Share This Report

2025

Canadian REAL ESTATE REPORT

Economic uncertainty amid ongoing trade wars drives tactical shift in Canada’s top commercial markets in 2025

REMAX analyzed first-quarter activity across 12 major Canadian commercial real estate markets and found that investors are capitalizing on opportunities that allow for strategic repositioning, adaptive reuse and targeted investment, as escalating global trade tensions, economic concerns and evolving market conditions loom large.

"Canada’s commercial real estate market is shifting to fundamentals this year."

Don Kottick, President, REMAX Canada

Canada’s commercial landscape continues to evolve as investors and asset holders adapt to optimize portfolios and performance against a changing economic climate. Multi-family and industrial were the top-performing asset classes, followed by retail. Commercial markets continue to move forward at a steady pace, fuelled by ongoing pressure on the country’s existing housing stock, government policies set to advance growth such as the Housing Accelerator Fund, and a continued upswing in e-commerce sales.

Canada’s Commercial Growth Leaders in 2025

Western Canada’s commercial markets, alongside Newfoundland-Labrador, led the country in terms of commercial growth in 2025, buoyed by an increase in population, greater investment activity, and solid economic performance.

Read the Press Release

2025 Market Trends

Regional Highlights

Value of farmland and agri-industrial properties spikes in Saskatchewan. The farmland market climbed 13.1 per cent over 2023 levels despite inclement weather that impacted yields and commodity prices, according to Farm Credit Canada’s 2024 Farmland Values Report released in March 2025. Amalgamation of farming operations continues unabated.

Mid-market industrial with flex-space is popular with owner-occupiers. Demand for logistics, trades and manufacturing businesses remain high in markets including Calgary, Edmonton, Saskatoon and Winnipeg, with smaller flex industrial properties with one or two offices and warehouse space, proving ideal for owner-users and coveted by investors for steady rental income.

Grocery-anchored retail centres remain a preferred asset for private and public investors. Retail plazas continue to outperform, especially in suburban areas, attracting investors in Ottawa, Halifax, Winnipeg, Edmonton and the Greater Toronto Area (GTA). In addition to improving cash-flow, these assets offer future mixed-use redevelopment and/or intensification potential.

Office/retail-to-residential conversions continue, yet at a slower pace. Calgary and Ottawa continue to lead the country in terms of office-to-residential conversions. Calgary has 11 downtown office conversion projects approved and at least 20 buildings purchased for further redevelopment.

Trends to watch in 2025

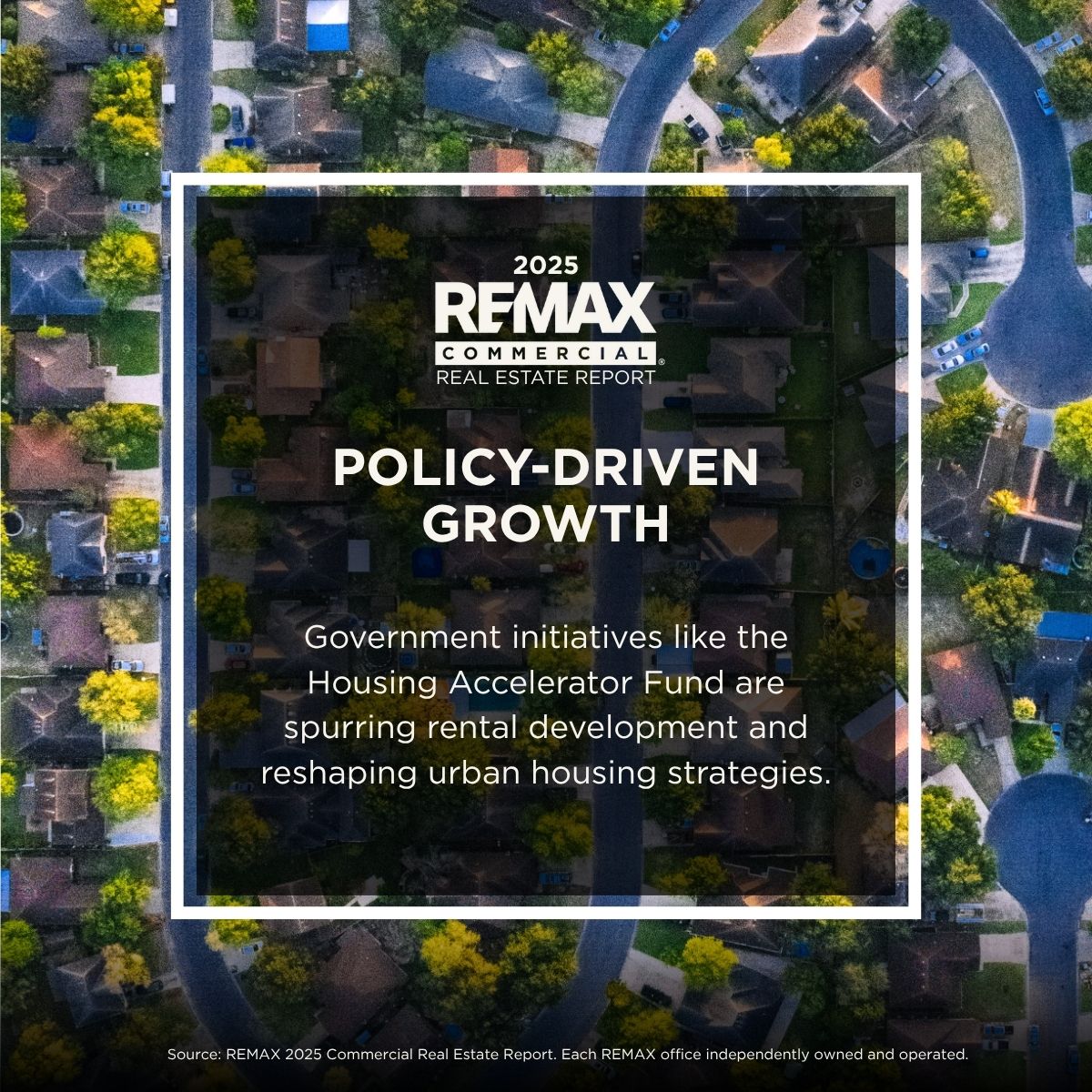

Government policy, including the Housing Accelerator Fund (HAF), has supported the recent upswing in multi-unit purpose-built rentals development. In fact, the federal government has earmarked an additional $74 million to top-performing HAF communities to fast-track construction of 112,000 new homes by 2028, by ending restrictive zoning, accelerating permits and advancing densification near transit and post-secondary institutions.

The number of new homes fast-tracked to 2028, thanks to the Housing Accelerator Fund.

Over the next decade, the program is forecast to create 750,000 new homes for people in towns, cities and indigenous communities across Canada. Yet, more stimulation is needed to address Canada’s housing crisis. The reintroduction of the popular Multiple Unit Residential Building (MURB) tax credit, directly responsible for the construction of close to 200,000 rental units in the 1970s, would further aid in expediting growth.

Regional Market Trends at a Glance

Seniors and students fuel demand for affordable housing. Conversion and repurposing of office buildings and renewed construction of purpose-built rentals offer solutions to the housing deficit in large urban centres including Toronto, Ottawa, London and Halifax.

Policy-Driven Growth

Industrial and multi-family asset classes have both experienced a serious upswing in inventory levels over the past year. An influx of new industrial product has softened absorption rates nationwide, prompting some tenants to pursue retrofits of older properties with lower lease rates. The same dynamic is playing out in multi-family markets, where increased inventory has eased rent pressures and pushed vacancy rates upward in traditionally tight markets like the GTA and Vancouver where vacancies are now climbing.

Shifting Investment Priorities

At present, investors are revisiting the value proposition in select markets. Development has stalled in cities such as Vancouver, where high interest rates and elevated construction costs have upended the value proposition and the viability of previously planned projects. More stimulus is required against a backdrop of increased distressed sales of condominium development.

Land Assets

Falling land values in the city have developers recalibrating, weighing the prospect to sell at a loss or hold until values recover while servicing mortgage debt and absorbing negative cash flow. Demand for development land has slowed as a result, with interest now shifting to income-generating properties that can ride out current headwinds.

"Land is no longer just about future potential—it’s about present performance. It’s about cash flow,” says Kottick. “Increasingly, investors value properties that deliver steady rental income to help portfolios weather market volatility and economic uncertainty.

Despite economic headwinds amid trade tensions, Canadian cities and towns have become increasingly popular destinations among Canadian and international tourists alike.

Industrial & Multi-Family Assets

Tourism Boosts Local Markets

Older multi-family building portfolios attract capital. In Greater Vancouver, Hamilton, Saskatoon and Halifax, REITs, institutional and small investors are pursuing aged multi-family assets that require revitalization, trade below replacement cost, and offer solid returns by rent optimization following modest renovation to boost curb appeal and the tenant experience.

The mall experience continues to transition. Foot traffic continues to diminish in older, dated shopping malls, with management introducing more service-related retail to their tenant mix, and some planning future residential development. Vibrant neighbourhood retail nodes are filling the void, offering a curated mix of retailers, services, dining, healthcare and beauty options, popular with both locals and tourists.

About the REMAX Network

�As one of the leading global real estate franchisors, REMAX, LLC is a subsidiary of REMAX Holdings (NYSE: RMAX) with more than 140,000 agents in over 9,000 offices with a presence in more than 110 countries and territories. REMAX Canada refers to REMAX of Western Canada (1998), LLC, REMAX Ontario-Atlantic Canada, Inc., and REMAX Promotions, Inc., each of which are affiliates of REMAX, LLC. Nobody in the world sells more real estate than REMAX, as measured by residential transaction sides.

REMAX was founded in 1973 by Dave and Gail Liniger, with an innovative, entrepreneurial culture affording its agents and franchisees the flexibility to operate their businesses with great independence. REMAX agents have lived, worked and served in their local communities for decades, raising millions of dollars every year for Children's Miracle Network Hospitals® and other charities. To learn more about REMAX, to search home listings or find an agent in your community, please visit remax.ca. For the latest news from REMAX Canada, please visit blog.remax.ca.

Forward looking statements

This report includes "forward-looking statements" within the meaning of the "safe harbour" provisions of the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements may be identified by the use of words such as "believe," "intend," "expect," "estimate," "plan," "outlook," "project," and other similar words and expressions that predict or indicate future events or trends that are not statements of historical matters. These forward-looking statements include statements regarding housing market conditions and the Company's results of operations, performance and growth. Forward-looking statements should not be read as guarantees of future performance or results. Forward-looking statements are based on information available at the time those statements are made and/or management's good faith belief as of that time with respect to future events and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. These risks and uncertainties include (1) the global COVID-19 pandemic, which has impacted the Company and continues to pose significant and widespread risks to the Company’s business, the Company’s ability to successfully close the anticipated reacquisition and to integrate the reacquired regions into its business, (3) changes in the real estate market or interest rates and availability of financing, (4) changes in business and economic activity in general, (5) the Company’s ability to attract and retain quality franchisees, (6) the Company’s franchisees’ ability to recruit and retain real estate agents and mortgage loan originators, (7) changes in laws and regulations, (8) the Company’s ability to enhance, market, and protect the REMAX and Motto Mortgage brands, (9) the Company’s ability to implement its technology initiatives, and (10) fluctuations in foreign currency exchange rates, and those risks and uncertainties described in the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in the most recent Annual Report on Form 10-K and Quarterly Reports on Form 10-Q filed with the Securities and Exchange Commission (“SEC”) and similar disclosures in subsequent periodic and current reports filed with the SEC, which are available on the investor relations page of the Company’s website at www.remax.com and on the SEC website at www.sec.gov. Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date on which they are made. Except as required by law, the Company does not intend, and undertakes no duty, to update this information to reflect future events or circumstances.

While 2025 was expected to be a year of recovery for Greater Vancouver’s commercial real estate market, tariff wars and recession fears prompted investors to shift into preservation mode, making strategic adjustments to their holdings that allow for maximum flexibility.

There has been some year-over-year improvement reported in areas including office and industrial leasing, with dollar volume transactions in the first quarter of 2025 up 10 per cent to $2 billion, according to Altus Group's Vancouver Q1 Report.

Greater Vancouver Area

Read More

Calgary

Robust immigration and interprovincial migration to the Calgary CMA in recent years have bolstered unprecedented expansion throughout the city’s residential and commercial real estate markets.

While the influx of new residents has slowed in recent quarters, supply shortages continue to exist across a multitude of commercial asset classes, including multi-family housing, which remains the top performer in Calgary, driven by REITs, institutional investors and out-of-province buyers.

Read More

1/12

2/12

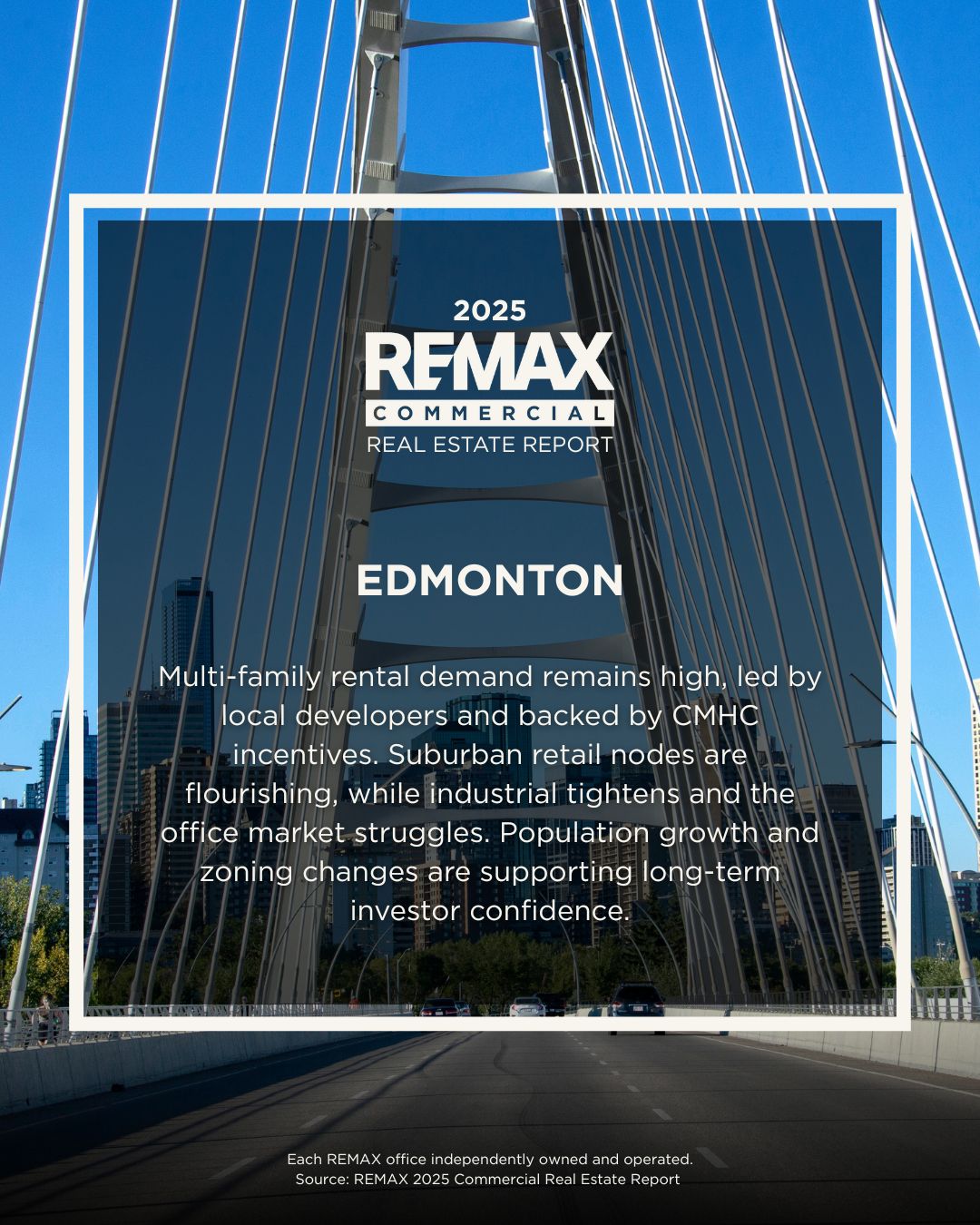

Edmonton

3/12

In the absence of larger institutional players in Edmonton’s multi-family asset class, mid-size investors and private buyers are playing an increasingly important role in city’s expansion.

Buoyed by ongoing population growth, multi-unit residential properties continue to be Edmonton’s strongest sector. Private developers, in partnership with local government, are committed to increasing the city’s rental housing stock in areas close to the University of Alberta, McEwan and Concordia as demand continues to exceed supply.

Read More

7/12

regina

Regina’s robust population growth has fueled a surge in commercial real estate activity, with multi-family housing achieving its best performance in a decade in 2024. Momentum has spilled over into the first quarter of 2025, with demand for multi-unit apartments from out-of-province investors climbing yet again, despite rapidly depleting inventory levels.

Much of the growth in multi-family has been achieved through the federal government’s Housing Accelerator Fund administered by the Canada Mortgage and Housing Corporation (CMHC).

Winnipeg’s commercial real estate market continues to gain traction, buoyed by sustained population growth and a renewed sense of energy across the city’s industrial, multi-family and retail sectors. Over the past two years, the city’s expanding population has sparked a level of activity not seen in recent memory, placing mounting pressure on available inventory and pushing both prices and competition higher.

At the forefront is the industrial sector, which remains the city’s strongest performer.

Read More

Winnipeg

Read More

4/12

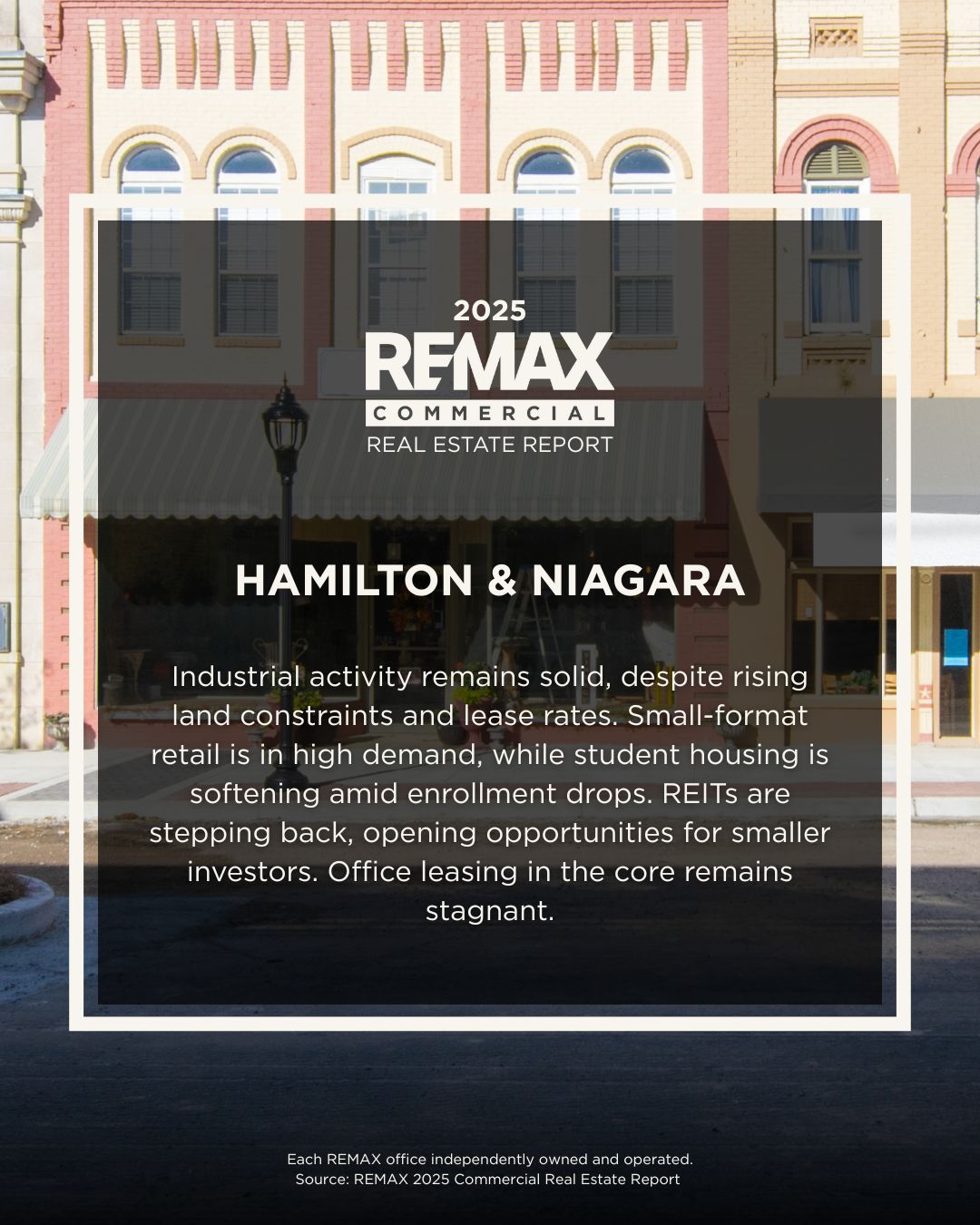

While tariffs on steel, aluminum and auto parts have had an impact on Hamilton’s commercial real estate performance this year, lower land costs continued to spur growth in the Niagara Region. Industrial sales were up significantly in Q1 2025 according to data from CoStar, with 11 properties sold, compared to five during the same period in 2024.

Despite a substantial increase in the number of industrial listings—up 35 per cent in Niagara and 33 per cent in Hamilton—lease rates continue to edge upward due to low vacancy rates.

6/12

London

Read More

While current trade tensions have yet to impact London’s commercial real estate sector, most businesses have adopted a wait-and-see attitude until greater clarity emerges. Two asset classes, however, have bucked the trend, with a marked shortage of industrial space driving healthy leasing activity, while population growth propels the city’s multi-family rental market.

Statistics Canada’s Annual demographic estimates, census metropolitan areas and census agglomerations: Interactive dashboard showed that London’s population rose 3.1 per cent to almost 630,000 between July 1, 2023, and July 1, 2024, bolstered by both international and intraprovincial migration.

Read More

Hamilton and the niagara Region

9/12

Greater toronto AREA

Read More

Looming trade wars continue to weigh on commercial investment in the Greater Toronto Area (GTA), with leasing and sales activity slowing year over year across nearly all asset classes.

While formal trade talks between the U.S. and Canada have yet to begin, and a resolution remains distant, the uncertainty in the market is creating opportunities for near-and long-term positioning of assets.

Industrial continues to be the top-performing sector in the GTA. Availability rates in Q1 2025 stood at 4.6 per cent, the second lowest in the country, but 40 basis points above last year during the same period, according to Altus Group.

8/12

10/12

Ottawa

Solid economic fundamentals continued to underpin Ottawa’s commercial real estate market, despite renewed concerns of a possible recession given current trade tensions. First quarter activity was strong out of the gate in the industrial and retail asset classes, with demand continuing to outpace supply.

While industrial availability rates have edged slightly higher over the past year, Ottawa remains the lowest in the country’s top eight industrial markets, sitting at 4.3 per cent, according to Altus Group’s quarterly industrial update for Q1 2025. Smaller light industrial buildings remain most coveted, especially those with good ceiling height (21 ft.) and loading docks.

Read More

5/12

Read More

Saskatoon

While economic uncertainty is causing some hesitancy in Saskatoon’s commercial real estate market, year-over-year transactions were up in the first quarter of 2025, with a significant uptick noted in leasing activity.

One hundred and seventy-six transactions occurred in the city, an increase of two per cent over the same period in 2024, even as tariffs, reduced immigration levels, and an undervalued Canadian dollar prompted many investors to hit the pause button.

Despite the disruption caused by U.S. tariffs, activity in Halifax’s commercial real estate market remains steady, though off year-ago levels. Confidence exists across the board, but much of the movement is now driven by necessity. While some buyers and tenants are capitalizing on current opportunities, many others—along with landlords and sellers—have adopted a cautious, wait-and-see stance as they seek economic clarity.

Industrial assets continue to be most active In Halifax, although seeing a significant shift this year. A substantial influx of new space has driven industrial availability rates higher, climbing to 12.7 per cent in the first quarter of 2025, up substantially from the 7.1 per cent reported during the same period last year, according to Altus Group.

11/12

HALIFAX

Read More

Read More

NEWFOUNDLAND-LABRADOR

Buoyed by offshore oil production and strength in manufacturing, Newfoundland-Labrador is expected to lead the country in terms of GDP growth for the second year in a row. While significant capital investment in mining, energy and infrastructure projects is occurring throughout the province, the impact on the commercial real estate market has been limited to date.

Fifteen commercial transactions were reported in Newfoundland-Labrador over the $500,000 price point between January and April of this year on the province’s MLS system—including a commercial mix building that sold for $4.2 million. Last year, just seven commercial properties changed hands, with the most expensive selling for $2 million in Labrador City.

12/12

Fundamentals are now driving decision-making and creative approaches to unlocking new value,” says Kottick. “The opportunities are there—for those that are prepared to rethink, reinvest and reposition. The good news is investors tend to easily adapt, pivot and embrace flexibility—an art in and of itself and a primary factor underpinning resilience in Canada’s commercial market. As a result, activity is expected to remain stable, regaining further momentum once economic performance improves."

© 2025 REMAX, LLC. Each office is independently owned and operated.

Newfoundland& Labrador

Newfoundland-Labrador’s growing pipeline of resource and infrastructure projects is helping the province enter a period of renewed economic momentum.

Western Canada

Steady immigration and interprovincial migration in Alberta, Saskatchewan and Manitoba helped spur expansion, with shortages reported in several asset classes.

K

112

While smaller, traditional malls continue to experience challenges, retail is proving resilient overall, with neighbourhood nodes outperforming – especially those anchored by essential shops and services. Although growing pains are expected, commercial markets are ultimately positioned for growth once the market shakes current transitory challenges and clarity emerges.

The most resilient and opportunity-rich markets are those where investors are proactively reshaping aging or underused assets to align with present and future demand.

Search Commercial Listings

Ready to explore opportunities in commercial real estate?

Read Our Blog

Stay up to date on commercial market trends and insights.

Population growth continues to propel the multi-family asset class. Bolstered by public policy, private and public investment is driving a resurgence in the construction of purpose-built rentals nationwide, while demand remains strong for existing portfolios. Industrial is the backbone of the commercial sector, with growing strength in the country’s logistics corridors.

At present, investors are revisiting the value proposition in select markets. Development has stalled in cities such as Vancouver, where high interest rates and elevated construction costs have upended the value proposition and the viability of previously planned projects. More stimulus is required against a backdrop of increased distressed sales of condominium development. Falling land values in the city have developers recalibrating, weighing the prospect to sell at a loss or hold until values recover while servicing mortgage debt and absorbing negative cash flow. Demand for development land has slowed as a result, with interest now shifting to income-generating properties that can ride out current headwinds.

Alberta, Saskatchewan, Manitoba and Newfoundland-Labrador lead the country in commercial activity