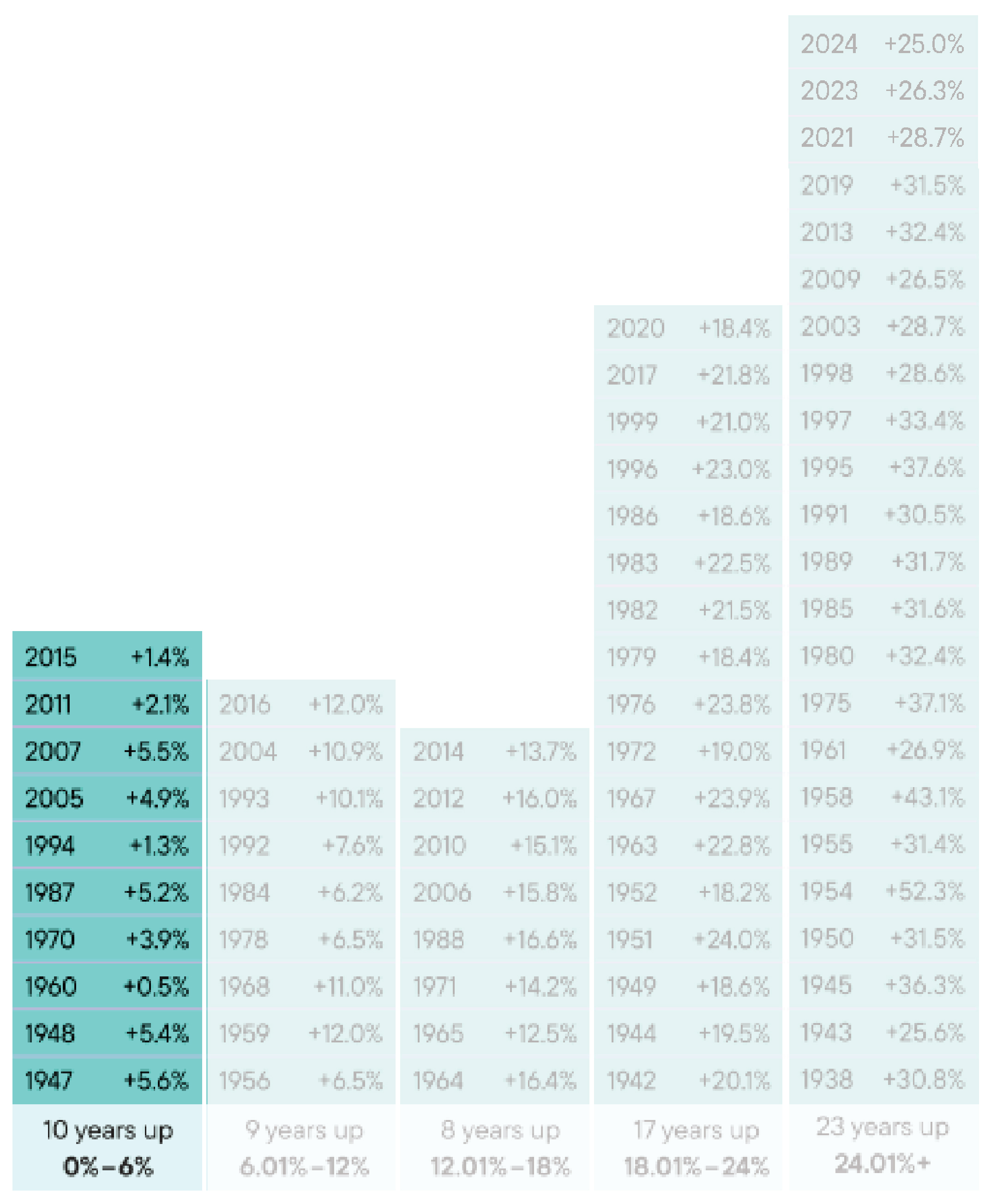

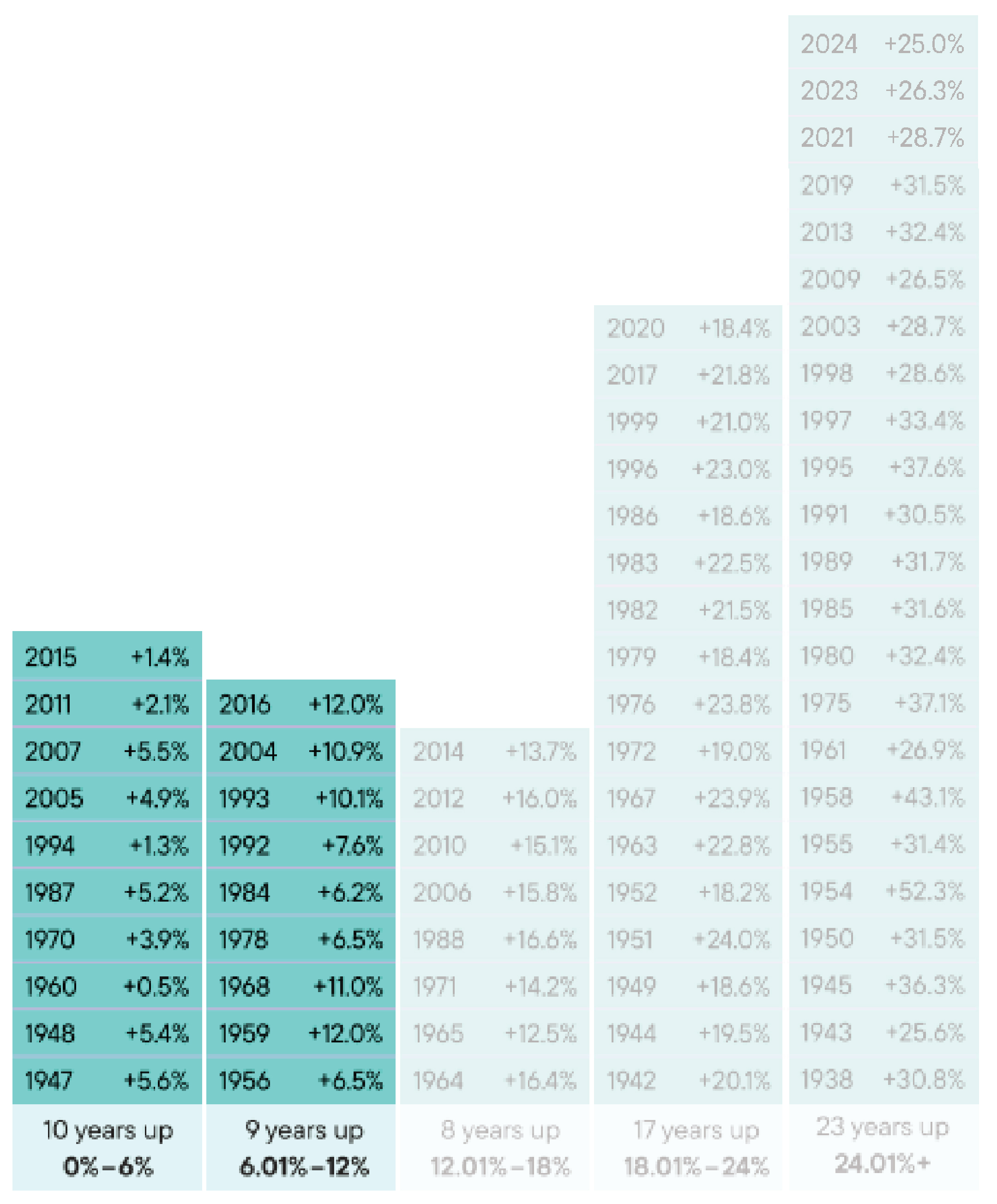

This chart highlights the 67 positive years of return of the S&P 500 .

®

This information is hypothetical and not representative of any particular product. Past performance does not guarantee future results.

Click below to learn more

Returns up to 6%

In 10 years or 15% of the time, returns ranged between 0-6%.

Returns up to 12%

In 19 years or 28% of time, returns ranged between 0-12%.

Returns up to 18%

In 27 years or 40% of the time, returns ranged between 0-18%.

Returns up to 24%

In 44 years or 66% of time, returns ranged between 0%-24%.

Returns 24%+

In 67 years or 100% of the time, returns

were positive.

A strategy such as an annuity could provide you various options to participate in opportunities for growth.

INVESTMENT AND INSURANCE PRODUCTS ARE:

• NOT FDIC INSURED • NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY

• NOT A DEPOSIT OR OTHER OBLIGATION OF, OR GUARANTEED BY, ANY BANK OR ITS AFFILIATES

• SUBJECT TO INVESTMENT RISKS, INCLUDING POSSIBLE LOSS OF THE PRINCIPAL AMOUNT INVESTED

Disclosures

Accessibility

Investors should carefully consider the features of the contract, index strategies, and the underlying portfolios’ investment objectives, policies, management, risks, charges and expenses. The initial summary prospectus and the index strategies prospectus for the contract, and the summary prospectus or prospectus for the underlying portfolios (collectively, the “prospectuses”) contain this and other important information and can be obtained from your financial professional. Please read them carefully before investing.

It is possible to lose money by investing in securities.

Annuities are issued by Pruco Life Insurance Company (in New York, by Pruco Life Insurance Company of New Jersey), Newark, NJ (main office) and distributed by Prudential Annuities Distributors, Inc., Shelton, CT. Both are Prudential Financial companies and each is solely responsible for its own financial condition and contractual obligations.

This material is being provided for informational or educational purposes only and does not take into account the investment objectives or financial situation of any client or prospective clients. The information is not intended as investment advice and is not a recommendation about managing or investing your retirement savings. If you would like information about your particular investment needs, please contact a financial professional.

Annuity contracts contain exclusions, limitations, reductions of benefits, and terms for keeping them in force. Your licensed financial professional can provide you with complete details.

You should carefully consider your financial needs before investing in annuity products and benefits.

The S&P 500® Index is a product of S&P Dow Jones Indices LLC (“SPDJI”), and has been licensed for use by Pruco Life Insurance Company. Standard & Poor’s®, S&P® and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”); Dow

Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by Pruco Life Insurance Company. Pruco Life Insurance Company’s Product(s) is not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P 500 Index.

All guarantees, including benefit payment obligations, index strategy crediting, or annuity payout rates, are backed by the issuing company's claims-paying ability and do not apply to the underlying variable investment options. The third-party broker-dealer/agency, or any of its affiliates, selling this annuity are not responsible for making those payments, and none makes any representations or guarantees about the issuer's claims-paying ability.

Buffers and floors are available on index-crediting strategies only. Variable investment options are available but do not offer protection levels.

This chart highlights the negative periods of the S&P 500 . In these 21 down years, strategies that offered a level of downside protection that could protect your account value in the case of a negative index return, such as a buffer within an annuity, could have helped limit your losses. That could have helped you feel more confident and stay the course.

®

This information is hypothetical and not representative of any particular product. Past performance does not guarantee future results.

Click below to learn more

In 2000

Your loss with a 5% buffer would

have been only 4.1% because you would have been protected from the initial 5% decline.

A 5% buffer would have protected you from a loss in 5 of those 21 down years, or 24% of the time.

Conversely, you would have seen a loss in the other 16 periods.

Conversely, you would have seen a loss in the other 16 periods.

5% Buffer

5% Buffer

In 1973

During this period, your loss with a

10% buffer would have been only 4.7% because you would have been protected from the initial 10% decline.

A 10% buffer would have protected you from any loss in 12 of those 21 down years, or 57% of the time.

Conversely, you would have seen a loss in the other 9 periods.

Conversely, you would have seen a loss in the other 9 periods.

10% Buffer

10% Buffer

In 2022

During this period, your loss with a

15% buffer would have been only 3.1% because you would have been protected from the initial 15% decline.

A 15% buffer would have protected from any loss in 16 of those 21 years, or 76% of the time.

Conversely, you would have seen a loss in the other 5 periods.

15% Buffer

15% Buffer

In 2002

During this period, your loss with a

20% buffer would have been only 2.1% because you would have been protected from the initial 20% decline.

A 20% buffer would have protected from any loss

in 17 of those 21 years, or 81% of the time.

Conversely, you would have seen a loss in the other 4 periods.

20% Buffer

20% Buffer

In 2008

During this period, your loss with a

30% buffer would have been only 7% because you would have been protected from the initial 30% decline.

A 30% buffer would have protected from any loss

in 19 of the 21 years, or 90% of the time.

Conversely, you would have seen a loss in the other 2 periods.

30% Buffer

30% Buffer

A 100% buffer would have protected from any loss in all of these years or 100% of the time.

Conversely, you may not have seen as much growth potential in up markets.

100% Buffer

100% Buffer

If you have a hard time staying the course in your investment approach, strategies that offer a level of downside protection might be right for you.

Emotions and

the market

Down markets

Up markets

Learn from history

Next steps

Reduce motion

Emotions and the market

Learning from the history of the S&P 500

®

®

Reflecting on the past 88 years (1937-2024) of the S&P 500 , market returns have fluctuated quite a bit. While market ups and downs can be overwhelming, they are a normal part of the investment journey. Historically, investors who took a longer term approach typically saw better results.

While there are many factors that can affect your returns—including volatility, interest rate changes, or inflation—the biggest factor is making decisions based on emotion.

Did you know?

Investors making decisions during periods of market stress saw average growth of only 3.4%—compared to the growth of the S&P 500 , which grew 9.7% during the same period.

®

Source: ClearBridge Investments; Anatomy of a recession December 31, 2024.

Download

Paper

Let’s explore how you can find a balance of protection and growth in your portfolio to help achieve your goals.