Will we have enough money to cover health care costs in retirement?

Meet Amy &

Sam Park

Is there a way to help ensure we can keep up with health care costs?

Amy and Sam, both in their late fifties, have well-paying jobs and are looking forward to retiring in a few years.

Their financial professional helps them understand their

potential medical expenses, and the different parts of Medicare,

and its premiums.

Amy and Sam are happy they met with their financial professional

to talk about a retirement challenge they hadn’t considered. They also have a better understanding of essential retirement expenses that are now considered in their financial plan. By incorporating FlexGuard Income into their overall financial strategy, they feel better prepared for the expected and unexpected health care costs in retirement.

Even if you've planned for retirement, you still may be concerned about essential expenses like health care.

Only 32% of retirees are “very confident” that they

will have enough money to take care of medical

expenses in retirement.

Total Medicare Cost Example – 2022

Unbundled coverage for a married couple with Adjusted Gross Income (AGI) less than $182,000/year

FlexGuard Income can provide Amy and Sam with lifetime income which can help them with health care costs in retirement. It also offers them choices to help them customize their income as their needs change over time. With FlexGuard Income, Amy and Sam can:

Annuities are issued by Pruco Life Insurance Company, Newark, NJ (main office) and distributed by Prudential Annuities Distributors, Inc., Shelton, CT. All are Prudential Financial companies and each is solely responsible for its own financial condition and contractual obligations.

This material is being provided for informational or educational purposes only and does not take into account the investment objectives or financial situation of any client or prospective clients. The information is not intended as investment advice and is not a recommendation about managing or investing your retirement savings. If you would like information about your particular investment needs, please contact a financial professional.

Annuity contracts contain exclusions, limitations, reductions of benefits, and terms for keeping them in force. Your licensed financial professional can provide you with complete details.

All guarantees including the benefit payment obligations arising under the annuity contract guarantees, any index strategy crediting, or annuity payout rates are backed by the claims-paying ability of the issuing company, and do not apply to the underlying variable investment options. Those payments and the responsibility to make them are not the obligations of the third-party broker-dealer from which this annuity is purchased or any of its affiliates.

You should carefully consider your financial needs before investing in annuity products and benefits.

Variable investment options are subject to contract and administrative fees.

Issued on Contract: P-FGI/IND(10/21), issued in ID P-FGI/IND(10/21)-ID

Issued on Rider: P-RID-VIB(10/21) and Schedule Supplement: P-SCH-VIB(10/21)

Issued on Endorsements: P-END-RILA-P2P(10/21), P-END-RILA-TPAR(10/21) and P-END-RILA-SRP(10/21)

© 2022 Prudential Financial, Inc. and its related entities. Prudential, the Prudential logo, and the Rock symbol, are service marks of Prudential Financial, Inc. and its related entities, registered in many jurisdictions worldwide.

ISG_DG_ANN46_01

1056210-00001-00

Employee Benefits Research Institute (EBRI), 2021 Retirement Confidence Survey

• Medicare is not free

• Medicare does not cover all of your health expenses

Bureau of Labor Statistics, Consumer Expenditure Survey 2019; Table 1300 Mean annual expenditures by age; Age 75+

On average, it’s expected that a healthy 65-year-old couple will need $300,000 to pay for medical expenses for the remainder of their lives.

3

Fidelity Benefits Consulting estimate, 08/31/2021. Health care and nursing home costs may vary by state.

*Buffers available on index-crediting strategies only. Variable investment options are available but do not offer protection levels.

Enhance the growth potential of income in up markets with unique crediting strategies before they start taking income

Wait to start taking income and potentially grow it each year that it is deferred, and participate in the growth potential of the market both before and after income begins

see note 1

•

•

•

How much money will you need?

Since Medicare is the primary source of health care coverage for most retirees, a good place to start planning is to work with your financial professional to understand what Medicare will actually cover.

Your financial professional can:

•

Show you strategies that include growth opportunities and protection

to help you address your health care costs in retirement

Help you estimate your future health care costs and incorporate them into your overall retirement plan.

•

•

In their spare time, they enjoy a variety of activities and place a lot of

importance on maintaining a healthy lifestyle.

In a recent meeting with their financial professional, they discussed their

plans to retire and their worries about financial risks they might encounter

as they age.

Amy and Sam's healthy lifestyle will likely give them more retirement years

to enjoy, but also more years to plan for financially. This could mean that

health care costs over time could deplete their retirement savings.

Amy and Sam also learned that Medicare won't cover all their medical expenses.

Annuities are issued by Pruco Life Insurance Company.

Any future changes in tax regulations could affect the calculations and assumptions made in this case study.

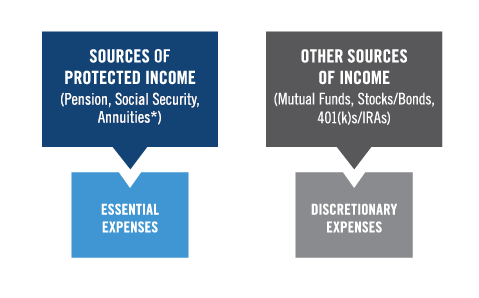

OTHER SOURCES

OF INCOME

(Mutual Funds, Stocks/Bonds, 401(k)s/s/IRAs)

*Annuities have different features and benefits, such as income benefits that offer different levels of income protection. Please ensure that you carefully review the features and options of any product or benefit before investing.

You’re not alone.

1

FlexGuard Income Brochure

Retirement

Income Worksheet

Learn about

health care considerations

in retirement

planning and how Medicare works

Take steps to create your own confident, healthy retirement by having a conversation with your financial professional.

Use the resources below to learn more:

Get started today!

Accessibility

The Parks story continued

The Parks story continued part 2

The Parks story continued part 3

The Parks story continued part 4

The Parks story continued part 5

The Parks story continued part 6

Calculate how much you will have

Explore the product's features and benefits

Receive a fully protected, fixed payment for life if their account value reaches zero

Together, they discuss developing a strategy that will help build their confidence in their ability to pay for these kinds of retirement costs.

Amy and Sam decide to create an income strategy with the Prudential FlexGuard Income indexed variable annuity to help them cover potential future healthcare costs.

1

2

2

3

®

Health Care Brochure

4

5

6

Learn about

health care considerations

in retirement

planning and how Medicare works

Calculate how much you will have

Explore the product's features and benefits

Investment and Insurance Products are:

• Not FDIC insured • Not insured by any federal government agency

• Not a deposit or other obligation of, or guaranteed by, the bank or any of its affiliates

• Subject to investment risks, including possible loss of the principal amount invested

FlexGuard Income and all product features are not approved for use in all states or through all broker-dealers.

Index-linked variable annuity products are complex insurance and investment vehicles and are long-term investments designed for retirement purposes. There is risk of loss of principal if negative index returns exceed the selected protection level. Gains or losses are assessed at the end of each term. Early withdrawals may result in a loss in addition to applicable surrender charges. Please reference the prospectus for information about the levels of protection available and other important product information.

Choose levels of protection with buffers* that may help limit losses for their assets and income

If your account value is reduced to $0, you move into the Insured Stage, and will continue to receive the last calculated Annual Income Amount as a guaranteed payment, for the rest of your life.

Text Alternative

Did you know?

Coverage out-of-pocket (prescriptions, vision, dental)

• Health care is the second largest expense in retirement

Disclosure:

Investing in FlexGuard Income's Index strategies does not represent a direct investment in an index.

Investors should consider the features of the contract, index strategies, and the underlying portfolios' investment objectives, policies, management, risks, charges and expenses carefully before investing. This and other important information is contained in the prospectus, which can be obtained from your financial professional. Please read the prospectus carefully before investing.

2

4. Kaiser Family Foundation "Medicare Part D: A First Look at Prescription Drug Plans in 2022," November 2, 2021

5. Median cost for Plan G male age 65 non-smoker in Overland Park KS (66013)

6. CMS.gov, “2022 Projected Medicare Part D Average Premium,” July 29, 2021

Chart shows the Total Medicare Cost Example, 2022 - Unbundled Coverage for Married Couple with AGI less than $182,000. Coverage Part A - average annual cost is zero. Coverage Part B - average annual cost is $2,041. Coverage Part D

average annual cost is $516. Coverage Medigap . average annual cost is $3,054.

average annual cost is $2,152. Total per person is $7,763.

Other sources of income (Mutual Funds, Stocks/Bonds, 401(k)s/IRAs) are Discretionary Expenses

Sources of Protected Income (Pension, Social Security, Annuities*) are Essential Expenses

*Annuities have different features and benefits, such as income benefits that offer different levels of income protection. Please ensure that you carefully review the features and options of any product or benefit before investing.

FlexGuard Income could help Amy and Sam cover their essential expenses

in retirement.

Their financial professional shows them that they have essential and discretionary expenses. Essential expenses are their basic needs (housing, food, health care), and discretionary expenses are the fun things that Amy and Sam dream of doing in retirement.

Their financial professional helps them understand that sources of protected income – like FlexGuard Income – can be used for their

essential expenses.

SOURCES OF

PROTECTED INCOME

(Pension, Social Security,

Annuities*)

DISCRETIONARY

EXPENSES

ESSENTIAL

EXPENSES

Average Annual Cost*

Total - Per Person

Coverage

Part A

Part B

Part D

Medigap

Out-of-pocket (prescriptions, vision, dental)

$0

$2,041

$516

$2,152

$3,054

$7,763