DECARBONISATION

Gap between pledges and progress

For the world to achieve carbon neutrality, asset managers have

a huge role to play, working hand in hand with governments on policy, investing in climate change solutions and decarbonising their portfolios

a huge role to play, working hand in hand with governments on policy, investing in climate change solutions and decarbonising their portfolios

As the Northern Hemisphere faces another unprecedented heatwave, the importance of climate change mitigation has never been more apparent. Decarbonisation – the process of reducing greenhouse gas emissions

– is arguably the most important aspect of this process.

Specific targets for this were first introduced at a meeting in Paris in 2015 called COP21, where the leaders of 195 nations signed an agreement to limit global warming to a maximum of 2C above pre-industrial levels, and preferably 1.5C. This is called the Paris Agreement.

To achieve this ambitious target, the world must reach carbon neutrality, bringing CO2 emissions to net zero.

Net zero is the balance between the greenhouse gases produced by human activity and the amount removed from the atmosphere, with the aim to have zero impact on the climate.

This is possible to achieve through a two-pronged approach that removes existing carbon dioxide from the atmosphere, while also reducing new emissions.

After signing the Paris Agreement, 140 countries across the globe have set net-zero targets, and private finance has a major role to play in reaching these goals.

– is arguably the most important aspect of this process.

Specific targets for this were first introduced at a meeting in Paris in 2015 called COP21, where the leaders of 195 nations signed an agreement to limit global warming to a maximum of 2C above pre-industrial levels, and preferably 1.5C. This is called the Paris Agreement.

To achieve this ambitious target, the world must reach carbon neutrality, bringing CO2 emissions to net zero.

Net zero is the balance between the greenhouse gases produced by human activity and the amount removed from the atmosphere, with the aim to have zero impact on the climate.

This is possible to achieve through a two-pronged approach that removes existing carbon dioxide from the atmosphere, while also reducing new emissions.

After signing the Paris Agreement, 140 countries across the globe have set net-zero targets, and private finance has a major role to play in reaching these goals.

The role of private finance

ESG Clarity’s Net Zero Database, which looks under the bonnet of 83 asset managers’ net-zero commitments, reveals that many industry players are making commitments to decarbonise their portfolios. They can do so in a number of ways, including absolute emissions reduction, emissions intensity reduction, temperature targets and net-zero alignment for assets or emissions.

The methodology for this research uses data from the Net Zero Asset Managers’ initiative (NZAM), launched in 2020 with the aim to “galvanise the asset management industry to commit to a goal of net-zero emissions”. NZAM now counts 315 firms with a total of $59trn (£46trn) in assets under management as signatories, including Aviva Investors, BlackRock and Fidelity International.

The methodology for this research uses data from the Net Zero Asset Managers’ initiative (NZAM), launched in 2020 with the aim to “galvanise the asset management industry to commit to a goal of net-zero emissions”. NZAM now counts 315 firms with a total of $59trn (£46trn) in assets under management as signatories, including Aviva Investors, BlackRock and Fidelity International.

Other private sector initiatives this year include an updated version of Climate Action 100+’s Net Zero Company Benchmark to encourage companies to work towards net-zero targets, as well as the release of net-zero standards for banks and guidance for private equity firms.

However, despite numerous pledges from asset managers and their investee companies, by April this year just 5% of FTSE 100 companies had published net-zero plans that are credible and detailed in terms of implementation.

And in May, research by Redington revealed only 17% of asset managers have a decarbonisation strategy in place, despite 59% making a net-zero commitment at a firm level.

Similarly, Net Zero Tracker reports that while the number of companies across the globe with net-zero targets has almost doubled in the past two and a half years, now standing at 909 of the world’s 2,000 largest businesses, just 4% of these commitments meet the UN Race to Zero campaign’s “starting criteria”.

However, despite numerous pledges from asset managers and their investee companies, by April this year just 5% of FTSE 100 companies had published net-zero plans that are credible and detailed in terms of implementation.

And in May, research by Redington revealed only 17% of asset managers have a decarbonisation strategy in place, despite 59% making a net-zero commitment at a firm level.

Similarly, Net Zero Tracker reports that while the number of companies across the globe with net-zero targets has almost doubled in the past two and a half years, now standing at 909 of the world’s 2,000 largest businesses, just 4% of these commitments meet the UN Race to Zero campaign’s “starting criteria”.

What are the challenges?

Meanwhile, investment managers themselves report various challenges

in meeting net-zero targets. These include a lack of consistency across data providers, which hinders the ability to calculate portfolio emissions, inconsistent climate modelling and uncertain policy context, and the fact economic growth is linked to higher emissions.

Asset managers interviewed by ESG Clarity highlight that net-zero targets may be riskier and more difficult to meet for emerging markets managers, while early-stage investors point to the lack of dedicated ESG standards.

Some in the industry also say policy is not moving fast enough to enable private finance to decarbonise.

“The government and the private sector must work hand in-hand, but at the moment the private sector’s ambition is running ahead while the government is lagging behind,” says Heather McKay, senior policy adviser at E3G.

“We need to deliver on transition plans and clear guidance through the UK

green taxonomy, but to mobilise investment at the scale required this must be backed up by the government ingraining net zero in its regulatory, policy and spending decisions.”

In October 2022, 30 leading UK companies managing £3trn assets, including Aviva, Jupiter and Royal London, wrote to the chancellor to advocate for “a clear ‘Net Zero Investment Plan’”. They called for an investment tracker to monitor financial flows into net zero, an assessment of sector-specific investment needs and the low-carbon investment gap, and the creation of a dedicated unit to track progress.

in meeting net-zero targets. These include a lack of consistency across data providers, which hinders the ability to calculate portfolio emissions, inconsistent climate modelling and uncertain policy context, and the fact economic growth is linked to higher emissions.

Asset managers interviewed by ESG Clarity highlight that net-zero targets may be riskier and more difficult to meet for emerging markets managers, while early-stage investors point to the lack of dedicated ESG standards.

Some in the industry also say policy is not moving fast enough to enable private finance to decarbonise.

“The government and the private sector must work hand in-hand, but at the moment the private sector’s ambition is running ahead while the government is lagging behind,” says Heather McKay, senior policy adviser at E3G.

“We need to deliver on transition plans and clear guidance through the UK

green taxonomy, but to mobilise investment at the scale required this must be backed up by the government ingraining net zero in its regulatory, policy and spending decisions.”

In October 2022, 30 leading UK companies managing £3trn assets, including Aviva, Jupiter and Royal London, wrote to the chancellor to advocate for “a clear ‘Net Zero Investment Plan’”. They called for an investment tracker to monitor financial flows into net zero, an assessment of sector-specific investment needs and the low-carbon investment gap, and the creation of a dedicated unit to track progress.

What’s next?

To remain on track for the Paris Agreement goals, asset managers will need to ramp up investments in climate solutions in the coming 12 months, according to Jasna Selih, senior stewardship specialist for Climate Action 100+, at the Principles for Responsible Investment.

She says: “Under the International Energy Agency’s Net Zero Emissions by

2050 scenario, renewables should exceed 60% of total electricity supply by 2030, which would require clean energy to rise to 4% of global GDP by 2030. While

we’ve seen significant growth in renewable energy generation over recent months, additional investment in clean energy is required for the world to meet the goals

of the Paris Agreement.

“Investment will also need to go to the deployment of new low-emissions technologies, which have yet to be scaled up but we know will be vital for the net-zero transition, and investments across the clean energy supply chain,” she adds.

She says: “Under the International Energy Agency’s Net Zero Emissions by

2050 scenario, renewables should exceed 60% of total electricity supply by 2030, which would require clean energy to rise to 4% of global GDP by 2030. While

we’ve seen significant growth in renewable energy generation over recent months, additional investment in clean energy is required for the world to meet the goals

of the Paris Agreement.

“Investment will also need to go to the deployment of new low-emissions technologies, which have yet to be scaled up but we know will be vital for the net-zero transition, and investments across the clean energy supply chain,” she adds.

Watch our decarbonisation explainer video below

Video Player is loading.

Loaded: 0%

0:00

Current Time 0:00

/

Duration 0:00

Remaining Time -0:00

1x

- Chapters

- descriptions off, selected

This is a modal window.

Beginning of dialog window. Escape will cancel and close the window.

End of dialog window.

MOST ASSET MANAGERS NOW HAVE A LONG-TERM NET-ZERO TARGET

Percentage of asset managers. Rollover bars to see categories

Source: Share Action, Point of no Returns 2023

5%

8%

6%

5%

6%

6%

hand in hand, but at

sector’s ambition is

running ahead while the

government is lagging’

government is lagging’

running ahead while the

government is lagging’

the moment the private

private sector must work

‘The government and the

Heather McKay,

senior policy adviser, E3G

senior policy adviser, E3G

NET-ZERO GHG BY 2050

(OR SOONER)

AMBITION

(OR SOONER)

AMBITION

75% of the world’s largest corporate GHG emitters have set a net zero by 2050 (or sooner) ambition that covers, at least, their Scope 1 and 2 GHG emissions. This is up from 69% in March 2022

Source: Climate Action 100+, Key Findings October 2022

51%

42%

25%

48%

31%

25%

28%

28%

24%

Yes

Partial

No

EQUALITY, DIVERSITY, INCLUSION

Stop, collaborate and listen

Although asset managers are

starting to incorporate diversity

and inclusion within their own organisations, the industry needs to work collectively with the businesses they invest in to effect real

starting to incorporate diversity

and inclusion within their own organisations, the industry needs to work collectively with the businesses they invest in to effect real

Equality, diversity and inclusion (EDI) are the hallmarks of a healthy environment, be it in the workspace or in the broader community. Multiple studies over the years have shown that a diverse workforce makes quicker and better decisions, and produces more revenue for the business.

According to a recent PwC survey, 85% of financial services CEOs polled saw benefits to their business performance from promoting diversity and inclusion, while a 2019 study by McKinsey & Co revealed that top-quartile businesses for racial and ethnic inclusion were 36% more profitable than those in the fourth quartile.

Yet while there has been some improvement, particularly when it comes to women’s representation on boards, progress has stalled over the past year amid a challenging economic climate.

According to a recent PwC survey, 85% of financial services CEOs polled saw benefits to their business performance from promoting diversity and inclusion, while a 2019 study by McKinsey & Co revealed that top-quartile businesses for racial and ethnic inclusion were 36% more profitable than those in the fourth quartile.

Yet while there has been some improvement, particularly when it comes to women’s representation on boards, progress has stalled over the past year amid a challenging economic climate.

How asset managers are looking at EDI internally

Within their own organisations, asset managers are starting to think about their policies and cultures, with media initiatives such as City Hive’s ACT Standard and Framework, which establishes an industry agreement on how to improve EDI internally, and MA Financial’s own Campaign for Better Governance, which encourages the industry to hold a mirror up to its own culture, leading the way.

CITY HIVE'S ACT FRAMEWORK

Unfortunately, progress is slow. Almost half (47%) of Europe’s asset and wealth managers are yet to achieve boards made up of 40% women, despite this being the target required by the European Women on Boards Directive, according to the latest EY European Financial Services Boardroom Monitor.

Racial discrimination also remains rife in the financial services sector. Research from financial services network Reboot found that 68% of ethnic minorities experienced discrimination in the workplace during the previous year, while 82% faced unwelcome comments on their backgrounds.

Justin Onuekwusi, co-founder of #TalkAboutBlack, says: “A lot of the momentum around EDI has dissipated, which is disappointing. There are a lot of initiatives trying to unkink the hosepipe and get people career ready, such as CV workshops and mentoring, but the support for them is not what it was three years ago.”

Racial discrimination also remains rife in the financial services sector. Research from financial services network Reboot found that 68% of ethnic minorities experienced discrimination in the workplace during the previous year, while 82% faced unwelcome comments on their backgrounds.

Justin Onuekwusi, co-founder of #TalkAboutBlack, says: “A lot of the momentum around EDI has dissipated, which is disappointing. There are a lot of initiatives trying to unkink the hosepipe and get people career ready, such as CV workshops and mentoring, but the support for them is not what it was three years ago.”

Justin Onuekwusi, co-founder, #TalkAboutBlack

dissipated, which

‘A lot of the momentum

is disappointing’

around EDI has

Watch our explainer video on EDI below

Video Player is loading.

Loaded: 0%

0:00

Current Time 0:00

/

Duration 0:00

Remaining Time -0:00

1x

- Chapters

- descriptions off, selected

This is a modal window.

Beginning of dialog window. Escape will cancel and close the window.

End of dialog window.

How asset managers are looking at EDI in their investments

Much more progress can be seen in attempts to improve EDI at the companies firms invest in. According to last year’s MSCI’s Women on Boards Progress Report, the number of women on boards globally has increased by 1.9% to 24.5% in 2022. The industry has played its part in this improvement with initiatives such as the 30% Club, which is dedicated to raising awareness of the lack of women in top management positions.

However, companies across the globe are still failing to close the gender pay gap. According to research from Equileap, just 28 companies worldwide have achieved this feat, amounting to less than 1%. Some 78% of the companies surveyed did not publish information on pay differences at all.

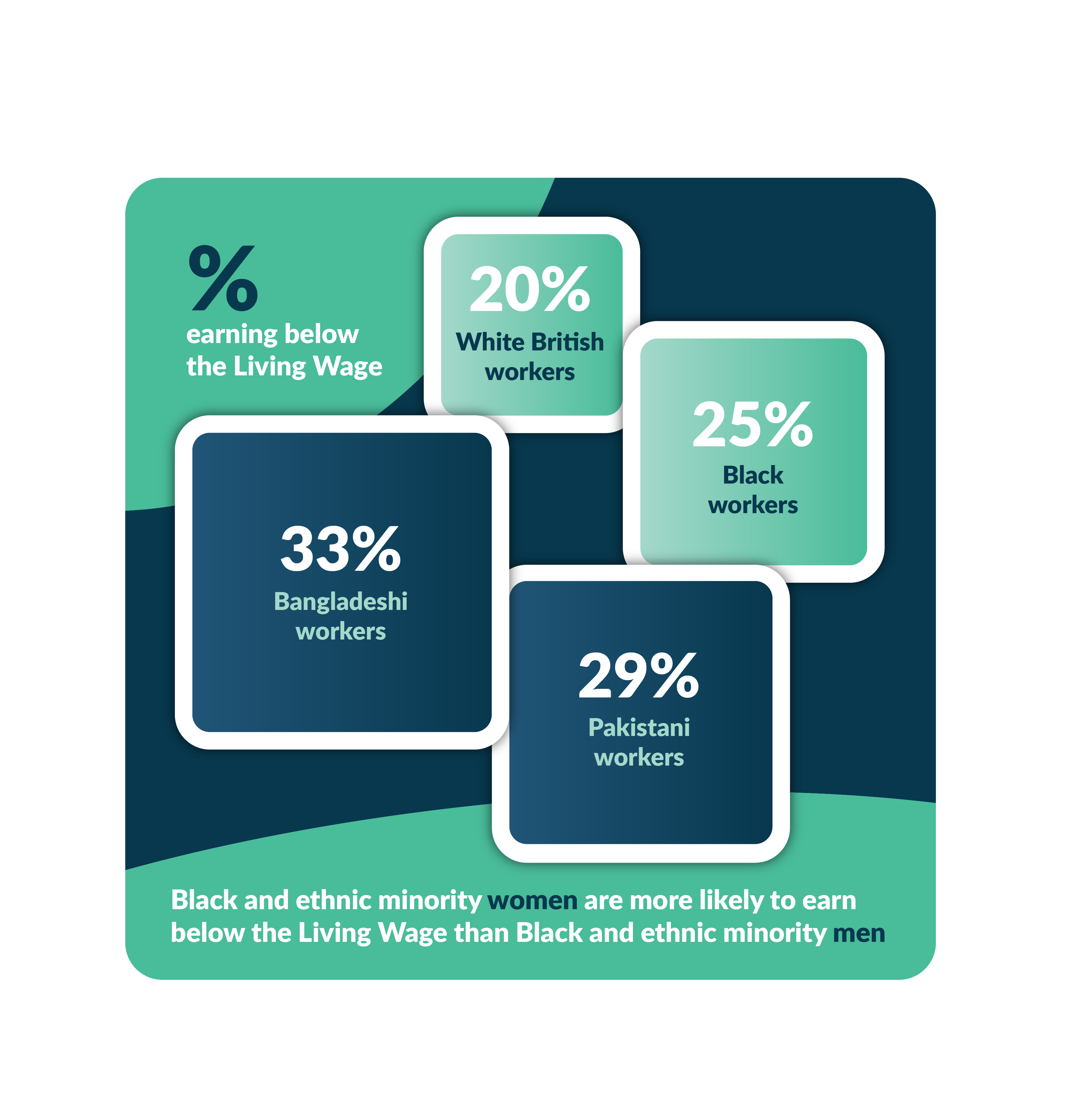

Reporting the ethnicity pay gap is still not mandatory, despite calls for change. In the UK, NGO ShareAction has lobbied FTSE companies to begin voluntarily disclosing this data, but at present, less than one in five FTSE 100 companies do so. The NGO launched a toolkit for this purpose in June, claiming that Black and ethnic minority workers are more likely to earn below the real living wage and face greater job insecurity than their white peers.

However, companies across the globe are still failing to close the gender pay gap. According to research from Equileap, just 28 companies worldwide have achieved this feat, amounting to less than 1%. Some 78% of the companies surveyed did not publish information on pay differences at all.

Reporting the ethnicity pay gap is still not mandatory, despite calls for change. In the UK, NGO ShareAction has lobbied FTSE companies to begin voluntarily disclosing this data, but at present, less than one in five FTSE 100 companies do so. The NGO launched a toolkit for this purpose in June, claiming that Black and ethnic minority workers are more likely to earn below the real living wage and face greater job insecurity than their white peers.

PERCENTAGE OF WORKERS IN THE UK EARNING BELOW THE LIVING WAGE

Black and ethnic minority women are more likely to earn below the living wage than Black and ethnic minority men

Source: ShareAction, Ethnicity Pay Gap Reporting

20%

White

workers

workers

25%

Black

workers

workers

29%

Pakistani

workers

workers

33%

Bangladeshi

workers

workers

While voting on diversity issues at AGMs may be increasing – companies in the US voted on 51 resolutions focused on racial equality last year, more than double the level of previous years – asset managers are not yet putting their money where their mouths are and changing capital allocations based on EDI issues.

Jacqueline Taiwo, founder of Black Women in Asset Management, called on the industry to invest with a racial equity lens, but had little to no response. Similarly, Onuekwusi told ESG Clarity in March: “I don’t think racial equity is explicitly thought about in portfolios, but within an ESG portfolio it should be.”

It’s a similar story when it comes to investing in LGBT issues. ESG Clarity found just one asset manager in the top 10 firms of the Responsible Ratings Index, Schroders, engages its investee holdings specifically on LGBT issues.

“Our engagement seeks to ensure companies create an inclusive culture regardless of an employee’s personal characteristics, including their sexual orientation;

this is through the belief that having an inclusive culture is what allows us to realise the benefits of diverse teams,” Katie Frame, active ownership manager at Schroders, says.

Jacqueline Taiwo, founder of Black Women in Asset Management, called on the industry to invest with a racial equity lens, but had little to no response. Similarly, Onuekwusi told ESG Clarity in March: “I don’t think racial equity is explicitly thought about in portfolios, but within an ESG portfolio it should be.”

It’s a similar story when it comes to investing in LGBT issues. ESG Clarity found just one asset manager in the top 10 firms of the Responsible Ratings Index, Schroders, engages its investee holdings specifically on LGBT issues.

“Our engagement seeks to ensure companies create an inclusive culture regardless of an employee’s personal characteristics, including their sexual orientation;

this is through the belief that having an inclusive culture is what allows us to realise the benefits of diverse teams,” Katie Frame, active ownership manager at Schroders, says.

What's next?

Working collectively as an industry seems to be the name of the game if progress is going to be seen, so fund selectors should keep an eye on what initiatives their asset managers are signed up to.

“The collaboration I’m seeing across the industry is genuinely really exciting,” says Mitesh Sheth, in the video above.

Onuekwusi agrees: “For real change to happen, there also needs to be a recognition that company cultures are not perfect, which can be really hard for businesses to accept,” he says.

“We all have a joint responsibility for the financial industry to improve, so we must work together collaboratively, along with our clients, regulators and the government, to create a transparent and level playing field for all.”

“The collaboration I’m seeing across the industry is genuinely really exciting,” says Mitesh Sheth, in the video above.

Onuekwusi agrees: “For real change to happen, there also needs to be a recognition that company cultures are not perfect, which can be really hard for businesses to accept,” he says.

“We all have a joint responsibility for the financial industry to improve, so we must work together collaboratively, along with our clients, regulators and the government, to create a transparent and level playing field for all.”

REGULATION

A busy

year of ESG regulation

year of ESG regulation

Parts of the finance industry that

have previously escaped scrutiny are being brought into the regulatory fold. Rating provider authorisation is welcomed but other legislation is criticised as weak and lacking

have previously escaped scrutiny are being brought into the regulatory fold. Rating provider authorisation is welcomed but other legislation is criticised as weak and lacking

Over the past year, the UK and Europe have seen an encouraging increase in regulatory frameworks designed to cover parts of the financial industry that have previously escaped ESG-related regulatory scrutiny.

For example, in June the EU published a new proposal to govern ESG ratings providers, requiring them to gain authorisation to provide ratings in the region.

This came hot on the heels of the UK’s proposal to bring ESG ratings providers under the Financial Conduct Authority’s (FCA) remit. This Code of Conduct, which is set to be finalised in Q4, proposes a six-point approach to regulate an industry that has faced criticism over inconsistencies and conflicts of interest.

An FCA spokesperson said: “We have delivered key regulatory initiatives in line with the priorities set out in our ESG strategy. This includes publishing proposals aimed at clamping down on greenwashing, the formation of a group to develop a voluntary Code of Conduct for ESG data and ratings providers, active monitoring of ESG-related business by firms and our review of climate disclosures by listed companies.”

For example, in June the EU published a new proposal to govern ESG ratings providers, requiring them to gain authorisation to provide ratings in the region.

This came hot on the heels of the UK’s proposal to bring ESG ratings providers under the Financial Conduct Authority’s (FCA) remit. This Code of Conduct, which is set to be finalised in Q4, proposes a six-point approach to regulate an industry that has faced criticism over inconsistencies and conflicts of interest.

An FCA spokesperson said: “We have delivered key regulatory initiatives in line with the priorities set out in our ESG strategy. This includes publishing proposals aimed at clamping down on greenwashing, the formation of a group to develop a voluntary Code of Conduct for ESG data and ratings providers, active monitoring of ESG-related business by firms and our review of climate disclosures by listed companies.”

Watch our regulation explainer video below

Video Player is loading.

Loaded: 0%

0:00

Current Time 0:00

/

Duration 0:00

Remaining Time -0:00

1x

- Chapters

- descriptions off, selected

This is a modal window.

Beginning of dialog window. Escape will cancel and close the window.

End of dialog window.

Nature protection

Another area gaining the attention of regulators is biodiversity. In September, the UK will see the launch of the Taskforce for Nature-related Disclosures – a voluntary market-led initiative that is working on a framework to help companies identify, assess, manage and disclose nature-related risks and opportunities.

Nitika Agarwal, WWF’s head of finance policy, says: “The inclusion of nature in climate transition plans is a very positive step: it has the potential to ensure that the financial sector and the economy doesn’t inadvertently exacerbate the nature crisis in trying to transition to a low-carbon economy.”

Similarly, in June, the UK’s House of Lords agreed to include nature in the Financial Services and Markets Bill, while the European Parliament passed the Nature Restoration Law in July. The latter makes some of the biodiversity targets agreed at COP15 legally binding, including restoring 20% of the EU’s land and sea by 2030 and 90% of degraded ecosystems by 2050. However, the bill’s text has been criticised for being ‘significantly weakened’.

Nitika Agarwal, WWF’s head of finance policy, says: “The inclusion of nature in climate transition plans is a very positive step: it has the potential to ensure that the financial sector and the economy doesn’t inadvertently exacerbate the nature crisis in trying to transition to a low-carbon economy.”

Similarly, in June, the UK’s House of Lords agreed to include nature in the Financial Services and Markets Bill, while the European Parliament passed the Nature Restoration Law in July. The latter makes some of the biodiversity targets agreed at COP15 legally binding, including restoring 20% of the EU’s land and sea by 2030 and 90% of degraded ecosystems by 2050. However, the bill’s text has been criticised for being ‘significantly weakened’.

EU ESG REGULATION IN 2023

Hover over dates to see regulation

Source: Schroders, EU Commission, ESAs, ESMA 608499, MA Financial

Consultations

Responses

Final decisions

10 Jan

20 Feb

3 Apr

5 Apr

12 Apr

14 Apr

Jun

Jun

31 Jul

Sep

3 Oct

Q4

What is

SDR? Click

to read

SDR? Click

to read

A busy summer for regulation

June was also marked by the rollout of the International Sustainability

Standards Board’s (ISSB) S1 and S2 sustainability reporting standards – widely

seen as a ‘landmark’ development with the potential to create a truly level playing field, although details and discrepancies are still being worked out in the

Standards’ consultation.

The framework aims to standardise disclosure around climate-related financial risks and opportunities. While reporting remains up to an individual country’s discretion, leading nations including Australia, Hong Kong, New Zealand, Singapore and the UK have already indicated plans to adopt these standards.

Also in June, the EU adopted a new due diligence regulation, the Corporate Sustainability Due Diligence Directive, which aims to foster responsible corporate behaviour that considers human rights and environmental risks. However, while some have called it a game changer, others believe it is a ‘light touch’ proposal.

Standards Board’s (ISSB) S1 and S2 sustainability reporting standards – widely

seen as a ‘landmark’ development with the potential to create a truly level playing field, although details and discrepancies are still being worked out in the

Standards’ consultation.

The framework aims to standardise disclosure around climate-related financial risks and opportunities. While reporting remains up to an individual country’s discretion, leading nations including Australia, Hong Kong, New Zealand, Singapore and the UK have already indicated plans to adopt these standards.

Also in June, the EU adopted a new due diligence regulation, the Corporate Sustainability Due Diligence Directive, which aims to foster responsible corporate behaviour that considers human rights and environmental risks. However, while some have called it a game changer, others believe it is a ‘light touch’ proposal.

Delays and criticisms

Amid an increase in regulatory proposals, many existing and proposed legislations have been criticised for a lack of clarity. Following the launch of the EU’s ESG ratings standards, for example, Victoria Hickman, counsel, financial regulation at Linklaters, pointed out several “unanswered questions” in the proposals, while some have criticised the tight timeline for providers to become authorised.

Another regulation that garnered criticism for ‘flip-flopping’ was the Sustainable Finance Disclosure Regulation (SFDR), which went into effect on 10 March 2021.

The European Commission (EC) has provided conflicting guidance on Article 8 and 9 definitions. This caused some 40% of Article 9 funds to be downgraded to Article 8 last year, only to face a potential reversal of this decision.

As frustration mounts, the EC is considering scrapping the ‘dark green’ Article 9 label altogether. A review of the consultation is set to kick off in September.

In February, French financial regulator the Autorité des Marchés Financiers (AMF) said the way SFDR is being used can be misinterpreted by savers to mean Article 8 or 9 funds are guaranteed to contribute to a more sustainable European economy.

The AMF has therefore made several recommendations to be introduced into European law in order to prevent ambiguity and meet saver expectations, including that Article 9 funds should exclude investments in fossil fuel activities that are not aligned with the European taxonomy.

The FCA’s final policy statement on its Sustainability Disclosure Requirements (SDR) has also been delayed for a second time, and is now expected in Q4. The SDR aims to stamp out greenwashing and includes proposals on sustainable fund labelling, fund disclosures for consumers and intermediaries.

Another regulation that garnered criticism for ‘flip-flopping’ was the Sustainable Finance Disclosure Regulation (SFDR), which went into effect on 10 March 2021.

The European Commission (EC) has provided conflicting guidance on Article 8 and 9 definitions. This caused some 40% of Article 9 funds to be downgraded to Article 8 last year, only to face a potential reversal of this decision.

As frustration mounts, the EC is considering scrapping the ‘dark green’ Article 9 label altogether. A review of the consultation is set to kick off in September.

In February, French financial regulator the Autorité des Marchés Financiers (AMF) said the way SFDR is being used can be misinterpreted by savers to mean Article 8 or 9 funds are guaranteed to contribute to a more sustainable European economy.

The AMF has therefore made several recommendations to be introduced into European law in order to prevent ambiguity and meet saver expectations, including that Article 9 funds should exclude investments in fossil fuel activities that are not aligned with the European taxonomy.

The FCA’s final policy statement on its Sustainability Disclosure Requirements (SDR) has also been delayed for a second time, and is now expected in Q4. The SDR aims to stamp out greenwashing and includes proposals on sustainable fund labelling, fund disclosures for consumers and intermediaries.

Stuart Forbes,

co-founder, Rize ETF

co-founder, Rize ETF

What is

SFDR? Click

to read

SFDR? Click

to read

What’s coming up?

With a growing number of ESG regulations in the pipeline, regulators may struggle to keep up. The UK’s green taxonomy, which the FCA was planning to put into law by the end of last year, has been heavily postponed, with the final implementation decision not expected until late 2023.

The taxonomy is an important piece of legislation that outlines a system to determine how sustainable a particular activity is and sets key climate, social, green or sustainable targets.

This will make for a busy end of the year for the UK regulators, while EU institutions also face additional reporting requirements under the Taxonomy Regulation in January 2024. As pressure ramps up, it will be crucial for all market players to keep a close eye on the ever-changing regulatory landscape, to ensure they are compliant with the right regulation at the right time.

The taxonomy is an important piece of legislation that outlines a system to determine how sustainable a particular activity is and sets key climate, social, green or sustainable targets.

This will make for a busy end of the year for the UK regulators, while EU institutions also face additional reporting requirements under the Taxonomy Regulation in January 2024. As pressure ramps up, it will be crucial for all market players to keep a close eye on the ever-changing regulatory landscape, to ensure they are compliant with the right regulation at the right time.