking for cross-border transfers. These networks have delivered scale, reliability and trust, forming the backbone of modern commerce. Today, a new generation of payment rails is emerging. They aim to enhance programmability, real-time settlement and interoperability — and are designed for digital-native money and the complex logic of AI-driven commerce. Rather than replacing legacy systems, these new rails are layering on top and alongside them, creating a multi-rail environment where different networks intersect like a dynamic switchyard. Public digital infrastructure and private networks together form the layered architecture for this next era of payments — an ecosystem focused on speed and intelligence.

In many markets, governments are building digital public infrastructure (DPI) to modernize payments, expand financial inclusion and ensure self-reliance. The idea is simple but powerful: treat the core components of a digital economy — identity, payments and data exchange — as public goods, much like roads or electricity. These systems increasingly behave like messaging platforms — always on, traceable and rich in metadata. India’s Unified Payments Interface (UPI) and Brazil’s Pix are leading examples of DPI transforming national payment systems. Both offer real-time payments, simple user aliases (such as phone numbers or email addresses) and open access for banks, fintechs and other licensed providers. They have reset consumer expectations around convenience, reliability and inclusion.12

India’s UPI

Digital payment ecosystems and financial inclusion: Comparative analysis of UPI in India and PIX in Brazil UPI Transaction Witness 31% YoY Growth in September 2025 at 19.63 Billion: NPCI UPI Statistics 2025: Key Insights and Trends Shaping Digital Payments UPI Statistics 2025: Key Insights and Trends Shaping Digital Payments Pix Transactions Estimated 6.3 Billion in March Pix in Brazil: What to Expect in 2025 and beyond https://www.jpmorgan.com/kinexys/content-hub/deposit-tokens Mastercard Multi-Token Network - Enabling Digital Transactions 15% of Bitcoin Transactions on Coinbase Now Move Over Lightning Rails Powered by Lightspark

12 13 14 15 16 17 18 19 20

Brazil’s PIX

At their best, public rails compress costs and expand reach. They allow the state to fund the base layer, while the private sector competes on innovation and application. There are challenges, however. Most DPI systems are designed for domestic use, with cross-border capabilities still in development. Consumer protections vary widely and some systems rely on irrevocable transfers that shift the burden of dispute resolution to merchants and platforms. There are also sustainability concerns. Public funding may not be sufficient to maintain and upgrade DPI platforms, especially in low-resource settings where ongoing maintenance, upgrades and cybersecurity require significant investment. Additionally, they can suffer from bureaucratic inefficiencies, slower innovation cycles and governance challenges. When the state is both regulator and operator there can be concerns about data privacy and government surveillance.

Challenges and limits

Still, the trajectory is clear. In markets with DPI, instant domestic payments are the new baseline. These public rails are rapidly evolving from simple transfer mechanisms into data-rich communication channels capable of carrying structured metadata alongside value. This enables automated reconciliation, event-triggered settlement, real-time financing and embedded commerce models that operate with minimal human intervention. Yet DPI alone does not solve for every use case — particularly where programmability, cross-border reach or enterprise-grade assurance are required. That is where a new class of private and open rails is emerging.

The path ahead

A country’s DPI doesn’t just collect taxes or issue subsidies — it adapts to what is required in real time. At checkout, VAT and incentives adjust dynamically based on verified data from the national identity and registry systems: income level, region or sustainability goals. A farmer buying fertilizer receives a higher discount after a poor harvest. A commuter’s carbon subsidy changes automatically when they switch to public transport. Each rule executes through the DPI rail itself — no forms, claims or reconciliation.

DPI evolves from a payment and reporting tool to an active fiscal instrument. Policy becomes granular, data-driven and continuously adjustable.

DPI as a living policy engine

While DPI focuses on self-reliance, cost compression and inclusion, private and open rails are pushing the frontier in three critical areas: programmable settlement, cross-border reach and bank-grade assurance.

Some of the world’s largest banks now operate permissioned ledgers that represent commercial bank money as digital tokens. These systems allow clients to move funds 24/7 with near-instant finality, rich data and full regulatory compliance. The real breakthrough comes when these ledgers host both deposit tokens and tokenized securities. This enables atomic settlement, eliminates counterparty risk and unlocks new capabilities for treasury teams: intraday liquidity sweeps, automated collateral calls and event-triggered transfers tied to market data.

Tokenized bank money: Smart flows, regulated

J.P. Morgan’s Deposit Token (JPMD), launched in 2025, exemplifies this shift. Unlike earlier systems confined to internal networks, JPMD is designed for broader interoperability, marking a move toward a more open, composable infrastructure that’s still anchored in traditional banking. It’s a hybrid innovation — combining the programmability and speed of blockchain with the regulated, secure world of commercial banking.

Tokenized DEPOSITS

Money itself (used for payments and settlement).

Tokenized assets

Claims on something of value (used for investment and trading).

Permissioned

Available only to institutional clients that meet JPMorgan’s compliance standards.

JPMorgan – Deposit Token (JPMD)18 JPMD is a USD deposit token issued on Base, an Ethereum Layer 2 blockchain. It is:

Interoperable

Designed to work across public blockchain networks, not just JPMorgan’s internal systems.

Integrated

Tied directly to JPMorgan’s core banking infrastructure, offering interest payouts and deposit protection, unlike stablecoins.

Card networks remain essential — particularly for consumer payments that require strong identity assurance and dispute protection. Features like tokenization, push-to-account transfers and established chargeback procedures make them a trust-and-compliance layer even when the settlement occurs off-network. Modern card networks are increasingly positioned as the essential layer that enables seamless connectivity across the payments landscape.

Modernized card rails: Powering the payment continuum

Mastercard’s Multi-Token Network19 Mastercard’s Multi-Token Network (MTN) is designed to help banks, businesses and consumers move different types of money quickly, safely and smartly using blockchain technology. It supports tokenized deposits, stablecoins and real-world assets while preserving compliance and consumer protections.

MTN is a private blockchain supporting tokenized fiat, stablecoins, carbon credits and U.S. Treasuries.

Enables 24/7 real-time interbank settlement, programmable payments and app-initiated flows.

Partners include JPMorgan Kinexys, Fiserv and Ondo Finance.

Lightspark adds an enterprise-grade, interoperable layer to open rails, namely the Bitcoin Lightning Network. Its Universal Money Address (UMA) acts like an email address for money that works across wallets, banks and currencies. It allows users to send and receive payments across currencies and providers, with the routing and conversion handled automatically, and it offers enterprise-grade functionality such as liquidity management and compliance tooling. Fifteen percent of all Bitcoin transactions on Coinbase now move on Lightning rails via Lightspark.20

Open payment protocols are designed for speed and decentralization, but they lack the controls and guarantees that enterprises need to use them properly. To make them enterprise-ready, providers are layering added functionality, or “wrappers,” such as:

Compliance tooling

Integrating KYC/AML checks and regulatory reporting.

Managed liquidity

Ensuring there’s enough capital available to complete transactions smoothly.

Enterprise-grade blockchain: Wrappers that mean business

Uptime guarantees

Offering service-level agreements (SLAs) for reliability and availability.

Fraud controls

Adding monitoring and prevention systems to detect suspicious activity.

In payment corridors where speed, reach and always-on access matter most, blockchains provide a compelling alternative to traditional rails. Public blockchains allow messaging and settlement to occur in a single on-chain instruction — enabling transfers across time zones in seconds, with predictable fees and 24/7 uptime. Unlike bank transfers, the liability rests with the stablecoin issuer rather than a correspondent bank. Even so, the operational advantages are significant for scenarios like supplier payouts, marketplace disbursements and cross-border working capital. Programmability is authored by smart contracts, so workflows can include conditional releases, automated approvals or escrow-style logic without additional intermediaries.

Public blockchains: 24/7 finance

The common driver across these innovations is composability — not just the ability to combine different payment rails, but to assemble them dynamically based on context, whether optimizing for cost, speed, risk or compliance. To enable this, enterprises need systems that can evaluate conditions in real time, route accordingly and embed business logic directly into the flow of funds. Delivering that requires modern APIs, programmable interfaces and live data integration. In a composable landscape, the winners aren’t the owners of the rails, but the builders of intelligent control layers that orchestrate them.

Mix, match and move: The future is composable

A company sends a supplier payment through a treasury platform that acts like a smart router. The sender doesn’t pick ACH vs. stablecoin vs. card. Instead, it selects “fast,” “cheapest” or “in currency of receiver.” The system evaluates cost, settlement time and compliance requirements in real time, then executes across the optimal rail automatically.

Routing logic replaces rail selection. Liquidity is optimized as payment choice becomes a software decision rather than a human one.

Automated treasury routing

In another development SWIFT, the global financial messaging network that underpins most cross-border payments, recently announced plans to develop its own blockchain-based ledger as part of its infrastructure stack. The announcement marks a major shift. By embracing distributed ledger technology, SWIFT is signalling that legacy infrastructure is evolving to meet the demands of tokenization, programmability, and instant global payments.19

Mastercard’s Move is composability in action. It’s a global money movement platform that uses multi-rail architecture, dynamic routing and programmable interfaces to achieve secure interoperability at scale and speed.

Border

Business

Individual

“We are entering an era where the movement of money will be as seamless and intelligent as the movement of information. By connecting billions of endpoints across borders and currencies, we’re not just facilitating transactions—we’re laying the groundwork for a truly inclusive global economy where opportunity flows instantly to anyone, anywhere.”

Pratik Khowala | Global head of transfer solutions at Mastercard

The third big change covered by this report is the advent of autonomous transactions and embedded intelligence. Money will increasingly carry logic — able to release, route or prioritize itself according to preset rules — while AI agents initiate and manage payment flows on behalf of users and businesses. This turns payments from a reactive process into a proactive one. Instead of waiting for people to push funds, systems will anticipate needs, settle obligations as they arise and coordinate across suppliers, platforms and counterparties. The result is a step toward financial infrastructure that adapts in real time based on intent, context and opportunity. There are two elements to this: programmability and agentic AI.

With programmability, money is no longer just a medium of exchange — it becomes a tool for automation. Rather than simply transferring funds, systems can attach rules to them: release payment only when a shipment arrives, split proceeds across stakeholders or pause transfers if risk thresholds change. Payments stop being one-off instructions and instead become responsive workflows that adapt to events in real time.

The 2025 Global Payments Report | McKinsey Signals | Agentic Commerce | Q3 2025 - Summary

21 22

Two core technologies make this possible:

Smart contracts are automated agreements encoded in software. When a condition is met — delivery confirmed, certification approved, inventory scanned — the contract releases the payment without manual intervention. Running on blockchain-based infrastructure, the logic is transparent, verifiable and resistant to tampering.

Smart contracts

Atomic settlement ensures that every part of a transaction executes together. Either all steps complete or none do — removing the risk that one side delivers while the other fails to pay.

Atomic settlement

A global publishing platform integrates blockchain-based payment rails. It enables earnings from book sales to be batched and distributed daily in stablecoins to authors, editors and translators.

Lower settlement costs make small payments viable, enabling usage-based pricing models that reward ongoing engagement rather than one-time purchases.

Sustainable transaction revenue

How an agent-mediated programmable payment works

How it works

Agro Company B needs to stock up on fertilizer:

Sensor finds anomaly

Sensor confirms successful delivery

AI agent: Cancels transaction Extends escrow Requests human intervention

AI agent releases funds to seller

Benefits

The transaction executes fully (delivery and payment are simultaneous) or doesn’t process at all.

Atomic

Agentic AI systems can process thousands of transactions at the same time.

Scalable

Little need for human verification.

Efficient

Programmable payments are essential to the emerging field of agentic commerce because they enable autonomous agents — such as AI-driven shopping bots, supply chain optimizers or IoT devices — to transact without human intervention.

of consumers use AI to start their online shopping journey.

would be comfortable asking AI to purchase on their behalf.21

In this model, agents can negotiate, purchase and settle payments based on real-time data and predefined logic. A user might simply say, “Buy me a new pair of running shoes,” and the agent interprets preferences (brand, budget, delivery time), searches across retailers, compares options, reasons through trade-offs and completes the purchase. In this model, intent is expressed once, and the execution is handled entirely by software.

Authorization

How does a merchant confirm that an agent has spending rights?

This creates new questions for the financial system:

Authentication

How do participants verify if the agent’s action reflects the user’s intent?

Accountability

If a transaction goes wrong, who is liable — the user, the platform or the agent developer?

Recognizing both the opportunity and the risk, technology and payments providers are building new protocols to support agent-to-agent commerce. The Model Context Protocol acts as a universal interface layer, allowing agents to connect securely to tools and services — the digital equivalent of USB-C. The Agent-to-Agent Protocol enables agents to collaborate and negotiate across platforms. At the settlement layer, agentic payment systems such as Mastercard’s Agent Pay and Ant International’s EasySafePay allow agents to initiate programmable transactions with built-in controls.22 Crucially, these systems are designed to be payment-agnostic. They can move traditional card-based funds, stablecoins or tokenized deposits. That flexibility is essential for machine-to-machine commerce, where transactions need to be instant, conditional and executed at sub-cent precision.

New protocols and infrastructure

THE INDUSTRY RESPONSE

Split seconds, split payments and the agent’s cut

Agentic commerce doesn’t just change how transactions happen — it redefines who gets paid for making them happen. Today’s affiliate models reward human-driven funnels: clicks, impressions and last-touch attribution. But in an agentic world, autonomous agents — shopping bots, recommendation engines, supply chain optimizers — do the heavy lifting. They search, compare, configure, reserve and confirm, often across dozens of micro-interactions. Each of these touchpoints could trigger micropayments or streaming compensation, with programmable splits that reflect actual contribution. This flips the script: Instead of marketers and platforms capturing referral fees, agents themselves become the affiliates — earning for the value they create in the transaction flow. Traditional payments infrastructure struggles with this model:

A new model for referral economics

Compliance

Most systems assume a human pressing “buy,” not a machine executing contract logic.

Latency

Agents need millisecond-level confirmations while evaluating thousands of offers in parallel.

Economics

It was not built for millions of sub-cent or per-second transactions.

To support this future, agents may control pre-funded wallets and distributed ledgers may serve as transparent audit trails — tracking who did what, when and under what rules. Programmable safeguards such as escrow, spend limits or automatic refunds can replace blunt tools like chargebacks. This isn’t just a technical shift — it’s a new commercial architecture. One where attribution is dynamic, compensation is automated and agents are not just intermediaries — they’re earners.

A consumer tells her shopping assistant, “Find me the best price on noise-cancelling headphones.” The agent scans dozens of retailers, identifies price drops and negotiates bundled delivery. When it completes the purchase, the platform automatically identifies which agents contributed value — one discovered the product, another optimized shipping, another detected a price match — and splits a small referral fee across them, streaming payouts in tokenized currency at settlement.

Affiliate economics shift from static last-click models to dynamic contribution-based rewards. Instead of advertising platforms capturing referral value, agents — human-owned or autonomous — are compensated directly for verifiable influence.

Referral fees flow directly to agents

The path forward

The implication is clear: Payment infrastructure is becoming smarter. Businesses will need to support autonomous transactions, embed conditional logic and rethink how attribution, settlement and trust are mediated. Those that succeed won’t simply process payments — they’ll orchestrate value exchange across a network of machines, agents and programmable assets. The future of money movement is not just faster — it is more autonomous and deeply woven into the logic of commerce itself.

Intelligent money

"We are entering an era where the movement of money will be as seamless and intelligent as the movement of information. By connecting billions of endpoints across borders and currencies, we’re not just facilitating transactions — we’re laying the groundwork for a truly inclusive global economy where opportunity flows instantly to anyone, anywhere.”

Mastercard’s Move is composability in action. It’s a global money movement platform that uses multi-rail architecture, dynamic routing and programmable interfaces to achieve secure interoperability at scale and speed

Faster, cheaper payment rails are important, but programmability enables entirely new business models. It makes possible automated pay-on-delivery in supply chains, real-time liquidity management across accounts and compliance rules enforced directly within the transaction itself. These aren’t just streamlined versions of today’s processes — they’re the foundations for how business will operate.

The promise of seamless global payments is compelling — but not quite within reach. While the benefits of the new digital rails are clear, they remain siloed. A tokenized deposit on a bank's private ledger can’t interact with a stablecoin on the Ethereum blockchain, which itself is unusable on a national CBDC network. Without interoperability, these innovations risk becoming isolated islands of progress. Success depends on building bridges.

TIPS to connect to other fast payment systems globally Press Release: Introducing PayPal World: a global platform connecting the world's largest payment systems and digital wallets, starting with interoperability to PayPal and Venmo - Jul 23, 2025

23 24

The strategic question is therefore not which rail, platform or protocol wins, but how they converge such that value moves seamlessly across a single continuous payments fabric. A “network of networks” approach — pragmatic, multilateral and standardized — is emerging that delivers interoperability and “oneness” of money across forms and borders.

At checkout a customer selects “use best combination.” The system automatically draws $15 from a loyalty balance, $20 from a stablecoin wallet and the rest from a bank card — without any manual entry.

Retailers increase conversion and basket size, while consumers use stored value efficiently.

Mixed payment sources at checkout

A global marketplace pays 10,000 sellers daily. Instead of selecting a payout route, the finance department selects a rule — “pay as cheaply as possible, in line with terms and conditions.” The platform dynamically routes each payment based on geography, cost and liquidity — choosing such rails as SEPA Instant in Europe, RTP in the U.S., PIX in Brazil, and stablecoin rails like USDC on Solana or Ethereum for cross-border settlements. Where needed, it uses traditional card networks or SWIFT GPI for high-value or regulated corridors.

Cost and speed become programmable variables. Liquidity optimization moves from human judgment to machine execution.

Smart routing optimizes performance

Interoperability will deliver three key benefits:

Ease

Users and businesses will be able to move money across networks — whether card, account-to-account or blockchain — without friction or the need to understand the underlying complexity. A merchant will be able to accept payment from a card, a digital wallet or a stablecoin, with settlement and reconciliation handled seamlessly in the background.

Cost efficiency

Duplication will be reduced and smart routing will lower fees by letting transactions take the most efficient path — whether that’s a domestic instant scheme, a cross-border blockchain transfer or a card network. Multi-rail orchestration will unlock new business models and optimize liquidity.

Security

Protection will be end-to-end, traveling with the payment through the ecosystem, not staying confined to individual parts of it. This will mean harmonized authentication, fraud prevention and consumer protection standards that apply across networks. Card networks long ago set the benchmark for dispute resolution and liability; as instant payments and blockchain rails scale, these protections will be adapted and extended.

From central banks to private sector innovators, a range of players are working on creating interoperable infrastructures that support instant settlement, programmable flows and multi-currency capabilities. This convergence reflects a strategic shift toward coordinated financial ecosystems. Notable initiatives include:

Linking instant systems

The European Central Bank (ECB) is implementing a cross-currency settlement service to link its Eurozone TARGET Instant Payment Settlement (TIPS) system to other fast payment systems around the world.23 This means money in one currency could be sent from Europe and arrive instantly in a different currency in another country.

Project Nexus

TIPS is also joining Project Nexus, led by the Bank for International Settlements (BIS), which is connecting the fast payment systems of Malaysia, the Philippines, Singapore, Thailand and India. Rather than connecting to each other via the labor-intensive process of crafting individual APIs, systems will plug into BIS’s central hub — one connection replacing many.

Project Agorá

Another BIS-led project, this one involving 40 private financial institutions (including Mastercard) and seven central banks. Its goal is to modernize the correspondent banking model by developing a multi-currency unified ledger for wholesale cross-border payments, integrating tokenized commercial bank deposits with wholesale CBDCs on a programmable platform.

Blockchain bridges

Circle's Cross-Chain Transfer Protocol (CCTP) is a system designed to move the USDC stablecoin securely and efficiently between different, otherwise incompatible, blockchain networks. Lightspark's UMA standard represents a different approach, aiming to create a universal addressing layer that can sit on top of and abstract away the differences between various underlying settlement rails.

PayPal World

PayPal World launched recently to connect major payment systems and digital wallets to enable seamless cross-border transactions. By partnering with entities like Mercado Pago, UPI and Tenpay Global, it facilitates interoperability across wallets, allowing consumers to use their domestic payment methods internationally and businesses to access nearly two billion users without additional integration.24

Mastercard Multi-Token Network

Mastercard’s Multi-Token Network (MTN) is a permissioned blockchain infrastructure that enables seamless interoperability across payment systems by supporting tokenized deposits, stablecoins and real-world assets. It facilitates multi-rail orchestration, cross-network token compatibility and programmable payment flows via open APIs, while maintaining compliance through built-in governance.

From central bank-led projects to blockchain-based protocols to private sector platforms, this evidence of convergence points to a future where interoperability is not just a technical feature but a mission objective. As these systems mature and interconnect, they evolve toward a more inclusive, efficient and resilient financial landscape.

A U.S. tourist tips a driver in Nairobi using Apple Pay. The driver receives funds instantly in M-Pesa. Neither party has to download a new app or know what rail is used — conversion and routing happen invisibly via an interoperability layer.

Local payment schemes stop being silos. Regional wallets behave like global messaging apps — distinct brands, shared language.

Wallet-to-wallet across borders

Mastercard Move

Mastercard Move is a private network of financial institutions spanning 200+ countries, with direct connections into domestic and regional payment schemes. It reaches nearly 10 billion endpoints — bank accounts, wallets, cards and cash pick-up locations — across 150+ currencies. Payments can be delivered in near real time and accessed through local ACH or RTP systems. This design enables an international payment experience as seamless as a domestic transfer, eliminating the need for multiple intermediaries.

The next two to five years will be a critical transition period for global payments. Legacy infrastructure and digital-native systems will operate in parallel as regulation advances, pilots harden into production and new instruments move from experimentation into everyday use. Adoption will unfold in stages, as different technologies mature at different speeds and market incentives align.

The immediate horizon will be defined by the blending of traditional rails with programmable, digital-native infrastructure.

From 2025 to 2027.

In this phase:

Fiat-backed stablecoins gain regulated scale, moving from niche trading tools to standard instruments for cross-border remittances, merchant settlement and B2B flows.

Tokenized deposits shift from pilots to live deployment, with major banks using on-chain settlement for treasury, securities and commercial operations.

CBDC initiatives pivot toward wholesale applications and interoperability, integrating public-sector currency models with private-sector payment infrastructure rather than pursuing mass retail rollouts.

Card networks and instant payment schemes extend interoperability, exposing APIs that enable seamless payouts to cards, wallets and bank accounts — including those denominated in digital assets.

Blockchain protocols emerge as programmable settlement layers, bridging legacy ledgers with digital assets and enabling early automation and agent-led transactions.

Once foundational rails align, value will shift from connectivity to orchestration. Payments will increasingly be routed — and optimized — by AI rather than human choice.

From 2027 to 2030.

Stablecoins and tokenized deposits will become embedded across mainstream payment flows, supporting dynamic treasury, programmable invoicing and consumer incentives.

Card networks, real-time payment systems and blockchain platforms will be orchestrated through open APIs, allowing money and data to move fluidly across currencies, platforms and borders.

Interoperability will evolve from basic compatibility to intelligent routing, where transactions are automatically optimized for speed, cost, risk tolerance and user preference regardless of the underlying rail.

AI-driven commerce will mature, with autonomous agents negotiating, transacting and settling across multiple networks and asset types in real time.

A business never chooses a rail again. When it sends or receives money, software automatically selects — in milliseconds — the optimal route based on cost, speed, counterparty preference and compliance rules. The choice of network becomes as hidden as internet routing protocols.

Payments stop being a product. They become embedded infrastructure, with value created not through toll collection but through orchestration, liquidity intelligence and trust guarantees.

Payments become invisible infrastructure

Beyond the immediate challenges of technology and market adoption, there are deeper, more enduring questions about the kind of financial world we wish to build. The choices made now — about openness, governance, privacy and inclusion — will shape not only the architecture of payments, but the values embedded in our economic lives. Are we designing a system that empowers individuals and communities, or one that facilitates control and exclusion? Will our innovations foster trust, transparency and opportunity, or create complexity and uncertainty? The answers will emerge from the current interplay of policy, innovation and public discourse, guiding us toward a future where the movement of money reflects not just what is possible, but what is desirable:

Public vs. private

What will be the balance of power between public infrastructure (DPIs and CBDCs) and private-sector innovation (stablecoins and proprietary networks)? Will money and payments become more like a public utility or a field of competitive enterprise?

Will the future financial system be built on open, permissionless standards and protocols that foster a level playing field for innovation, or will it be dominated by proprietary platforms and the creation of walled gardens?

Open vs. closed

As AI routes more types of money across a wider mix of rails, how do we pair machine‑speed autonomy with clear, cross‑network accountability? Can consent, limits and purpose move with every payment, across every rail? Can audit trails and shared rules make liability clear from start to finish?

Autonomy vs. accountability

The path is complex, but the trajectory is clear. The organizations that build for flexibility, security and openness will be ready for what comes next. The winners will be those who connect the dots — making payments seamless, secure and accessible for all.

Mastercard powers economies and empowers people in 200+ countries and territories worldwide. Together with our customers, we’re building a resilient economy where everyone can prosper. We support a wide range of digital payments choices, making transactions secure, simple, smart and accessible. Our technology and innovation, partnerships and networks combine to deliver a unique set of products and services that help people, businesses and governments realize their greatest potential.

"We stand at a crossroads in the evolution of payments: never before have we had such diversity of choice, technology, and opportunity. Yet the true breakthrough will come from convergence—where interoperability transforms complexity into simplicity, and fragmented innovation becomes a unified ecosystem. Only then can we realize the true potential of intelligent and programmable payments."

Ken Moore | Chief innovation officer at