Text Alternative

ISG_DG_ANN30_01

1050623-00001-00

Issuing company located in Newark, NJ (main office). Variable annuities are distributed by Prudential Annuities Distributors, Inc., Shelton, CT. Both are Prudential Financial companies and each is solely responsible for its own financial condition and contractual obligations.

This material is being provided for informational or educational purposes only and does not take into account the investment objectives or financial situation of any client or prospective clients. The information is not intended as investment advice and is not a recommendation about managing or investing your retirement savings. If you would like information about your particular investment needs, please contact a financial professional.

A variable annuity is a long-term investment designed for retirement purposes. Investment returns and the principal value of an investment will fluctuate so that an investor’s units, when redeemed, may be worth more or less than the original investment. Withdrawals or surrenders may be subject to contingent deferred sales charges. Withdrawals and distributions of taxable amounts are subject to ordinary income tax and, if made prior to age 59½, may be subject to an additional 10% federal income tax penalty, sometimes referred to as an additional income tax. Withdrawals reduce the account value and the living and death benefits.

All guarantees including the benefit payment obligations arising under the annuity contract guarantees, any index strategy crediting, or annuity payout rates are backed by the claims-paying ability of the issuing company, and do not apply to the underlying variable investment options. Those payments and the responsibility to make them are not the obligations of the third-party broker-dealer from which this annuity is purchased or any of its affiliates.

Variable investment options are available, but do not offer levels of protection, and are subject to contract and administrative fees.

© 2022 Prudential Financial, Inc. and its related entities. Prudential, the Prudential logo, and the Rock symbol, are service marks of Prudential Financial, Inc. and its related entities, registered in many jurisdictions worldwide.

Issued on Contract P-RILA/IND(10/21), issued in ID P-RILA/IND(10/21)-ID

Issued on Rider: P-RID-RILA-ROP(10/21) (or state variation thereof)

Exceptions to the 10% federal income tax penalty – The penalty exceptions for employer plan and IRA distributions are not identical. Two exceptions apply to an employer plan, but do not apply to an IRA: separation from service at or after age 55, and Qualified Domestic Relations Orders. On the other hand, IRAs provide penalty exceptions for first-time home purchase and higher education, but employer plans do not.

Net Unrealized Appreciation (NUA) tax treatment – Favorable NUA tax treatment is not available to IRAs. Therefore, if you have highly appreciated company stock in your employer-sponsored plan, rolling that stock to an IRA eliminates the ability to take advantage of NUA tax treatment.

Creditor protection – While IRAs now have federal bankruptcy protection, they are not protected from other judgments the way that federal law (specifically ERISA) protects qualified plans.

New contributions to the employer plan – Taking an in-service distribution may affect your ability to make future contributions to the employer plan.

Loan – In the event that a 401(k) is terminated, the loan may be subject to income taxes and a federal income tax penalty.

Availability and Fees – It is important to check with your employer to see if they offer in-service withdrawals. Sources of information include your Plan Administrator, Summary Plan Description, or Participant Statement. Please consult these sources for any possible restrictions, fees and expenses.

Required Minimum Distributions (RMDs) – If you have attained age 70½ prior to Jan 1, 2020, your RMDs are required to begin at age 70½. If you have or are attaining age 70½ after Jan 1, 2020, your RMDs are not required to begin until age 72. Whether you are required to begin distributions at 70½ or age 72, the first distribution can be deferred to April 1 of the year following the year in which you attain your required distribution age. For subsequent years, distributions must be taken by December 31st. If you defer the first payment to the year following the year you reach your required distribution age, you will have to take two distributions within the same year. If you're a participant in an employer plan, and are not a 5% or greater owner of the sponsoring employer, RMDs must begin at the later of your required distributions age (70½ or 72), or when you retire from that employer. If you are a 5% or greater owner of the sponsoring employer, RMDs must begin at your required distribution age (70½ or 72).

Index-linked variable annuity products are complex insurance and investment vehicles and are long-term investments designed for retirement purposes. There is risk of loss of principal if negative index returns exceed the selected protection level. Gains or losses are assessed at the end of each term. Early withdrawals may result in a loss in addition to applicable surrender charges. Please reference the prospectus for information about the levels of protection available and other important product information.

Investment and Insurance Products are:

• Not FDIC insured • Not insured by any federal government agency

• Not a deposit or other obligation of, or guaranteed by, the bank or any of its affiliates

• Subject to investment risks, including possible loss of the principal amount invested

In-service withdrawals can be appropriate for many individuals. There are, however, some factors to consider:

Accessibility

Annuity contracts contain exclusions, limitations, reductions of benefits, and terms for keeping them in force. Your licensed financial professional can provide you with complete details.

You should carefully consider your financial needs before investing in annuity products and benefits.

Explore the product's features and benefits

FlexGuard Brochure

See FlexGuard's performance over time

History of

the Markets

Read about balancing risk and growth

Kiplinger Article

Talk to your financial professional about how FlexGuard may help you manage market volatility.

View the resources below to learn more about FlexGuard.

Take action today!

Jonathan takes a portion of his 401(k) and invests it into FlexGuard. He works with his financial professional to tailor the product to meet his goals and appetite for risk, giving him more confidence in his financial future.

FlexGuard also allows Jonathan to adapt and adjust his investment duration, growth potential, and protection levels as his financial goals change over time. Additionally, when Jonathan passes

away, if there is money remaining in the account, FlexGuard's guaranteed death benefit provides a legacy he can pass along to the animal rescue organization he supports.

Jonathan's story continued part 3

There are no annual contract or administrative fees when invested in the index strategies. Please note, not all crediting strategies are available at all broker-dealers or in all states.

Investing in FlexGuard's Index Strategies does not represent a direct investment in an index.

Enhance growth potential in up markets with two unique crediting strategies

ACCELERATE

Participate in the growth potential of the market

GROW

Select a level of protection that may help limit losses

PROTECT

FlexGuard index strategies can help him:

®

Together with his financial professional, Jonathan decides to explore this option. He contacts his 401(k) administrator and confirms that his plan allows for in-service withdrawals. His financial professional then introduces him to Prudential’s FlexGuard indexed variable annuity, which offers a level of protection, index-based growth opportunity, and the potential to accelerate growth beyond the index performance.

Jonathan's story continued part 2

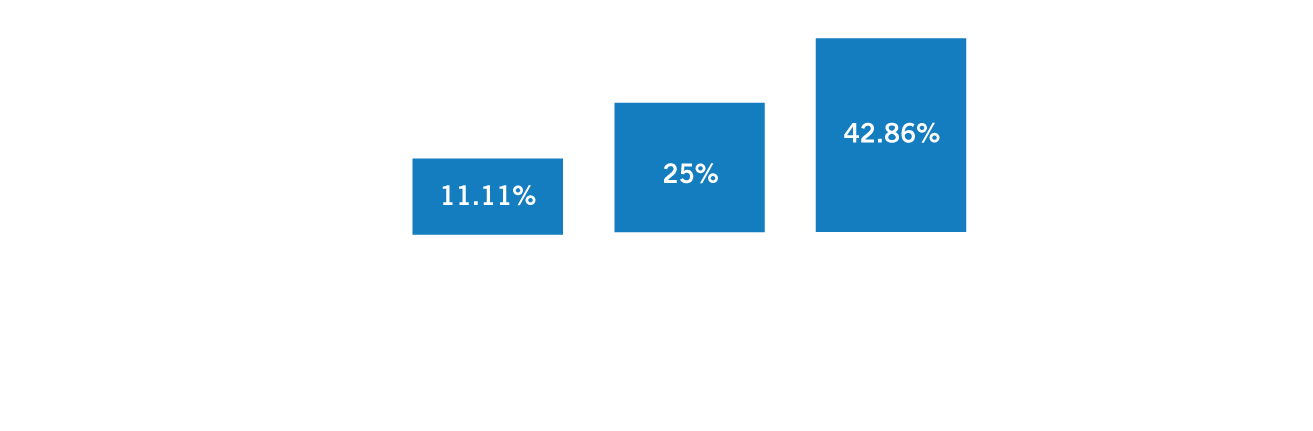

With a 20% loss and a 10% buffer, you would only need an 11.1% return to recover your loss, as compared to a full 25% if your investment had no buffer.

The buffer is the amount your Account Value is protected in the case of a negative index return.

What does it take to recover from a loss assuming you are protected from the first 10%?

Let's take a closer look

It is important to check with your employer to see if they offer in-service withdrawals. Sources of information include your Plan Administrator, Summary Plan Description, or Participant Statement. Please consult these sources for any possible restrictions, fees and expenses.

Click here to learn more.

Because Jonathan is concerned specifically about his 401(k), his financial professional talks with him about the in-service withdrawal concept. Even though he is still working, an in-service withdrawal would allow Jonathan to take a portion of his 401(k) money out and use it to fund an investment that can provide some protection against market loss as well as growth potential. The rest would remain in his 401(k) with the opportunity to grow.

His financial professional explains that some products, such as certain indexed variable annuities, can offer him the opportunity to grow his money for the future as well as a level of account value protection through buffers. Jonathan is glad to hear that he would even be able to customize some aspects of his investment to meet his individual needs.

Jonathan has seen his 401(k) dip significantly at points and becomes concerned about his own retirement. He contacts his financial professional to discuss his concerns.

Jonathan's story continued

This is a hypothetical example for illustrative purposes only. It does not reflect a specific annuity, an actual account value, or the performance of any investment. Chart assumes no withdrawals.

What percentage gain does it

take to recover from a loss?

Market Risk

Meet Jonathan

Is there a way to protect your portfolio if the market goes down?

Annuities are issued by Pruco Life Insurance Company.

*Yardeni Research, Market Briefing: S&P 500 Bull & Bear Markets & Corrections, April 25, 2022: https://www.yardeni.com/pub/sp500corrbear.pdf

®

•

•

•

•

•

Did you know?

You’ve worked hard to prepare for your future, but market downturns can have a significant impact on your financial plan. When you invest, it's expected that you'll experience market ups and downs, and even market corrections. But leaving yourself exposed to market losses can delay your retirement, disrupt your retirement lifestyle – even cause you to run out of money.

Can I protect my portfolio if the market goes down?

Return

to top

Return

to top

Return

to top

Return

to top

Explore the product's features and benefits

See FlexGuard's performance over time

Read about balancing risk and growth

Jonathan, a 60-year-old divorced engineer, is an avid animal lover who dedicates his free time to volunteering and fundraising for the local animal shelter. Jonathan saw family and friends struggle during the 2008 financial crisis when extreme market volatility and the resulting losses forced them to rethink what they could afford in retirement. Even when the market returned to former levels, some of them discovered that recovering from losses requires a significant market rebound just to get the account back to even.

Disclosure:

Investors should consider the features of the contract, index strategies, and the underlying portfolios' investment objectives, policies, management, risks, charges and expenses carefully before investing. This and other important information is contained in the prospectus, which can be obtained from your financial professional. Please read the prospectus carefully before investing.

A market correction is defined as a 10% loss from

the most recent market peak

A retiree will face 4 bear markets on average

during their retirement***

There have been 39 market corrections since 1950*

42% of corrections became bear markets**

A bear market is defined as a 20% loss from the

most recent market peak

**JP Morgan “Guide to the Markets, 4Q 2020; based on market activity post-WWII

*** Assumed retiree age 65 with anticipated death at age 90, and an average 6.8 years between market peaks in the post-WWII era

*Yardeni Research, Market Briefing: S&P 500 Bull & Bear Markets & Corrections, April 25, 2022