Reduce Motion

You’re committed to their future

time to care for yours

Explore how the NJEA-endorsed Income Protection+ Program—Disability, Hospital Indemnity, and Critical Illness Insurance Plans— can help secure your financial future if an injury, illness, or accident prevents you from doing what you love. This curated experience gives you the power to learn how to help protect your income with educational plan information, tools, and other resources.

See how your NJEA membership works to support you holistically.

Educators Insurance Services (EIS) is a team dedicated to helping NJEA members. Watch this video to learn more about our unique approach to supporting NJEA members.

Plan features, helpful information, & FAQs

View the videos below to learn more about what the EIS Team has to say about Disability Income, Hospital Indemnity, and Critical Illness Insurance—the only insurance plans endorsed by NJEA and designed to help protect you now and in the future.

Common plan misconceptions we’ve heard from our members.

Everything you’ve wanted to know about our plans and enrollment.

What is Disability Insurance?

What is Hospital Indemnity?

What is Critical Illness?

If you can’t work due to an accident or illness, this plan pays monthly benefits that can be used to help pay your rent, health insurancepremiums, childcare, or other expenses. Use our needs estimator to calculate what coverage amount may be right for you. Read more about the Disability Plan. Already have NJEA Disability coverage? Check out the Critical Illness Insurance and Hospital Indemnity Insurance plans. Ready to enroll? Visit enroll.njea.org.

Q: Won’t state disability cover me if I have a disability? A: NJEA members are not covered by state disability. This means that if a work absence is caused by an accident, illness, cancer, mental and behavioral health, you will have to rely on any accrued sick time and your savings.

View full list of FAQs

Your top questions answered

This plan helps with unexpected expenses that aren’t covered by health insurance if you’re admitted and/or confined to a hospital or ICU. Read more about the Hospital Indemnity Plan. Already have NJEA Hospital Indemnity coverage? Check out the Disability Insurance and Critical Illness Insurance plans Ready to enroll? Visit enroll.njea.org.

Q: I have health insurance—do I still need Hospital Indemnity Insurance? A: You might have great health insurance, but consider the non-medical expenses that could add up if you or a family member is sick or injured. This plan allows you to use your benefit money to help pay for things that health insurance is not going to cover.

If you can’t work due to an unexpected, life-changing illness, this plan offers fast access to money to use however you like for medical and non-medical expenses. Read more about the Critical Illness Plan. Already have NJEA Critical Illness coverage? Check out the Disability Insurance and Hospital Indemnity Insurance plans. Ready to enroll? Visit enroll.njea.org.

Q: Is it true that Critical Illness Insurance only covers cancer? A: No! Critical illness covers a range of illnesses. The plan pays a lump sum benefit if you’re diagnosed with conditions like cancer, heart attack, stroke, Alzheimer’s, Parkinson’s, and more.

Disability Insurance Read the article

Hospital Indemnity Insurance Read the article

Critical Illness Insurance Read the article

Read more about what the Income Protection+ Program offers NJEA members

Get to know your EIS Account Executives

We’re committed to you and your financial security. From identifying coverage gaps to answering your questions, we’re here to help build a plan that works for you. Click your school district/county to find your dedicated rep.

Ready to enroll? Great! Let’s walk you through the simple process or visit enroll.njea.org. Already enrolled? Give us a call and we’ll help make sure you have the right coverage for where you are in life.

We’re 100% dedicated to servicing you.

To us, it’s not about selling insurance–it’s about helping to protect you and your family’s financial future.

Resource Center

The EIS difference

Frequently asked questions

Download

NJEA Enrollment Forms (Disability, Critical Illness, Hospital Idemnity)

NJEA Brochures (Disability, Critical Illness, Hospital Idemnity)

Group Insurance coverages are issued by The Prudential Insurance Company of America, a Prudential Financial company, Newark, NJ. Prudential, the Prudential logo, and the Rock symbol are service marks of Prudential Financial, Inc. and its related entities, registered in many jurisdictions worldwide.

Educators Insurance Services (EIS) was incorporated in 1998 by Chuck Ray, who has worked with NJEA’s staff and members since 1977 to assist NJEA members like you. The EIS Account Team averages over 15 years of experience working with NJEA members, and over 2/3 of our team has family who are either State of New Jersey teachers or educational support staff. The dedicated team genuinely cares about members and honestly tries to help with any concerns, thanks to their broad understanding, connection to the community, and in-depth knowledge of the benefits available.

Caring for your mental health as an educator Read the article

Chuck Ray President 732-918-2000 (ext. 21)

Email me

Greg Longo Account Executive 732-918-2000 (ext. 31)

Leslie Kendus Account Executive 732-918-2000 (ext. 29)

David Knight Account Executive 732-918-2000 (ext. 26)

Megan Ray Senior Account Executive 732-918-2000 (ext. 24)

John Magrini Senior Account Executive 732-918-2000 (ext. 28)

Randy Hasbrouck Senior Account Executive 732-918-2000 (ext. 27)

Kelly Carella Account Executive 732-918-2000 (ext. 34)

Vince Pinto Senior Account Executive 732-918-2000 (ext. 30)

Kelly Ray Occhipinti Senior Account Executive 732-918-2000 (ext. 32)

Educators Insurance Services 732-918-2000

Email us

1079943-00004-00

View

Apply now

Ready to enroll?

Find your EIS Account Executive

Read more about the NJEA-endorsed plans

View FAQs and download resources

frequently asked questions about the NJEA Income protection program

return home

Disability Insurance

Hospital Indemnity Insurance

Critical Illness Injury

General

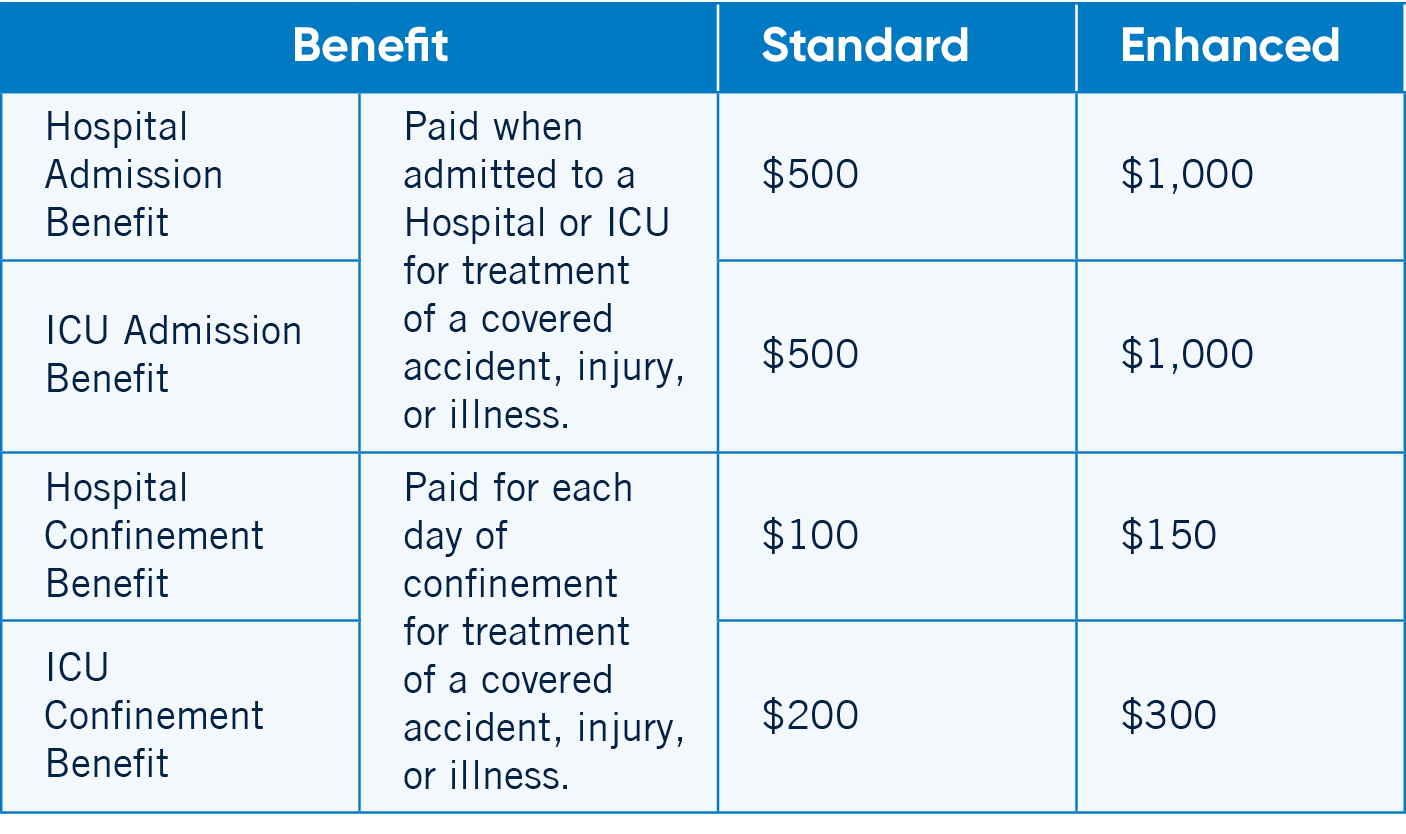

I have health insurance—do I still need Hospital Indemnity Insurance? You might have great health insurance, but consider the non-medical expenses that could add up if you or a family member is sick or injured. This plan allows you to use your benefit money to help pay for things that health insurance is not going to cover. For example, your spouse may have to stay overnight in a hotel and pay for meals and transport to and from the hospital to visit you. Hospital Indemnity Insurance pays a benefit if you’re confined to the hospital, which you can use wherever you feel it’s needed. Plus, you can add coverage for your spouse and children for added protection. What’s the difference between the standard plan and the enhanced plan? The standard plan pays you $500 for admission to a hospital and $100 each day after that for up to 30 days. The enhanced plan pays $1,000 or admission and $150 each day after that for up to 30 days. What does it cover? The plan pays a lump sum-benefit if you’re admitted and confined to the hospital. This benefit can be used for unexpected medical or non-medical out-of-pocket costs, to help avoid dipping into your savings.

Critical Illness Insurance

Is it true that Critical Illness only covers cancer? Critical illness covers a range of illnesses, not just cancer. The plan pays a lump-sum benefit if you’re diagnosed with conditions like, but not limited to: • Cancer • Heart attack • Stroke • Alzheimer’s • Parkinson’s How are benefits paid? Critical Illness Insurance provides you with a lump-sum payment when you are diagnosed with a covered illness. The speed at which benefits are paid is helpful for out-of-pocket up-front costs that accompany medical and non-medical expenses.

What is the difference between Open Enrollment at my school and the Statewide Open Enrollment? There are two types of Open Enrollments that you might experience. The first is a District Open Enrollment that occurs after a school visit from your EIS Account Executive and lasts for 60 days. These occur every three years. The second is the Statewide Open Enrollment in the Fall. This Open Enrollment begins at the start of the Annual Convention and lasts for approximately 60 days. However, the decision to hold a Statewide Open Enrollment is subject to annual approval and never guaranteed. Both of these Open Enrollments provide an opportunity to enroll in or change any coverage–with an option to increase your disability coverage by $500 and/or one Elimination Period (EP) without answering any health questions. How can the NJEA help me choose benefits that are best suited for my family? Your coverage needs will change as life and career events happen—whether you’re getting married, having children, or have children who have just left home. The EIS Team is here to support you every step of the way. The flexibility of the plans means you can find the coverage you need at various stages of your life. As your first point of contact, they are dedicated to helping you identify your coverage needs or possible gaps and building a plan that works best for you. How does the NJEA Income Protection Program impact my financial future? The NJEA Income Protection Program are the only insurance plans endorsed by NJEA and they are designed with members like you in mind. If you’re ever unable to earn an income due to a disability, accident, or serious illness, benefits from these plans will help you pay for medical and non-medical expenses so you can help avoid tapping into your savings. My salary just increased—how can I make sure my new income is covered? Your coverage won’t automatically increase as your salary does. You can make changes to your coverage online at enroll.njea.org, or contact your EIS Account Executive to make sure your income is fully covered. I just changed jobs, will this affect my coverage? No, you can keep your coverage if you change jobs or districts as long as you maintain your membership. However, if your salary increases with your new job, you may need to increase your coverage, which doesn’t happen automatically. When can I enroll for coverage? Anytime! During statewide open enrollments, you will have the opportunity to enroll in any level of coverage as well as review your current coverage and make changes if you need to. For example, during open enrollment, you’ll have the option to increase your disability coverage by $500 and/or reduce your elimination period by one increment without answering any health questions. Although statewide enrollment isn’t guaranteed every year, districtwide open enrollments occur once every three years. Contact your EIS Account Executive to see when open enrollment is planned for your district. How long does enrollment season last after you visit my school? It’s a 60-day window that opens the day your EIS Account Executive visits your school. If I’m a new member how long do I have to enroll? New members have up to 120 days to enroll. How often do you visit each school district? EIS Account Executives visit school districts once every three years. Is the NJEA Income Protection Program available to my family? Yes. You can also add family coverage, for your spouse/partner and eligible children for Critical Illness and Hospital Indemnity Insurance. How can I contact someone for more information? EIS Account Executives are here to answer your questions. Visit this link to find out which Account Executive supports your county. You can also call, 800-727-3414, or email info@educators-insurance.com.

Group Hospital Indemnity insurance coverage is a limited benefit policy issued by The Prudential Insurance Company of America, a Prudential Financial company, Newark, NJ. Prudential’s Group Hospital Indemnity Insurance is not a substitute for medical coverage that provides benefits for medical treatment, including hospital, surgical, and medical expenses, and it does not provide reimbursement for such expenses. The Booklet-Certificate contains all details, including any policy exclusions, limitations, and restrictions, which may apply. If there is a discrepancy between this document and the Booklet-Certificate/Group Contract issued by The Prudential Insurance Company of America, the Group Contract will govern. In Washington, the controlling document is the Certificate, not the Contract. Please contact Prudential for more information. Contract provisions may vary by state. Contract Series: 83500. Group Insurance coverages are issued by The Prudential Insurance Company of America, a Prudential Financial company, Newark, NJ. Prudential, the Prudential logo, and the Rock symbol are service marks of Prudential Financial, Inc. and its related entities, registered in many jurisdictions worldwide.

1081497-00002-00

Helping you prioritize your well-being You have the power to help secure the financial future you imagine for your family with three income protection plans that are endorsed by the NJEA: Disability Income, Hospital Indemnity, and Critical Illness Insurance. All plans are issued by The Prudential Insurance Company of America, one of the largest insurance companies with nearly 150 years of experience.

Critical Illness

Articles:

Return home

Caring for your mental health

Do I need to revisit my coverage once I have it? Your coverage won’t automatically increase as you move up in your career and your salary increases. It’s important to regularly revisit and increase your coverage to ensure you always have enough—your Educators Insurance Services (EIS) Account Executive can help! Find your dedicated Account Executive. Why do I need Disability Insurance if I have employer-provided sick days? Sick leave can help with expenses incurred during short bouts of work absence, but once you run out, you’re unpaid by the district, meaning it might not be enough to cover you if you get ill or are injured. Disability Insurance can help bridge the gap so that you’re covered even if you use up all your sick days. The coverage pays a benefit to help with monthly expenses to help keep you financially secure while you’re out of work. Will state disability cover me if I have a disability? NJEA members are generally not covered by state temporary disability insurance (TDB), which provides statutory benefits for up to the first 26 weeks of a disability. This means that if a work absence is caused by an accident, illness, cancer, or mental/behavioral health, you will have to rely on any accrued sick time and your savings to keep up with expenses and financial obligations. What does it cover? The plan covers accidents, illnesses, maternity, and mental health issues like stress, anxiety, and depression. If you become disabled due to any of these reasons and can’t work, you’ll receive a monthly benefit that you select at the time of enrollment that will help keep you on your feet while you’re not able to earn your own income. I’m young and in great health — why would I need Disability Insurance? No one likes to think about the possibility of getting sick or injured, no matter what age they are. But even if you’re in the best shape of your life, it’s important to protect your income if the unexpected happens. Disability Insurance can help provide financial security if you are unable to work due to a covered condition. It covers accidents, illnesses, maternity, and mental health including stress, anxiety, and depression. Aren’t NJEA members already covered by the state for disability? No. NJEA members are generally not covered by state temporary disability insurance (TDB), which provides statutory benefits for up to the first 26 weeks of a disability. What can I use my benefits for? Disability Insurance provides a monthly benefit that can be used to cover a range of medical and non-medical expenses like travel, lodging, mortgage payments, car payments, bills, and more. Disability Insurance is a maternity plan, right? Disability coverage under the NJEA Income Protection Program does provide benefits for maternity. However, one of the biggest misconceptions with the disability plan is that it’s only a maternity plan. In reality, it can help cover your expenses if you’re unable to work for an extended period of time, due to accident, illness, and mental health issues like stress, anxiety, and depression. What is an elimination period (EP)? This is the time period after your illness or disability begins but before your benefits start. For example, if you are out of work for 42 days and have an elimination period of 30 days, your benefits will kick in after the 30-day elimination period, meaning you’ll receive 12 days of benefits. There are different options for elimination periods depending on the plan you choose.

Disability Insurance 101 for Educators

Help protect your income

How would you support your loved ones if you couldn’t work?

As an educator, you devote so much of your life guiding the future of this country. But what happens when an unexpected disability prevents you from keeping the promise you made to your students and your family? With the NJEA-endorsed Disability Plan, you can help protect your income and savings with benefits that help ease financial burdens due to an accident, illness, or health condition.

Read articles:

1

2

3

4

Why is coverage important for you?

A number of injuries and illnesses could prevent or limit your ability to work as an educator. You could be injured in a car accident, have to undergo cancer treatment, or require mental health therapy, to name a few. Because a disability can happen to anyone at any stage in their life, this plan can help provide welcome relief from an unexpected challenge by covering a portion of your income if you were ever unable to work. This helps prevent dipping into your savings to support your financial obligations. It also pays benefits in addition to sick leave and, since school employees are typically not covered by New Jersey State Disability, you’ll have peace of mind knowing you’re covered if ever needed.

Most of us have life insurance to help protect our families if we pass away. But what if a disability or illness left you unable to work—and unable to earn an income? In addition to the loss of income, disabilities often mean medical costs and other expenses. While life insurance is designed to protect those left behind, disability insurance is important for now, whether you have a family or not. The plan has been designed to help protect your most valuable asset—your income—by providing monthly payments to help keep up with daily expenses if you’re unable to work.

What’s covered?

This plan covers most injuries, illnesses, or conditions that could prevent or limit your ability to work, such as: Accidental injury Cancer-related illness Childbirth and complications of pregnancy Mental and behavioral health

Monthly benefits to help pay for things like rent/mortgage, health insurance premiums, child care, college tuition, and more. Benefits pay in addition to sick leave and continue when sick leave is exhausted. Premiums are conveniently deducted from your paycheck.

Key plan features:

How does the plan work?

Choose a plan and benefit amount that suits your needs, whether you’re early in your career or later in life. Benefit amounts are available in $100 increments, from $500 to $7,500 per month (not to exceed 66% of your salary). If you’re diagnosed with a disability, the plan will provide your monthly benefit to you to help replace lost income if you’re ever unable to work, but the bills keep coming in.

Three plans to choose from:

PruProtect Plus Short- & long-term coverage

A combined short- and long-term disability plan with maximum coverage that helps to protect you for your working life (up to age 65). It also lets you select your elimination period.

A short-term disability plan that may be a good choice for those who seek a partial short-term income replacement solution. Members close to retirement age or with other resources to cover long-term absences may want to select this plan.

PruProtect Six-Month Short-term coverage for 6 months

Provides additional coverage for those who want coverage beyond six months and seek a partial short-term income replacement solution. Members close to retirement age or with other resources to cover long-term absences may want to select this plan.

PruProtect Two-Year Short-term coverage for 24 months

What about elimination periods and preexisting conditions?

Benefits for a covered disability are payable following an elimination period (your waiting period to receive benefits). For PruProtect Plus, you can choose your elimination period: 14, 30, 90, or 180 days. For PruProtect Six-Month and Two-Year, you can choose between a 14-day or 60-day elimination period. You should note, the longer the period, the lower your paycheck deduction. It’s also important to note that a disability will not be covered if it is related to a preexisting condition. A pre-existing condition is one that was diagnosed or treated during the three months prior to the effective date of your coverage. A disability that begins during the first 12 months and is due to a pre-existing condition is excluded.

1 in 4 of today’s 20-year-olds can expect to be out of work for at least a year because of a disabling condition before they reach the normal retirement age.*

Disability Insurance in action

Meet Lisa, a 34-year-old teacher with disability coverage endorsed by NJEA

Lisa enrolled for disability insurance when she was expecting her first child, and received benefits while she was out on maternity. A year later, things took an unfortunate turn and she was diagnosed with cancer. Luckily, she was prepared for this unexpected diagnosis with a plan that offered financial security during this trying time, helping her focus on her recovery. Lisa was grateful that she had stayed in the plan and still had access to benefits after her child was born. This hypothetical example illustrates how the plan helps provide financial security in times of need.

You can make a disability claim in one of two ways: 1. Call 1-800-727-3414, Option 1. 2. Register on prudential.com/mybenefits

How to make a claim:

Once a claim is initiated, Prudential will reach out to your providers for any medical documents they require. They may contact you for help securing these if they’re unable to do so. Prudential will then review your claim for eligibility (depending on which Disability Plan you are enrolled in) and come to a decision. Your Prudential Disability Claim Manager will contact you with the decision and, if applicable, discuss any return-to-work plans with you. Prudential will be in touch throughout your claim journey until your claim is closed. You can also access your claim status at any time and upload any supporting documentation online or through a mobile device.

Steps:

* https://disabilitycanhappen.org/disability-statistic/ This policy provides disability income insurance only. It does NOT provide basic hospital, basic medical, or major medical insurance as defined by the New York State Department of Financial Services. NJEA Disability Insurance coverage is issued by The Prudential Insurance Company of America, a Prudential Financial company, Newark, NJ. The Booklet-Certificate contains all details, including any policy exclusions, limitations, and restrictions, which may apply. Contract Series: 83500 Prudential, the Prudential logo, and the Rock symbol are service marks of Prudential Financial, Inc. and its related entities, registered in many jurisdictions worldwide.

1081480-00002-00

Helping you prioritize your well-being You have the power to help secure the financial future you imagine for your family with the NJEA-endorsed Income Protection+ Program—Disability Income, Hospital Indemnity, and Critical Illness Insurance Plans. All plans are issued by The Prudential Insurance Company of America, one of the largest insurance companies with 150 years of experience.

Hospital Indemnity Insurance plan 101 for Educators

Help supplement your medical coverage

How flexible are your finances in the face of the unexpected?

While your role as an educator or school support staff member probably means you’re used to adapting to change in an evolving, challenging environment, the same might not hold true for your paycheck. Injuries and illnesses that come with unexpected expenses can put strain on you both mentally and financially. The NJEA-endorsed Hospital Indemnity Insurance Plan can help provide peace of mind during trying times (such as an unexpected hospital stay) by covering expenses you may not have considered, including costs your primary health insurance won’t cover.

56% of Americans are unable to pay a $1,000 emergency expense.*

Hospital Indemnity Insurance Plan in action

Meet Susan, a 27-year-old school cafeteria worker with HIP coverage endorsed by NJEA.

Susan was seriously injured in a car accident on her way to work one morning and ended up spending five days in the hospital. But it wasn’t just a hospital stay… It was an ambulance ride to the ER, pet care while she was in the hospital, two weeks of missed work, and thousands of dollars in out-of-pocket expenses that her health plan didn’t cover. The accident was a major scare and a huge expense that she didn’t expect, even with great health insurance. Susan made a full recovery after two weeks and because she had the Enhanced Hospital Indemnity Plan, she received $1,000 for Hospital admission and $150 for each day confined so she didn’t have to take on any debt or dip into her savings. This hypothetical example illustrates how the plan helps provide financial security in times of need.

Benefits will not be paid for a Covered Accident, Covered Injury or Covered Illness caused, or resulting from a Preexisting Condition. A person has a Preexisting Condition when that person receives medical treatment, consultation, care or services, including diagnostic measures, or has taken prescribed drugs or medicines, or followed treatment recommendation in the 12 months just prior to the person’s effective date of Coverage and the person had symptoms for which an ordinarily prudent person would have consulted a health care provider in the 12 months just prior to the person’s effective date of Coverage.

What about preexisting conditions?

* CNBC, “56% of Americans can’t cover a $1,000 emergency expense with savings,” https://www.cnbc.com/2022/01/19/56percent-of-americans-cant-cover-a-1000-emergency-expense-with-savings.htmlopens in a new window. 1/19/2022. This coverage is not health insurance coverage (often referred to as “Major Medical Coverage”). This policy provides Hospital Indemnity insurance only. It does NOT provide basic hospital, basic medical, or major medical insurance as defined by the New York State Department of Financial Services. IMPORTANT NOTICE – THIS POLICY DOES NOT PROVIDE COVERAGE FOR SICKNESS. Hospital Indemnity insurance coverage is a limited benefit policy issued by The Prudential Insurance Company of America, a Prudential Financial company, Newark, NJ. Prudential’s Hospital Indemnity Insurance is not a substitute for medical coverage that provides benefits for medical treatment, including hospital, surgical, and medical expenses, and it does not provide reimbursement for such expenses. The Booklet-Certificate contains all details, including any policy exclusions, limitations, and restrictions, which may apply. If there is a discrepancy between this document and the Booklet-Certificate/Group Contract issued by The Prudential Insurance Company of America, the Group Contract will govern. Please contact Prudential for more information. Contract provisions may vary by state. Contract Series: 83500.

1081486-00003-00

Hospital indemnity insurance is a supplemental plan that complements your health insurance. You pay a monthly premium and, if you end up spending time in the hospital, you receive a fixed benefit amount paid directly to you to help cover expenses. Your lump-sum payment is yours to spend as you please, though people often use the benefits for deductibles, coinsurance, transportation, medications, rehabilitation, or home care costs. You can also use the money to pay for expenses incurred as you recover, such as groceries and childcare.

Guaranteed acceptance—no need for a medical exam Helps with costs not covered by medical benefits No requirement on where you spend the benefits

The plan helps you cover the cost of a hospital stay when receiving treatment for a covered accident, injury, or illness. It pays out after admission or confinement to a hospital or ICU, which can be used to cover daily living expenses, to make up for lost income, or to pay for out-of-pocket medical expenses.

Two plans to choose from:

Designed in response to today’s rising hospital costs, this supplemental plan complements your health insurance, paying in addition to what is covered. Even with a robust medical plan, you may not realize that a short hospital stay can add up to substantial out-of-pocket costs. The plan provides a direct benefit when admitted and/or confined to a hospital or intensive care unit, which can be used for both medical and non-medical expenses, making your recovery a little easier while you’re dealing with a tough situation.

What is the Hospital Indemnity Insurance Plan?

Accidents and illnesses can happen to anyone at any time and when they do, they can be expensive. Even a short hospital stay can add up to substantial uncovered costs. Specially designed for New Jersey Educators, the Hospital Indemnity Insurance Plan is an affordable supplement to health insurance. It helps provide a financial cushion if you’re met with unexpected hospital costs resulting from an injury or illness, so you won’t have to dip into your savings to meet your financial obligations.

Critical Illness 101 for Educators

Help protect your savings

Have you ever stopped to think how a serious medical diagnosis could affect your life?

You’re committed to making a profound and lasting impact on students’ lives. Their educational career starts with you, making your wellness key to their journey. Don’t let an unexpected diagnosis throw your journey (and theirs) off track. There’s a simple way you can help protect your financial future when life throws a curveball your way: The NJEA-endorsed Critical Illness plan, your safety net helping provide protection and security in the face of life’s uncertainties.

The plan helps to ease financial burdens and protect your savings when you’re dealing with a serious illness or health condition–so you can focus on your recovery and get back to doing what you love most. It’s more than just a cancer plan. There are a wide range of diagnoses that are covered, giving you peace of mind knowing that should an illness arise, you’ll have welcome relief and financial support during a very stressful time.

Being diagnosed with a critical illness is not only a devastating physical blow, but it can be a severe financial one as well. Even with health insurance, out-of-pocket medical and non-medical expenses can really cause financial strain. This plan helps protect your income and savings by easing financial burdens due to a covered illness or health condition.

What is Critical Illness Insurance?

The plan covers a range of illnesses and health conditions including:

Most claims are paid within seven business days Benefits are paid based on diagnosis, not treatment Receive benefits even if you’re not out of work Coverage available for members and their families

What about pre-existing conditions?

More than half of Americans live paycheck-to-paycheck, often leaving little or no money for unexpected emergencies like an illness.*

Critical Illness Insurance in action

Meet Dave, a 45-year-old bus driver with NJEA-endorsed critical illness coverage.

Dave’s world was turned upside down when he experienced a sudden stroke at home one evening. Fortunately, he made the wise choice to invest in Critical Illness Insurance through his membership, a decision that would prove to be a lifesaver in more ways than one. With the support of his coverage, receiving a lump-sum payment within a week of being diagnosed, he was able to focus entirely on his recovery without the added stress of financial obligations. With reduced income during this time, the plan provided Dave with the financial stability he needed to cover medical bills, rehabilitation costs, and more—meaning he didn’t have to stretch his budget to cover normal household expenses. And perhaps most importantly, it provided his family with peace of mind during one of the most challenging times of their lives. Thankfully, Dave emerged from his ordeal stronger than ever. This hypothetical example illustrates how the plan helps provide financial security in times of need.

*https://fortune.com/recommends/banking/more-than-half-of-americans-living-paycheck-to-paycheck/ April, 2023. This coverage is not health insurance coverage (often referred to as “Major Medical Coverage”). NJEA Critical Illness Insurance coverage is a limited benefit policy issued by The Prudential Insurance Company of America, a Prudential Financial company, Newark, NJ. Prudential’s Critical Illness Insurance is not a substitute for medical coverage that provides benefits for medical treatment, including hospital, surgical, and medical expenses, and it does not provide reimbursement for such expenses. The Booklet-Certificate contains all details, including any policy exclusions, limitations, and restrictions, which may apply. If there is a discrepancy between this document and the Booklet-Certificate/Group Contract issued by The Prudential Insurance Company of America, the Group Contract will govern. A more detailed description of the benefits, limitations, and exclusions applicable are contained in the Outline of Coverage provided at time of enrollment. Please contact Prudential for more information. Contract provisions may vary by state. Contract Series: 114774. Prudential, the Prudential logo, and the Rock symbol are service marks of Prudential Financial, Inc. and its related entities, registered in many jurisdictions worldwide.

1081491-00002-00

You and your spouse choose a coverage amount in increments of $10,000, up to a maximum of $200,000. If you have children, you can cover them for 50% of your benefit amount, to a maximum of $15,000. You’ll be covered in the first of the month after one full monthly deduction has been made. If you’re ever diagnosed with a covered illness, the plan will pay a lump-sum payment directly to you within a week of diagnosis. This money can be used for whatever you need to help keep up with unexpected expenses like babysitters, take-out food, deductibles, and anything else that may come up.

Note that a critical illness or procedure is not covered if it is related to a pre-existing condition, which is an existing health diagnosis you have in the 6 months before your coverage begins or the date an increase in your benefits would otherwise be available.

A critical illness or procedure is not covered if it is caused by, contributed to, or resulted from a pre-existing condition. A person has a pre-existing condition if both (1) and (2) are true: The person received medical treatment, consultation, care, or services, including diagnostic measures, from a doctor or took prescribed drugs or medicines, or followed treatment recommendation in the six months just prior to the person’s effective date of coverage or the date an increase in the person’s benefits would otherwise be available. The person’s critical illness or procedure begins within six months of the date the person’s coverage under the plan becomes effective.

Caring for your mental health as an educator

As an NJEA member, you’ve built a career supporting children through their educational experience. Whether you’re a teacher, bus driver, or custodian, or whether you’re more at home in the office or cafeteria, you play a pivotal part in their school journey. And while it can be rewarding, there’s no doubt that it can be stressful! The COVID-19 pandemic proved that demands in educational roles are ever-changing, which can make it easier to downplay your own wellness. However, if you’re struggling with the challenges of your career, you’re not alone. Take teachers as an example: Three-quarters of those who participated in the 2023 State of the American Teacher Survey said that they had accessed at least one type of well-being or mental health support in 2023, up 11% from 2022.1 Thankfully, there are some simple steps you can take to help support wellbeing and mental health.

For yourself:

You’ve probably heard that it takes a village to raise a child—the same is true for educating one! Your school is made up of a wide range of people in different roles, all playing their part to try and make things run smoothly. It can help to lean on the community around you for support. Having someone to talk to and trust at work can help contribute to positive well-being and mental health.

For each other:

Today’s lesson:

Learn how to care …

This can be as simple as spending more time with friends and family (people are 12 times more likely to feel happy on days that they spend six to seven hours with friends and family). And if you’re looking for activities to do together, a 30-minute walk in nature could increase your energy levels, reduce depression, and boost well-being. Small diet changes can also help—coffee consumption can lower rates of depression, while a few pieces of dark chocolate can improve alertness and mental skills. Meal prepping can help you include healthy foods more easily and has the added bonus of giving you a sense of control over your week!2

It can be easy to take work home with you, but creating boundaries between work and home is important for wellness. Get involved in an extracurricular activity, organize family dinners, or set aside time to watch a TV show with loved ones. And don’t forget about any furry family member you may have. Time with animals lowers the stress hormone, cortisol, and boosts oxytocin, stimulating feelings of happiness.2

For your family:

For many, finances can be a source of stress, but even small steps can help in alleviating the strain. Try creating a budget to highlight areas where you can cut costs—this might make it possible to set some money aside as a cushion for unexpected expenses. An income protection plan can also help you feel more secure about your finances—talk to an EIS Account Executive to discuss the plans available to you through your membership.

For the financial future:

Looking after your mental and physical well-being is very important, but if it’s something you find yourself struggling with, you’re not alone. Take advantage of the resources available to support you, so you can keep supporting your students the way you want to. It’s important to have a plan in place to support your loved ones if the unexpected happens. Your EIS Account Executive can help you create a coverage plan that protects both you and your family. Small changes can make a big difference when it comes to well-being. Study our list of ways to care for yourself, your loved ones , and your finances, and we’re sure you’ll ace it!

1 RANDD/Teacher Well-Being and Intentions to Leave, https://www.rand.org/pubs/research_reports/RRA1108-8.html, accessed April 2024. 2 Mental Health America/31 Tips to Boost Your Mental Health, https://mhanational.org/31-tips-boost-your-mental-health, accessed April 2024. Prudential, the Prudential logo, and the Rock symbol are service marks of Prudential Financial, Inc. and its related entities, registered in many jurisdictions worldwide.

1079943-00001-00