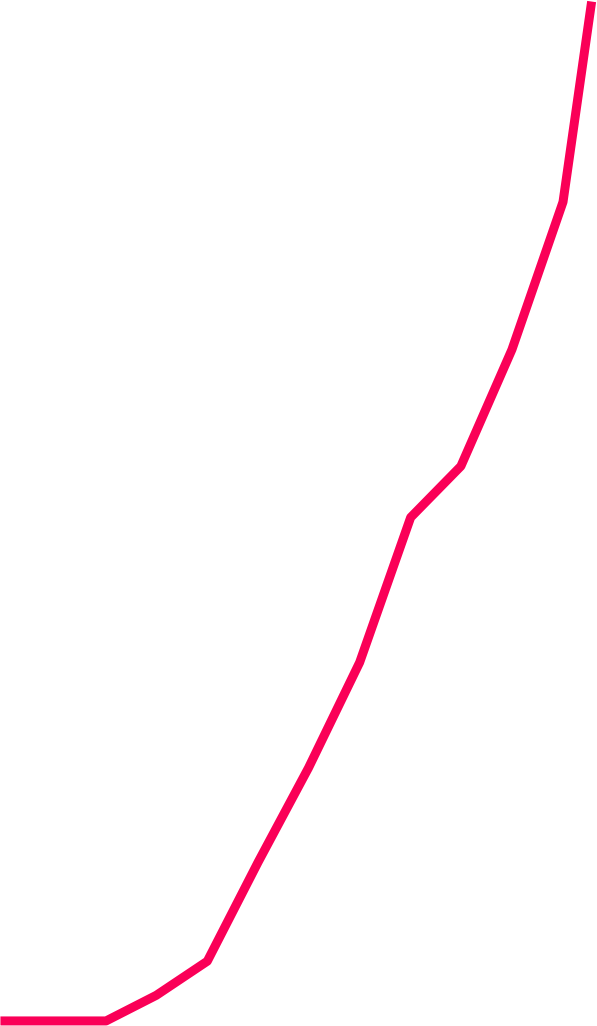

The OFR Financial Stress Index, a widely followed gauge of stress in financial markets, is rising although not to levels of previous crises.

A recent Reuters poll of economists predicts that the range will reach 4.75%-5% in early 2023 signaling further pressure to come.

4.75%-5%

Source: Reuters

Predicted hike range of fed funds rate in 2023

The UK’s gilt market crisis, triggered by the government’s “mini-budget” of September 23, signalled the fragility in markets.

They fell and their yields soared as investors sold, alarmed by the scale of unfunded tax cuts. The selling pressure was compounded as UK defined benefit pensions’ liability-driven investment (LDI) funds struggling with liquidity sold further gilts to meet margin calls. 30-year gilt yields rose from under 3.5% before the announcement to over 5%.

UK Gilts Crisis

Rising Rates With More To Come?

The U.S. Fed's Federal Open Market Committee is ratcheting up the pressure on markets as it raises the fed funds rate at the fastest rate since 1981. In December, the Fed implemented another increase of 0.5%, hoisting its target range to between 4.25% and 4.5%. The range was near zero as recently as March.

When stress in indebted financial systems rises, the risk of a liquidity crack-up mounts. At its root is usually a mismatch between the terms of lending or investing and the ability to repay. Financial crises can be triggered by large economic shocks or interest rate rises.

The index measures systemic financial stress – disruptions to the normal functioning of financial markets. When the index is zero it indicates that stress levels are normal. But a positive index including recent levels, indicates that stress is above average.

UK government bonds are not the only sign of fragility in financial markets.

At the end of November, the yen had lost more than 15% of its value against the dollar in 2022, as Japan’s zero interest rate policy radically contrasted with the U.S. Federal Reserve’s rapid tightening.

Extreme dislocations in markets such as this can put pressure on debt-funded positions and spark liquidity crises.

Japanese Yen Fragility

2015-19

1994-95

1987-89

2004-06

2022

Source: Federal Reserve Economic Data

Change in Effective Federal Funds Rate In Cycle (%)

2

4

0

10

5

0

40

45

30

25

20

15

35

The Fed is Hiking Further and Faster Than Any Time In Modern History

5

1

3

Months since hiking cycle began

Source: Reuters

In response, the Bank of England stepped in to buy gilts to avoid the funds collapsing.

The Bank also forced LDI funds to build up their liquidity defenses, stating publicly that more “stresses” could emerge as global financial markets adjust to the rapid rise in interest rates, with the “weak” points primarily in non-bank financial institutions like leveraged funds.

Weighted Average Level

OFR Financial Stress Index

Source: Refinitiv

Japanese Yen to USD

0.009

0.0085

0.008

0.0075

0.007

0.0065

Yen’s Decline vs Dollar Year-to-Date

Source: Refinitiv

Yield (%)

Liz Truss resignation

BoE ceases intervention

BoE widens intervention

BoE announces temporary targeted intervention

5

5.25

4.75

4.50

4.25

4

3.75

3.50

3.25

28

24

20

18

28

10

14

12

Oct 2022

Sept 2022

UK Long-Term Borrowing Costs Swing

30-year gilt yield (%)

Chapters Menu

CLOSE

Mar 2022

May 2022

Jul 2022

Sept 2022

Nov 2022

-10

-5

5

0

10

15

20

25

30

2022

2020

2018

2016

2014

2012

2010

2008

2006

2004

2002

2000

Credit

Equity valuation

Safe assets

Volatility

Funding

FSI

Source: Office of Financial Research

Explore

Explore

Explore

Explore

Explore

Select a Chapter to Continue:

Explore

Explore

Explore

Explore

Explore

Select a Chapter to Continue: