Copyright © 2023 Spotlight Sports Group. Produced by Spotlight Sports Group

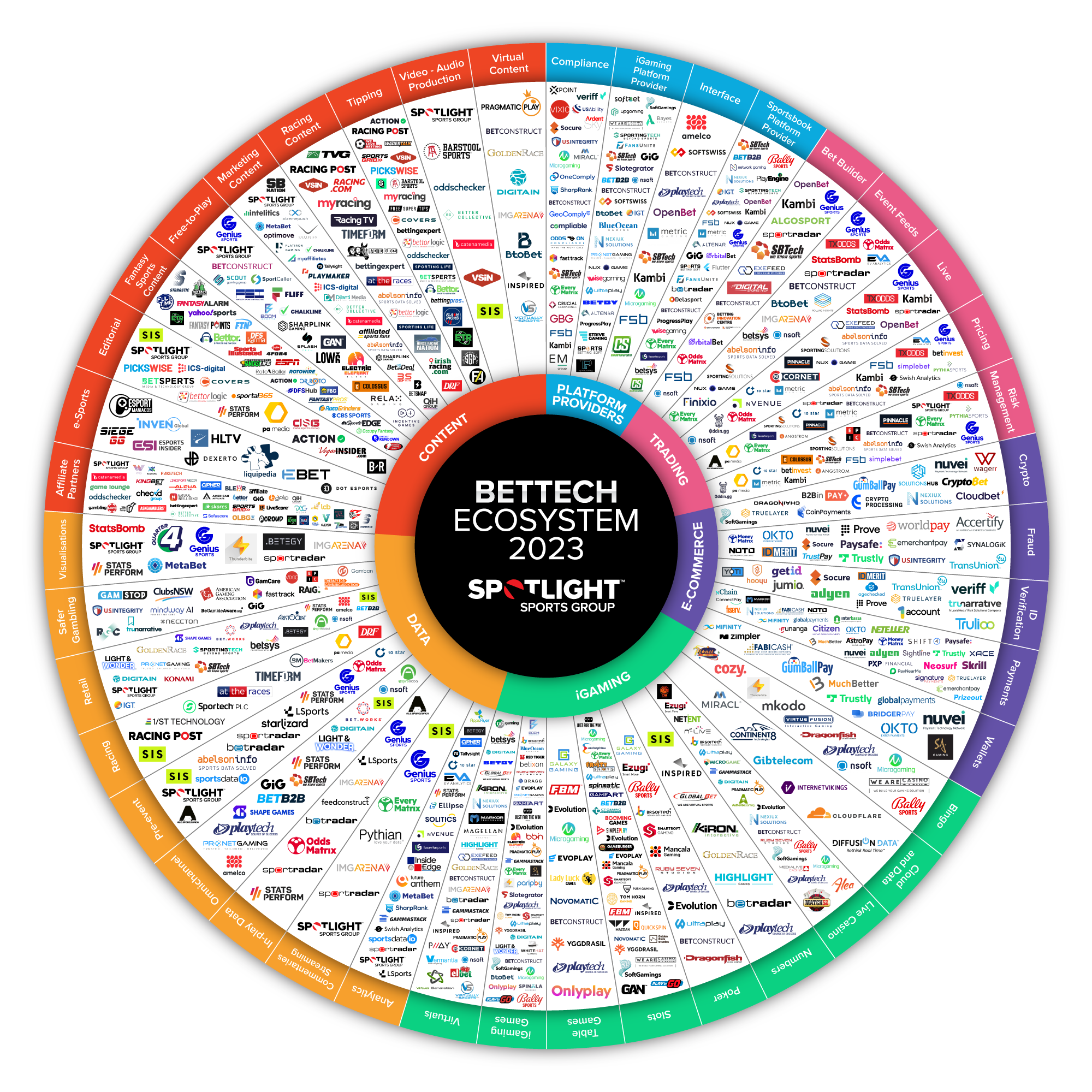

Welcome to the third edition of the BetTech Ecosystem report produced by Spotlight Sports Group. This report helps provide the sports betting and iGaming industries with a deeper understanding of regulated betting markets globally. To do this, we create a single visual that showcases all of the supplier companies that work in specific areas of these industries and have relationships with iGaming and sportsbook operators or bettors. Additionally, we take a deeper look at hot topics within the industry and provide insight as to where we think the industry could be heading in the next 12 months. While the list of companies included in the BetTech Ecosystem visual is both in-depth and based on research from dozens of industry experts at Spotlight Sports Group and independent experts, it is by no means a definitive list. The ultimate goal is to showcase how many companies are essential participants in the industry and to help those within the industry better understand it. The 2023 BetTech Ecosystem visual includes six main sections, 42 subsections and 375 companies. These companies range from start-ups to global enterprises with a presence in one legal market or every legal market. As we reviewed the 2022 visual, we had to remove 24 of 321 companies due to mergers and acquisitions or ceasing of operations. In this review, we also added the Cloud and Data providers subsection to the iGaming section and 80 new companies overall. We hope you enjoy reading the third edition of the BetTech Ecosystem report and please share your feedback or any suggested additions with our BetTech team to help us improve this report for 2024: bettech@spotlightsportsgroup.com

FOREWORD

DISCLAIMER: The information provided within the report is not definitive and is the opinion of Spotlight Sports Group and not intended to provide legal, accounting, compliance, investment or policy advice, nor should they be used as a forecast.

BETTECH ECOSYSTEM BY SEGMENT

FOREWORD INTRODUCTION North America, can everyone be a winner? Maturing regulations in the UK MARKET SNAPSHOTS North America: The fight for market share and profitability US Canada UK and Europe: Markets with different regulations but a common theme of stricter rules coming UK Ireland Spain Germany Netherlands SPORTSBOOK SNAPSHOT Operators and Market Share NFL THE ECOSYSTEM Deep dive Data and Content: The way to engage sports bettors no matter the market Data Content Platform providers Trading E-commerce iGaming Ecosystem Wheel COMPANIES WITHIN THE ECOSYSTEM ABOUT

This year, for our industry report, we have taken a deep dive into the current state of the North American market and the combined markets of the UK and the rest of Europe. These two geographies are in contrasting stages of maturity and require differing services from the wider betting ecosystem. Here are the key takeaways from this year’s report.

INTRODUCTION

North America, can everyone be a winner? In North America, new jurisdictions have been legalising sports betting every few months and sportsbooks are making determinations as to how they will attempt to gain market share and move toward profitability. This is, of course, much easier said than done. Out of the pack FanDuel, DraftKings and BetMGM have emerged at the front of the grid and now control a combined 85% of the American sports betting market over a recent rolling 3-month period. This is according to a November 2022 report from Eilers and Krejcik Gaming (EKG) and is a more than significant majority that is already proving hard for other players to challenge. This competition enhances the importance of sports betting affiliates that can drive valuable sports bettors directly to sportsbooks and help to optimise their returns. Maturing regulations in the UK: In the UK and other countries in Europe, legal sports betting has long been established and a host of governments throughout the whole of Europe are tightening their regulations. In the UK, the long-awaited gambling white paper has finally been published following continuous speculation as to what the final copy would look like. All the while, the implementation of affordability checks by some operators has begun and is strongly opposed by bettors. A Racing Post study of more than 10,000 horseracing bettors showed that 97% of bettors don’t think any agency should determine how much they are allowed to bet. A report by Ernst & Young that reviewed gambling data covering the period between July 2021 and June 2022 found that online betting revenue was down by 15% compared to the same time period in the previous year. This was largely attributed to “the gradual implementation of affordability checks over the past 12 months, plus the inflation-driven squeeze on household incomes.”

NORTH AMERICA: THE FIGHT FOR MARKET SHARE AND PROFITABILITY US: The slowing of newly regulated markets The rush of states to legalise online sports betting in America has slowed in 2023. In 2022, New York, Arkansas, Kansas, Louisiana and Maryland joined other states in legalising online sports betting, which led to a bidding war from sportsbooks looking to gain market share state by state. In 2023, though, only Ohio and Massachusetts have launched their online sports betting markets to this point. There are few other states expected to join them within the next 12 months. The states expected to legalise sports betting next are Kentucky, Maine, Missouri and Vermont. However, with fewer states expected to legalise sports betting imminently it is likely that sportsbooks will begin to turn their focus towards retention sooner rather than later and affiliates will be doing everything they can to drive new bettors who are engaged in content and are valuable for the long-term to their operator partners while acquisition is still a main focus. If the hypothesis is correct that North America will follow similar market forces to Europe then actionable betting content will become king. Companies in the betting ecosystem with the unique combination of proprietary data, content, and technology to continuously engage sports bettors and innovate quickly will thrive and become the trusted partner of sportsbooks.

MARKET SNAPSHOT

US States with Legalised Sports Betting - Handle By Month 2022-23

Source: Legal Sports Report

POPULATION OF CITIZENS AGED 21+ IN THE US

Online sports betting is legal

Online sports betting is not legal

*Population is based on state populations from June of 2020

CANADA: One year of sports betting in Ontario On 4th April 2022, Ontario became the first Province in Canada to legalise single-event wagering in the country and a report from iGaming Ontario (IGO) shows that residents are starting to take to sports betting. IGO reported that the market’s revenue increased by more than 70% from Q2 of 2022 to Q3 of the same year and that the number of active player accounts grew 45% to 910,000 over the same period. Similarly, in iGaming, Ontario has seen consistent growth. IGO reports that the Ontario Province already has the fifth largest iGaming market in North America with an estimated C$35.6bn in total wagers placed in the past year. While growth in gambling within the Province is apparent, regulations established by Canada’s Alcohol and Gaming Commission (AGCO) have seemingly limited the potential within the market. In Ontario, while sportsbook bonus offers are allowed, they can be promoted only on the platforms of operators. Sportsbooks and iGaming operators have also been made responsible for ensuring that any third-party market affiliates that advertise on their behalf meet the same advertising standards as the operators themselves. The decision by the AGCO to not directly regulate affiliate companies and allow for the promotion of sportsbook offers has limited the ability of sportsbooks and affiliates that were not a part of the previously functioning grey markets to compete with the already established brands.

Source: lpsos survey conducted in March 2023

MOST POPULAR SPORTS TO BET ON IN ONTARIO

UK AND EUROPE: MARKETS WITH DIFFERENT REGULATIONS BUT A COMMON THEME OF STRICTER REGULATIONS COMING In Europe, many countries that have legal sports betting and/or iGaming regulations in place have begun to introduce stricter rules and regulations for operators and affiliates in the past year-plus. Some of the countries have established markets while others have only recently legalised gaming, however, the common theme is to protect potential bettors from specific types of marketing. UNITED KINGDOM In the UK, the seemingly never-ending wait for the government's white paper finally came to a close on Thursday, April 27, 2023. Among other points, the white paper states that punters will be subject to two forms of "frictionless" financial risk checks. Firstly, there will be increased background checks at moderate levels of spend, to check for financial vulnerability indicators, which is proposed to take place at £125 net loss within a month or £500 within a year. Secondly, it has been proposed that at higher levels of spend which may indicate harmful binge gambling or sustained unaffordable losses there should be a more detailed consideration of a customer’s financial position, with thresholds of £1,000 net loss within 24 hours or £2,000 within 90 days. Reacting to the white paper, the Racing Post’s Chris Cook said “While the white paper says these checks should be "frictionless", it is clear the precise mechanics required to meet this ambition have yet to be fully set down, raising the prospect that higher-staking bettors will continue to receive demands for sensitive financial documents.”

UK and Ireland breakdown of combined ‘Yes’ responses UK 17% Ireland 12.7%

Have you been asked to carry out an affordability check by a bookmaker?

No

Yes, by one bookmaker

Yes, by multiple bookmakers

Source: Racing Post - The Big Punting Survey - February 2023

In anticipation of certain regulations being implemented in the near future, most operators have already implemented affordability checks at varying levels among their audience with increased checks on payslips and bank accounts. According to a recent survey by the Racing Post that surveyed more than 10,000 bettors from the UK and Ireland, nearly 17% of respondents were asked to carry out an affordability check by a sportsbook. Of the 17%, more than half (55%) refused to comply with the check. Additionally, the survey asked participants who have yet to be asked to do an affordability check what they would do should it happen in the future and 66% said they would refuse. Greater restrictions are coming to the UK gambling market in the near future. Depending on the effects of the gambling white paper, strategies of operators and affiliates may need to be adjusted.

IRELAND Until November 2022, sports betting, retail gambling and iGaming were regulated in different ways by the Irish government. Each area of gambling had somewhat different regulations but the recently passed gambling regulation bill created a regulatory body for all forms of gaming in Ireland. The new regulatory body, Gambling Regulatory Authority of Ireland (GRAI) will consist of seven members and will oversee all gaming matters in the country besides the lottery. The implementation of this legislation immediately banned gambling advertisements on television from 5:00pm to 9:30pm every day, as well as the application of a complete ban on social media advertising that is targeted at individuals. This advertising restriction prohibits the offer of hospitality or VIP treatment, free bets or favourable treatment/better odds to entice a person to gamble is outlawed. Prospective bettors will need to ‘opt in’ to receive gambling ads online. Ireland’s regulatory body also created the Social Impact Fund to support research and problem gambling programs. To further protect problem gamblers, the GRAI will oversee a national exclusion register. If a problem gambler ‘opts out’, every licensed gambling company must ensure that gambler does not have access to that service. These new regulations were all implemented before the members of the regulatory body officially convened for the first time. SPAIN In Spain, the gross gaming revenues (GGR) for sports betting in Q4 of 2022 saw an increase of 223% when compared to the same quarter in 2021, according to the gambling regulatory body in Spain, the Directorate General for the Regulation of Gambling (DGOJ).

When looking at the full-year online sports betting revenue in Spain for 2022, the DGOJ reported it increased by 18% year on year. This growth occurred after the DGOJ implemented regulations that banned TV and radio advertisements outside of 1am-5am, prohibited gambling sponsorship and restricted sportsbook bonuses in 2021. More recently, the senate in Spain passed a new gambling law in October 2022 that restricts sportsbooks from creating advertisements appearing beneficial to social status, physical health, economic stability or mental health. The bill also created the Global Betting Market Research Service to process personal data to combat fraud.

SPORTS BETTING GROSS GAMING REVENUE IN SPAIN

Source: Directorate General for the Regulation of Gambling (DGOJ)

GERMANY For years Germany’s gambling regulations have been fractured across sports betting, iGaming and retail gambling with each federal state maintaining their own regulations. This structure was similar to what we see in the US, but it was much more convoluted. However, in late 2022, the Gemeinsamen Glücksspielbehörde der Länder (GGL) unified every area of gambling regulations into one body. The GGL took over regulatory control of Germany’s gambling sector due to The InterState Treaty from July of 2021 and it has already received criticism from stakeholders due to certain regulations. Namely, casino operators have seen strict restrictions, including maximum monthly deposits and limited bet sizes and taxes being based on turnover rather than profits. Other advertising restrictions in Germany include the ban of active athletes and officials participating in ad campaigns. The use of influencers in the context of sponsoring or advertising is also prohibited. Even with early criticisms, most stakeholders have noted that the GGL is a step in the right direction for the industry.

NETHERLANDS The Netherlands operates one of the newest online gambling markets in all of Europe as the country only officially legalised sports betting and iGaming in late 2021 after years of delays. Even as a relatively new market, online gambling has seen swift action taken by regulators to limit sportsbook advertising. To start 2023, the Netherlands implemented a ban on ‘untargeted’ gambling ads. This ban prohibits operators from advertising on television, radio or in public spaces. Starting in 2024, sponsorship of television programmes and events will be prohibited and in 2025 sponsorship of sports shirts and venues by operators will be banned. Other forms of direct and online marketing are permitted but further restrictions are expected as the regulatory body looks to protect vulnerable groups and potential problem gamblers.

OPERATORS AND MARKET SHARE While fewer states in the US are in line to legalise online sports betting, there is still fierce competition among operators to obtain a worthwhile portion of market share of sports bettors. FanDuel, DraftKings and BetMGM have obtained the largest pieces of the pie to this point. On the other end of the spectrum, bet365 and Fanatics Sportsbook have begun their push into North America more recently, with Fanatics planning to launch later in 2023. In 2021, bet365 was not approved by the New York Gaming Commission and is currently only active in New Jersey, Virginia, Colorado and Ohio. Despite its popularity in Europe, bet365 has taken a slower approach in the States, limiting the amount of markets in which it operates. In reviewing the current landscape of operators in the US, industry newsletter, Earnings+More noted: “FanDuel and DraftKings continued their dominance of the Ohio market in February with a combined 77% of GGR but bet365 was a notable entry into the top four with 5.5% GGR share and 5% of handle. Analysts at EKG suggested there were indications within the February data that bet365 made a post-Super Bowl marketing push. “We continue to believe bet365 will treat Ohio as a field trial of sorts for future US markets (i.e. Texas) in which it could conceivably leverage first-mover advantage,” they add. Notable less-than-one-percenters include Betway, betr and PointsBet while Tipico achieved just over 1%.”

SPORTSBOOK SNAPSHOT

While every sportsbook has a different strategy, to this point, only FanDuel has achieved profitability, turning a profit in Q2 of 2022 and expects to be profitable for the full year in 2023.

OHIO FEBRUARY 2023 GGR MARKET SHARES

Source: Earnings+More newsletter - April 3, 2023

sports on which mobile gamblers 18+ placed bets in last month

Data collected October 2022. Source: CRG Global for Variety Intelligence Platform. Base: Mobile Sports Gamblers 18+ (N=815)

NFL: Forever Important Since the repeal of PASPA, one thing that has remained crystal clear is the popularity of the NFL as a betting product. In October 2022, when the four major pro sports leagues in the US were in action, more than 80% of bettors placed a bet on the NFL, a report by CRG Global discovered. The report identified that the next closest competitor for betting popularity was the NBA, with just over half of bettors (54%) placing bets on NBA games. For this year’s Super Bowl, GeoComply saw 100 million sports betting geolocation transactions, which was an increase of 25% year-on-year. In and around State Farm Stadium in Glendale, Arizona, the host site of the game, more than 100,000 betting transactions were verified on game day. At one point during the game, FanDuel reported that their platform was receiving 50,000 bets per minute and averaged two million active users throughout the game. At the moment, it is seemingly a foregone conclusion that large numbers of US bettors will wager on the NFL and other key sporting moments throughout the year. What is truly in question is which sportsbook they will bet with.

DEEP DIVE NFL is proven to be the most valuable sport in North America and soccer in Europe, but how do sportsbooks translate this passionate following into active sports bettors? Sports betting regulations across North America and the whole of Europe will always differ from each other as the countries have different cultures and will mature at a different pace. In addition to this, bettors in each country have different reasons for betting and spending habits. However, as long as gambling is regulated in these markets, sportsbooks and affiliates will need to supply potential bettors with the best user experience possible. This is why the ecosystem of companies that are established in these markets is continuously changing and competition remains ever-present. Even in an established market like the UK, sportsbooks rely on their affiliate networks to drive valuable bettors to their platforms and this will remain true in North America as well. While new jurisdictions are opening slower there is still room for other operators to thrive. The ‘best user experience’ will vary from market to market similarly to that of which sports bettors are interested in. However, data and content is essential no matter what the best experience will be.

THE ECOSYSTEM

UK vs USA

Source: Receptional - Sport Bettors Buying Habits 2023 - UK Edition

SPENDING HABITS

Affiliate partnerships are a proven model for growth as they provide sportsbooks with brand visibility to sports betting-interested audiences and a way to display their odds in an environment outside of their own platform. In America, sports is deeply embedded in the culture with countless newspapers, blogs and media platforms completely dedicated to sports coverage. This leads to intense competition among affiliate companies and traditional media platforms, similar to that of their sportsbook counterparts. These platforms have grown immense audiences that are coveted by sportsbooks and are main drivers of first-time bettors in new markets, as they help publicise special offers and drive bettors directly to the operators. The advantage that affiliate platforms have over sportsbooks is their ability to provide unbiased third party information. Responsible affiliate companies also protect their audience from offshore sportsbooks. These affiliate companies direct their audience to regulated sportsbooks because of the important safer gambling rules they employ. The actionable betting content is not written by the sportsbooks, which in turn helps make potential bettors more informed in their betting decisions and can grow their trust of affiliate platforms. The trust and loyalty of bettors is what sportsbooks and affiliates are looking for and it is a highly competitive industry in all markets.

Source: Spotlight Sports Group

MODEL FOR GROWTH

For instance, Spotlight Sports Group has seen 14% more bets placed by bettors exposed to Superfeed content on sportsbook platforms compared to bettors that were not. The best content is not solely created based on beliefs of a person’s opinion, it is supported by historical and live data that helps shape the content into something actionable. This includes key reasons for a certain bet to be placed or not placed. As regulators impose strict advertising restrictions to protect potential problem gamblers, the best way forward is to provide bettors with unbiased and actionable content to ensure the decisions they are making are as educated as possible.

In separate surveys administered by Receptional, betting habits of UK bettors and US bettors were researched in December of 2022. For UK bettors, the average 18-50 year old will spend at least 30 minutes researching a bet, with some spending upwards of two hours doing research. Across the pond, in the US, bettors between 21 and 50 years old spent a similar amount of time researching bets, with the majority of people spending 30 minutes to an hour doing research. The research time taken by the most valuable age group of bettors in these markets shows their interest in expert opinions. The more actionable content provided by affiliate companies and embedded onto sportsbook platforms as independent expert content will increase user engagement.

DATA AND CONTENT: The way to engage sports bettors no matter the market

Source: Receptional - Sport Bettors Buying Habits 2023 - US Edition

RESEARCH TIME BY AGE

DATA Users thrive off data and data is an essential partner to content in the ecosystem. The most effective sports betting content is powered by or coupled with key data insights. For instance, high volumes of content being published is only possible with the help of historical and live data powering content engines. In-play betting prompts, pre-play bet suggestions and long-form betting editorials are all best when data is used to create actionable insights. Data is also essential on the business side to help operators and affiliates understand the trends of the industry and the interest of their audiences. The increased importance of business analytics units and analytical insights is the main reason why analytics saw the largest increase of any subsection in this part of the ecosystem. CONTENT Content is the driving force of the BetTech Ecosystem. Actionable sports betting content and insights drive users into, and through, the betting funnel and there are a variety of ways to do this. Written content is the most common type of tipping, but short-form video and audio content has become an increasingly important part of the content ecosystem in recent years. The desire for expert content from bettors is why more sports broadcast networks provide betting content consistently as part of their daily scheduling in today’s media landscape. The content section is the largest part of the BetTech Ecosystem due to the variety of ways content can be produced. However, the section saw the smallest increase in this year’s report due to the difficult task of cultivating and engaging with a large sports betting audience..

Source: Spotlight Sports Group’s data-infused smart content module

PLATFORM PROVIDERS In this year’s BetTech Ecosystem visual, the platform provider section saw most of the industry leaders return, but across the four subsections, 11 new companies were added. Platform providers and trading partners are the obvious areas with which sportsbooks generally work to create a user friendly platform, and supply bettors with everything they need to place a bet. There has been a trend to owning the platform given the strategic benefits and the flexibility it affords. However, in a world with increasing cost pressures, outsourcing large elements of the platform is becoming increasingly popular again. DraftKings, Caesars and bet365 are among the select few operators that use their own technology to power their platforms. Conversely, the interface of the soon-to-launch Fanatics Sportsbook is developed by Amelco, showcasing a new entrant to the market utilising a supplier as they scale their operations. There are a number of ways to build a successful sportsbook platform and operators decide to do this differently across the board, which is why there is a wide range of successful suppliers in this part of the ecosystem.

TRADING Trading is beyond essential for any sportsbook, in-person and online and it is evident that a one-size-fits-all solution is out of the question. Operators need to provide prospective bettors with a wide range of betting options whether they be pre-match, in-play or bet builders. Event feeds and pricing often allows operators to stand out among their competitors and supplier companies are consistently aiming to move faster and improve their technology to stand out in this now crowded market. Sportradar, Every Matrix, TXODDS and Pinnacle are among the biggest players in this part of the industry and supply operators with essentially everything they need to provide betting lines to their audience. Suppliers that provide elite trading systems allow sportsbooks to create the best betting lines for an infinite number of bet types and provide bettors with a seemingly endless supply of betting options across a wide array of sporting events.

iGAMING iGaming however, is a unique part of the ecosystem. In some established markets iGaming is the dominant revenue generator in the gambling space while in others it hasn’t taken that step yet. An interesting competition to watch as iGaming grows in the US is which operator controls the most GGR market share. In late 2022, EKG reported that FanDuel, DraftKings and BetMGM hold a combined GGR market share of 69%. This is similar to what we have seen on the sports betting side with these three operators holding the majority of the market share, however, when it comes to iGaming the market share leader changes. BetMGM holds 30%, DraftKings holds 23% and FanDuel has 16% while every other operator has less than 10% in market share. To provide users with the best iGaming experience, operators rely heavily on suppliers to create table games, live casino, bingo, slots and other popular forms of online casino games.

E-COMMERCE E-commerce is essential to allow sportsbooks to take bets and for bettors to receive payouts, especially in this digital age where more people are looking for ways to pay through less traditional ways. Companies that specialise in this area are key to the next generation of bettors.

The crypto subsection was added to the ecosystem last year as blockchain payments became more mainstream among the younger generation. It is now slowly becoming an essential payment option for iGaming gamblers and sports bettors and some established payment providers have added this to their services. In the e-commerce section, fraud and ID verification services are maybe the most important subsections. While gambling has been around for decades, online gambling is still a relatively new concept, so providing sportsbooks and bettors with security is an unparalleled necessity in the ecosystem.

As sports betting has become established in North America, more traditional payment providers have begun to provide operators with their payment solutions, which they are well versed in. This is why the payments subsections is the largest subsection in this part of the BetTech Ecosystem visual, and also saw the largest increase in companies listed.

PLATFORM PROVIDERS

TRADING

E-COMMERCE

DATA

iGAMING

CONTENT

Hover on the above section to view

1/ST TECHNOLOGY 10 Star 1account 1x2 Network 4for4 7BitPartners Abelson Info Accertify Acroud Action Network Adyen Affiliated Sports Fans AgeChecked Alea Algosport ALPHA Affiliates Alt Sports Data Altenar Amelco American Affiliate Co. American Gaming Association Angstrom Sports AppsFlyer ArdentSky Aristocrat Technologies askgamblers Aspire Global AstroPay At The Races B2BinPay Bally's Interactive Barstool Sports Bayes Esports BBIN BeGambleAware Bet Share Bet.Works BetanDeal Group BetB2B Betby BetConstruct Betegy betinvest Betixon BetMakers Technology Group Betradar BetSnap Betsperts media & technology group Betsys Better Collective Betting Expert Betting Innovation Centre BettingPros Bettor Sports Network Bettor Vision Bettorlogic Bleacher Report Bleacher Report Betting Blexr BlueOcean Gaming Bojoko BonusFinder Boom Entertainment booming games BR Softech Bragg Gaming BridgerPay BTOBet Catena Media CBS Sports Chalkline Sports Champion Sports Checkd Group Cipher Sports Technology Group Citizen Clever Advertising Group Cloudbet Cloudfare Clubs NSW CoinPayments Colossus Bets Compliable ConnectPay Continent 8 Technologies Cor Net Covers Crucial Compliance Cryptobet Cryptoprocessing by CoinsPaid CT Gaming Daily Racing Form Data Sports Group Delasport Dexerto DFS Hub DFSKarma DiffusionData Digitain Digital sports tech Dilanti Media Dot Esports DR Roto DragonChain Dragonfish EBet Elbet Electric Elephant Games Electronic Verification Systems Ellipse Data EM Group emerchantpay Endorphina Epic Risk Management ESPN Esportmaniacos Esports Insider Establish The Run EV Analytics Everi Every Matrix Evolution Gaming Group Evoplay Exefeed Ezugi FABICash FansUnite Fantasy Alarm Fantasy Points Fantasy Pros Fantasy Rundown Fantasy Sports Interactive Fast Track FBM Feedconstruct Finixio Fiserv FlashPicks Flatiron Gaming Fliff Social Sportsbook Flutter Entertainment Plc Footballguys footyaccumulators Free Super Tips Fruity Slots FSB Technology FTN Network Full Time Fantasy Funanga Future Anthem Galaxy Gaming Gamban Gambling Therapy GamCare Game Art Game Lounge Gameburger Studios Gaming Innovation Group Gammastack GAMSTOP GAN GBG Genius Sports GeoComply getid Gibtelecom Global Bet Global Payments Gaming Solutions Golden Race Golden Rock Studios GumballPay Highlight Games HLTV.org hooyu Horse Racing Nation ICS-digital ID Merit IGT PlaySports IMG Arena Incentive Games Inside Edge Inspired Entertainment Intelitics Interkassa Internet Vikings Inven Global irishracing.com Jumio Just For The Win Kafe Rocks Kambi KingBet Media Kiron Interactive Konami Gaming Lacerta Sports Lady Luck games Latest Casino Bonuses Light & Wonder Liquipedia Livescore Livesport Media Low6 LSports Magellan Robotech Mancala gaming Markor Technologies Matthew Berry's Fantasy Life Medialive Casino Metabet Metric Gaming Microgame Microgaming MiFinity Mindway AI MIRACL MoneyMatrix mraffiliate MuchBetter MyAffiliates myracing Natural Intelligence NBC Sports Edge nChain neccton Neosurf Neteller Network Gaming Nexiux Solutions NOTO Novomatic NSoft Nuvei Nux Game nVenue Occupy Fantasy Oddin.gg Odds On Compliance oddschecker Oddsmatrix OKTO OLBG OneComply Onlyplay OpenBet Optimove Orbital Bet PA Media Pariplay PayNearMe Paysafe Pickswise Pinnacle Play'n GO PlayEngine Playmaker Playtech Pllay Labs Pragmatic play Prizeout ProgressPlay Pronet Gaming Prove Push Gaming PXP Financial Pythia Sports Pythian QiH Group Quarter4 Quickspin Racing Dudes Racing Post Racing TV Racing.com RAIG Raketech RealTime Fantasy Sports Relax Gaming Responsible Gambling Council Rolling Insights Rotoballer Rotogrinders RotoWire Ruby Seven Studios SA Gaming SBNation SBTech Scout Gaming Group Shape Games SharpLink SharpRank Shift4 SiegeGG Sightline Payments Signature Payments Simplebet SimplePlay SIS Skores Skrill slotegrator Smartsoft gaming Socure SofaScore Soft2Bet SoftGamings SoftSwiss Solitics SolutionsHub Spinmatic Entertainment Spinola Gaming Splash Tech sportal365 SportCaller Sportech PLC Sporting Life Sporting Solutions Sportingtech Sportradar Sports Betting Soft Sports Gambling Podcast Network Sports Illustrated SportsDataIO SportsGrid Spotlight Sports Group Starlizard Stats Perform StatsBomb Stokastic Strive Gaming Swish Analytics Symplify SYNALOGiK TAG Media Tallysight The Action Network The Fantasy Footballers Thunderbite Timeform Tom Horn Gaming Traffic Lab TransUnion True Layer Trulioo trunarrative Trust Pay Trustly TVG Network TXODDS UltraPlay Upgaming US Integrity USAbility VegasInsider Veriff Vermantia Virtual Generation Virtually Sports Vita Media Group Vixio VSiN Wagerr WagerTalk Wazdan Ltd We Are Casino Web International Services welovebetting White Hat Gaming WiseGaming Worldpay Xace xlmedia plc Xpoint Xtremepush Yahoo Sports Yggdrasil Gaming Yoti Zimpler

Companies Included in the 2023 BetTech Ecosystem Visual

ABOUT SPOTLIGHT SPORTS GROUP

Spotlight Sports Group is a global media and technology company specialising in sports betting content and data. With more than 500 staff, the business operates multiple award-winning brands including Racing Post, the world’s largest horseracing affiliate, Pickswise, the #1 post PASPA affiliate in the US, MyRacing and Free Super Tips. Our other businesses in the group are ICS-digital and ICS-translate. Our global B2B division provides sports betting and fantasy sports content, including in-play, through the EGR award-winning Superfeed product. We also have media partnerships with leading global publishers, including Advance Local and The Arena Group. Spotlight Sports Group would like to thank all who contributed to compiling this report, if you would like to speak to the Spotlight Sports Group team that created this report please email the team or visit the BetTech website below.

Email bettech@spotlightsportsgroup.com

Visit the BetTech website

Download 2023 BetTech Ecosystem Visual