Unpacking the biggest developments in ESG and sustainable investing Click to read editor Natasha Turner’s introduction

ESG evolution explained

Home

Regulation

Equality, diversity, inclusion

Decarbonisation

Biodiversity

Engagement

Editor’s letter

Keeping pace with sustainable investing

Welcome to the very first edition of the ESG Clarity Intelligence e-zine. ESG Clarity Intelligence was set up in 2021 to complement our main publication and act as an educational hub and resource for fund selectors who were beginning to look at ESG, moving into sustainable investment careers or just starting out in the industry.

The sustainable investing industry is so fast-moving, and creates so many new acronyms and frameworks, that this has become a vital resource. This has led to the publication of this magazine, where we have chosen five of the biggest topics in the sustainable investment landscape right now to explain and explore. Read about what decarbonisation means in the context of investment, find out how the industry plans to progress on diversity and inclusion, watch our explainer video on biodiversity, flick through timelines and charts laying out the mass of upcoming regulation and reflect on a year of engagement efforts. As always, let us know what you think by emailing natasha.turner@markallengroup.com

editor’s letter

‘The sustainable investing

Natasha Turner, global editor, ESG Clarity

industry is so fast-moving

and creates so many new

acronyms, that ESG Clarity

Intelligence has become

a vital resource’

Contributor Anna Fedorova Global editor Natasha Turner Editor-in- chief, MA Financial Natalie Kenway

Head of production Caroline Howlett Deputy head of production Dan Parker Chief sub-editor Sarah Duree

The team

A busy year of ESG regulation

Parts of the finance industry that have previously escaped scrutiny are being brought into the regulatory fold. Rating provider authorisation is welcomed but other legislation is criticised as weak and lacking clarity

Over the past year, the UK and Europe have seen an encouraging increase in regulatory frameworks designed to cover parts of the financial industry that have previously escaped ESG-related regulatory scrutiny. For example, in June the EU published a new proposal to govern ESG ratings providers, requiring them to gain authorisation to provide ratings in the region. This came hot on the heels of the UK’s proposal to bring ESG ratings providers under the Financial Conduct Authority’s (FCA) remit. This Code of Conduct, which is set to be finalised in Q4, proposes a six-point approach to regulate an industry that has faced criticism over inconsistencies and conflicts of interest. An FCA spokesperson said: “We have delivered key regulatory initiatives in line with the priorities set out in our ESG strategy. This includes publishing proposals aimed at clamping down on greenwashing, the formation of a group to develop a voluntary Code of Conduct for ESG data and ratings providers, active monitoring of ESG-related business by firms and our review of climate disclosures by listed companies.”

REGULATION

Another area gaining the attention of regulators is biodiversity. In September, the UK will see the launch of the Taskforce for Nature-related Disclosures – a voluntary market-led initiative that is working on a framework to help companies identify, assess, manage and disclose nature-related risks and opportunities. Nitika Agarwal, WWF’s head of finance policy, says: “The inclusion of nature in climate transition plans is a very positive step: it has the potential to ensure that the financial sector and the economy doesn’t inadvertently exacerbate the nature crisis in trying to transition to a low-carbon economy.” Similarly, in June, the UK’s House of Lords agreed to include nature in the Financial Services and Markets Bill, while the European Parliament passed the Nature Restoration Law in July. The latter makes some of the biodiversity targets agreed at COP15 legally binding, including restoring 20% of the EU’s land and sea by 2030 and 90% of degraded ecosystems by 2050. However, the bill’s text has been criticised for being ‘significantly weakened’.

June was also marked by the rollout of the International Sustainability Standards Board’s (ISSB) S1 and S2 sustainability reporting standards – widely seen as a ‘landmark’ development with the potential to create a truly level playing field, although details and discrepancies are still being worked out in the Standards’ consultation. The framework aims to standardise disclosure around climate-related financial risks and opportunities. While reporting remains up to an individual country’s discretion, leading nations including Australia, Hong Kong, New Zealand, Singapore and the UK have already indicated plans to adopt these standards. Also in June, the EU adopted a new due diligence regulation, the Corporate Sustainability Due Diligence Directive, which aims to foster responsible corporate behaviour that considers human rights and environmental risks. However, while some have called it a game changer, others believe it is a ‘light touch’ proposal.

Watch our regulation explainer video below

Nature protection

A busy summer for regulation

Amid an increase in regulatory proposals, many existing and proposed legislations have been criticised for a lack of clarity. Following the launch of the EU’s ESG ratings standards, for example, Victoria Hickman, counsel, financial regulation at Linklaters, pointed out several “unanswered questions” in the proposals, while some have criticised the tight timeline for providers to become authorised. Another regulation that garnered criticism for ‘flip-flopping’ was the Sustainable Finance Disclosure Regulation (SFDR), which went into effect on 10 March 2021. The European Commission (EC) has provided conflicting guidance on Article 8 and 9 definitions. This caused some 40% of Article 9 funds to be downgraded to Article 8 last year, only to face a potential reversal of this decision. As frustration mounts, the EC is considering scrapping the ‘dark green’ Article 9 label altogether. A review of the consultation is set to kick off in September. In February, French financial regulator the Autorité des Marchés Financiers (AMF) said the way SFDR is being used can be misinterpreted by savers to mean Article 8 or 9 funds are guaranteed to contribute to a more sustainable European economy. The AMF has therefore made several recommendations to be introduced into European law in order to prevent ambiguity and meet saver expectations, including that Article 9 funds should exclude investments in fossil fuel activities that are not aligned with the European taxonomy. The FCA’s final policy statement on its Sustainability Disclosure Requirements (SDR) has also been delayed for a second time, and is now expected in Q4. The SDR aims to stamp out greenwashing and includes proposals on sustainable fund labelling, fund disclosures for consumers and intermediaries.

Delays and criticisms

With a growing number of ESG regulations in the pipeline, regulators may struggle to keep up. The UK’s green taxonomy, which the FCA was planning to put into law by the end of last year, has been heavily postponed, with the final implementation decision not expected until late 2023. The taxonomy is an important piece of legislation that outlines a system to determine how sustainable a particular activity is and sets key climate, social, green or sustainable targets. This will make for a busy end of the year for the UK regulators, while EU institutions also face additional reporting requirements under the Taxonomy Regulation in January 2024. As pressure ramps up, it will be crucial for all market players to keep a close eye on the ever-changing regulatory landscape, to ensure they are compliant with the right regulation at the right time.

What’s coming up?

01

EU ESG regulation in 2023

Hover over dates to see regulation

Source: Schroders, EU Commission, ESAs, ESMA 608499, MA Financial

Consultations

Responses

Final decisions

Deadline consultation on ESA call for evidence on greenwashing

Deadline consultation on ESMA guidelines on sustainability fund names

ESMA guidelines on Mifid II suitability test published

Taxonomy 4: consultation on the four remaining environmental objectives (ended 3 May)

ESA consultation on the review of SFDR RTS for PAI and financial product disclosures (ended 4 July)

European Commission published new Q&A on SFDR

Legislative proposal on ESG ratings and data providers

Taxonomy 4: adoption of delegated acts (application expected in Jan ’24)

Final guidelines for the use of ESG-related terms in fund names

European Commission consults on SFDR review expected progress report on greenwashing (ESAs)

Entry into force of updated ESMA guidelines on Mifid II suitability test

10 Jan

20 Feb

3 Apr

5 Apr

12 Apr

14 Apr

Jun

Q4

Sep

3 Oct

What is SDR? Click to read

What is SDR?

The FCA has announced new sustainable fund labels as part of its broader anti-greenwashing rule. These are ‘sustainable focus’ funds that invest in sustainable assets, ‘sustainable improver’ funds that invest in assets looking to improve their sustainability over time, and ‘sustainable impact’ funds that invest in solutions. Notably, ESG-integrated products won’t meet the criteria for sustainable focus funds.

Proposed sustainable investment label descriptions and objectives

Category name

No sustainable label

Sustainable focus

Sustainable improvers

Sustainable impact

Description

Products that do not meet the criteria for a sustainable label

Products with an objective to maintain a high standard of sustainability in the profile of assets by investing to (i) meet a credible standard of environmental and/or social sustainability; or (ii) align with a specified environmental and/or social sustainability theme

Products with an objective to deliver measurable improvements in the sustainability profile of assets over time. These products are invested in assets that, while not currently environmentally or socially sustainable, are selected for their potential to become more environmentally and/or socially sustainable over time, including in response to the stewardship influence of the firm

Products with an explicit objective to achieve a positive, measurable contribution to sustainable outcomes. These are invested in assets that provide solutions to environmental or social problems, often in underserved markets or to address observed market failures

Consumer-facing description

Invests mainly in assets that are sustainable for people and/or planet

Invests in assets that may not be sustainable now, with an aim to improve their sustainability for people and/or planet over time

Invests in solutions to problems affecting people or the planet to achieve real- world impact

Source: FCA

What is SFDR? Click to read

Stuart Forbes, co-founder, Rize ETF

European Commission adopts European Sustainability Reporting Standards

31 Jul

Stop, collaborate and listen

Although asset managers are starting to incorporate diversity and inclusion within their own organisations, the industry needs to work collectively with the businesses they invest in to effect real change

Equality, diversity and inclusion (EDI) are the hallmarks of a healthy environment, be it in the workspace or in the broader community. Multiple studies over the years have shown that a diverse workforce makes quicker and better decisions, and produces more revenue for the business. According to a recent PwC survey, 85% of financial services CEOs polled saw benefits to their business performance from promoting diversity and inclusion, while a 2019 study by McKinsey & Co revealed that top-quartile businesses for racial and ethnic inclusion were 36% more profitable than those in the fourth quartile. Yet while there has been some improvement, particularly when it comes to women’s representation on boards, progress has stalled over the past year amid a challenging economic climate.

is disappointing’

EQUALITY, DIVERSITY, INCLUSION

Unfortunately, progress is slow. Almost half (47%) of Europe’s asset and wealth managers are yet to achieve boards made up of 40% women, despite this being the target required by the European Women on Boards Directive, according to the latest EY European Financial Services Boardroom Monitor. Racial discrimination also remains rife in the financial services sector. Research from financial services network Reboot found that 68% of ethnic minorities experienced discrimination in the workplace during the previous year, while 82% faced unwelcome comments on their backgrounds. Justin Onuekwusi, co-founder of #TalkAboutBlack, says: “A lot of the momentum around EDI has dissipated, which is disappointing. There are a lot of initiatives trying to unkink the hosepipe and get people career ready, such as CV workshops and mentoring, but the support for them is not what it was three years ago.”

Much more progress can be seen in attempts to improve EDI at the companies firms invest in. According to last year’s MSCI’s Women on Boards Progress Report, the number of women on boards globally has increased by 1.9% to 24.5% in 2022. The industry has played its part in this improvement with initiatives such as the 30% Club, which is dedicated to raising awareness of the lack of women in top management positions. However, companies across the globe are still failing to close the gender pay gap. According to research from Equileap, just 28 companies worldwide have achieved this feat, amounting to less than 1%. Some 78% of the companies surveyed did not publish information on pay differences at all. Reporting the ethnicity pay gap is still not mandatory, despite calls for change. In the UK, NGO ShareAction has lobbied FTSE companies to begin voluntarily disclosing this data, but at present, less than one in five FTSE 100 companies do so. The NGO launched a toolkit for this purpose in June, claiming that Black and ethnic minority workers are more likely to earn below the real living wage and face greater job insecurity than their white peers.

While voting on diversity issues at AGMs may be increasing – companies in the US voted on 51 resolutions focused on racial equality last year, more than double the level of previous years – asset managers are not yet putting their money where their mouths are and changing capital allocations based on EDI issues. Jacqueline Taiwo, founder of Black Women in Asset Management, called on the industry to invest with a racial equity lens, but had little to no response. Similarly, Onuekwusi told ESG Clarity in March: “I don’t think racial equity is explicitly thought about in portfolios, but within an ESG portfolio it should be.” It’s a similar story when it comes to investing in LGBT issues. ESG Clarity found just one asset manager in the top 10 firms of the Responsible Ratings Index, Schroders, engages its investee holdings specifically on LGBT issues. “Our engagement seeks to ensure companies create an inclusive culture regardless of an employee’s personal characteristics, including their sexual orientation; this is through the belief that having an inclusive culture is what allows us to realise the benefits of diverse teams,” Katie Frame, active ownership manager at Schroders, says.

How asset managers are looking at EDI internally

Within their own organisations, asset managers are starting to think about their policies and cultures, with media initiatives such as City Hive’s ACT Standard and Framework, which establishes an industry agreement on how to improve EDI internally, and MA Financial’s own Campaign for Better Governance, which encourages the industry to hold a mirror up to its own culture, leading the way.

Working collectively as an industry seems to be the name of the game if progress is going to be seen, so fund selectors should keep an eye on what initiatives their asset managers are signed up to. “The collaboration I’m seeing across the industry is genuinely really exciting,” says Mitesh Sheth, in the video above. Onuekwusi agrees: “For real change to happen, there also needs to be a recognition that company cultures are not perfect, which can be really hard for businesses to accept,” he says. “We all have a joint responsibility for the financial industry to improve, so we must work together collaboratively, along with our clients, regulators and the government, to create a transparent and level playing field for all.”

Watch our explainer video on EDI below

How asset managers are looking at EDI in their investments

What's next?

Justin Onuekwusi, co-founder, #TalkAboutBlack

dissipated, which

around EDI has

‘A lot of the momentum

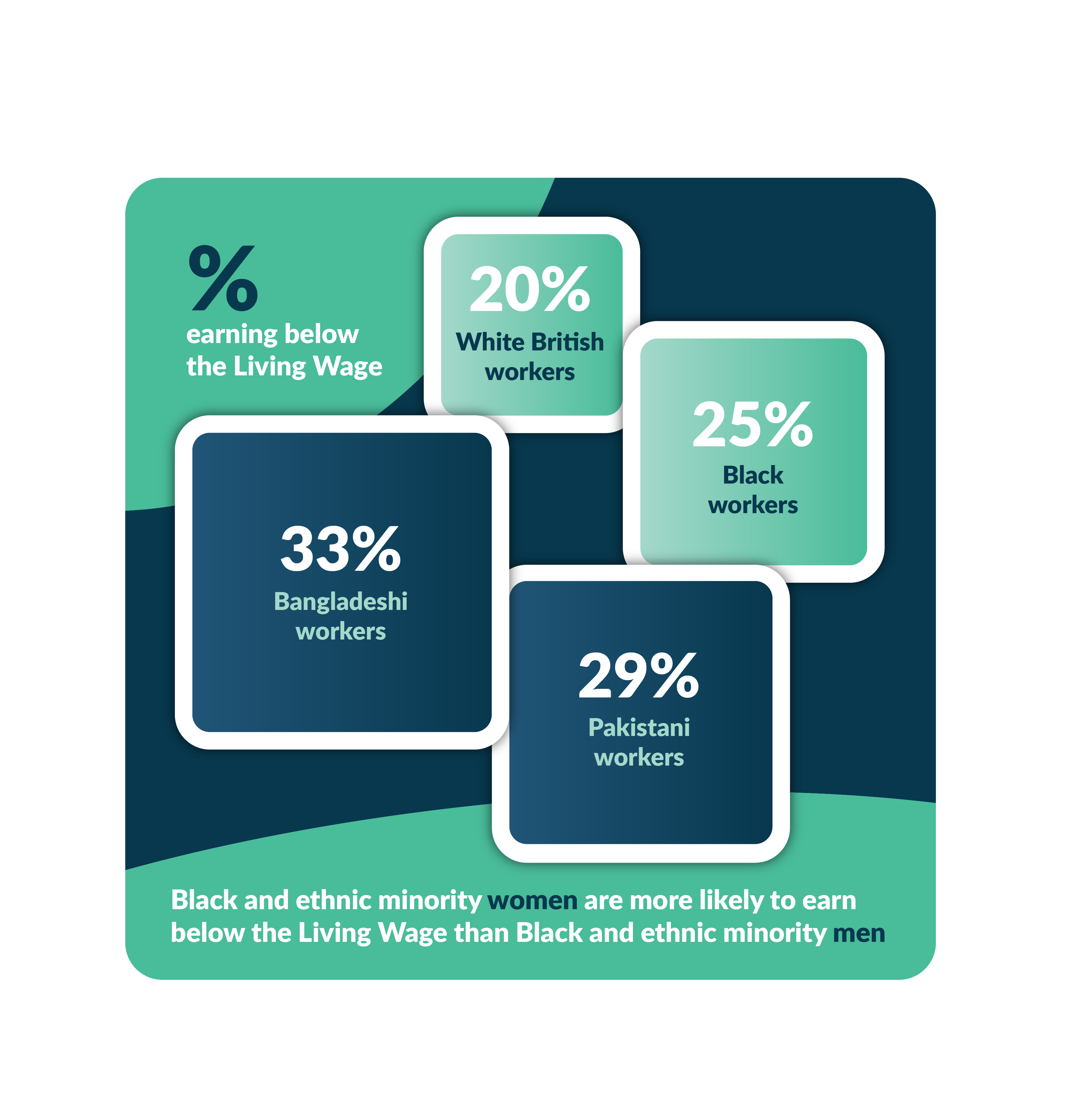

Percentage of workers in the UK earning below the living wage

Black and ethnic minority women are more likely to earn below the living wage than Black and ethnic minority men

White workers

20%

25%

29%

33%

Black workers

Pakistani workers

Bangladeshi workers

Source: ShareAction, Ethnicity Pay Gap Reporting

City Hive's ACT framework

Gap between pledges and progress

For the world to achieve carbon neutrality, asset managers have a huge role to play, working hand in hand with governments on policy, investing in climate change solutions and decarbonising their portfolios

As the Northern Hemisphere faces another unprecedented heatwave, the importance of climate change mitigation has never been more apparent. Decarbonisation – the process of reducing greenhouse gas emissions – is arguably the most important aspect of this process. Specific targets for this were first introduced at a meeting in Paris in 2015 called COP21, where the leaders of 195 nations signed an agreement to limit global warming to a maximum of 2C above pre-industrial levels, and preferably 1.5C. This is called the Paris Agreement. To achieve this ambitious target, the world must reach carbon neutrality, bringing CO2 emissions to net zero. Net zero is the balance between the greenhouse gases produced by human activity and the amount removed from the atmosphere, with the aim to have zero impact on the climate. This is possible to achieve through a two-pronged approach that removes existing carbon dioxide from the atmosphere, while also reducing new emissions. After signing the Paris Agreement, 140 countries across the globe have set net-zero targets, and private finance has a major role to play in reaching these goals.

‘The government and the

DECARBONISATION

ESG Clarity’s Net Zero Database, which looks under the bonnet of 83 asset managers’ net-zero commitments, reveals that many industry players are making commitments to decarbonise their portfolios. They can do so in a number of ways, including absolute emissions reduction, emissions intensity reduction, temperature targets and net-zero alignment for assets or emissions. The methodology for this research uses data from the Net Zero Asset Managers’ initiative (NZAM), launched in 2020 with the aim to “galvanise the asset management industry to commit to a goal of net-zero emissions”. NZAM now counts 315 firms with a total of $59trn (£46trn) in assets under management as signatories, including Aviva Investors, BlackRock and Fidelity International.

Other private sector initiatives this year include an updated version of Climate Action 100+’s Net Zero Company Benchmark to encourage companies to work towards net-zero targets, as well as the release of net-zero standards for banks and guidance for private equity firms. However, despite numerous pledges from asset managers and their investee companies, by April this year just 5% of FTSE 100 companies had published net-zero plans that are credible and detailed in terms of implementation. And in May, research by Redington revealed only 17% of asset managers have a decarbonisation strategy in place, despite 59% making a net-zero commitment at a firm level. Similarly, Net Zero Tracker reports that while the number of companies across the globe with net-zero targets has almost doubled in the past two and a half years, now standing at 909 of the world’s 2,000 largest businesses, just 4% of these commitments meet the UN Race to Zero campaign’s “starting criteria”.

Meanwhile, investment managers themselves report various challenges in meeting net-zero targets. These include a lack of consistency across data providers, which hinders the ability to calculate portfolio emissions, inconsistent climate modelling and uncertain policy context, and the fact economic growth is linked to higher emissions. Asset managers interviewed by ESG Clarity highlight that net-zero targets may be riskier and more difficult to meet for emerging markets managers, while early-stage investors point to the lack of dedicated ESG standards. Some in the industry also say policy is not moving fast enough to enable private finance to decarbonise. “The government and the private sector must work hand in-hand, but at the moment the private sector’s ambition is running ahead while the government is lagging behind,” says Heather McKay, senior policy adviser at E3G. “We need to deliver on transition plans and clear guidance through the UK green taxonomy, but to mobilise investment at the scale required this must be backed up by the government ingraining net zero in its regulatory, policy and spending decisions.” In October 2022, 30 leading UK companies managing £3trn assets, including Aviva, Jupiter and Royal London, wrote to the chancellor to advocate for “a clear ‘Net Zero Investment Plan’”. They called for an investment tracker to monitor financial flows into net zero, an assessment of sector-specific investment needs and the low-carbon investment gap, and the creation of a dedicated unit to track progress.

To remain on track for the Paris Agreement goals, asset managers will need to ramp up investments in climate solutions in the coming 12 months, according to Jasna Selih, senior stewardship specialist for Climate Action 100+, at the Principles for Responsible Investment. She says: “Under the International Energy Agency’s Net Zero Emissions by 2050 scenario, renewables should exceed 60% of total electricity supply by 2030, which would require clean energy to rise to 4% of global GDP by 2030. While we’ve seen significant growth in renewable energy generation over recent months, additional investment in clean energy is required for the world to meet the goals of the Paris Agreement. “Investment will also need to go to the deployment of new low-emissions technologies, which have yet to be scaled up but we know will be vital for the net-zero transition, and investments across the clean energy supply chain,” she adds.

Watch our decarbonisation explainer video below

The role of private finance

What are the challenges?

What’s next?

Heather McKay, senior policy adviser, E3G

private sector must work

hand in hand, but at

the moment the private

sector’s ambition is running ahead while the government is lagging’

running ahead while the government is lagging’

government is lagging’

Most asset managers now have a long-term net-zero target

Percentage of asset managers. Rollover bars to see categories

Set target of net-zero by 2040

5%

62%

8%

6%

Set target of net-zero by 2050 but dependent on parent/ company group

Set target of net-zero by 2050

Set target of net-zero by 2050 but with limited scope

Planning to set target of net-zero by 2050

Set target for ‘carbon neutrality’ by 2050

No net-zero target set or planned

Net-Zero GHG by 2050 (or sooner) ambition

75% of the world’s largest corporate GHG emitters have set a net zero by 2050 (or sooner) ambition that covers, at least, their Scope 1 and 2 GHG emissions. This is up from 69% in March 2022

Yes

Partial

No

42%

51%

28%

24%

48%

31%

Source: Share Action, Point of no Returns 2023

Source: Climate Action 100+, Key Findings October 2022

Jury’s out on funding nature

Protecting and restoring biodiversity is still in its infancy in asset management with a lack of reliable data hindering engagement, but with the natural world under threat, the finance industry must act

Planet Earth as we know it would not exist without its oceans and forests, thousands of varieties of mammals, birds, fish and millions of insect species. This varied natural world is typically referred to under the umbrella term biodiversity. Biodiversity is currently under massive threat, with 69% of mammal, bird, reptile, fish and amphibian species already lost since 1970, according to the World Wide Fund for Nature’s Living Planet Report 2022. That’s why protecting and restoring biodiversity is one of the essential areas of focus for sustainable investors. However, progress on this has been a mixed bag over the past year. In March, we reported the World Economic Forum removed biodiversity from its list of the top 10 most pressing risks over the next two years – a move criticised for its short-sightedness. Around the same time, the annual Point of No Returns report from ShareAction highlighted the lack of biodiversity voting and engagement policies at the world’s largest asset managers. It revealed that just 46% of European fund houses had a biodiversity voting policy and only half (49%) had an engagement policy, while the proportion reporting specific biodiversity commitments was just 27%.

BIODIVERSITY

Another issue, as highlighted in our ESG Clarity Annual 2021-2022, is a lack of reliable and consistent data. This was one of the roadblocks a group of investors, including Aviva and Robeco, faced during their recent collaborative engagement effort, which sought to measure the impact of waste management and nutrient pollution from livestock production of 10 animal agriculture firms. However, the past year has brought developments. January saw the launch of the Integrated Biodiversity Assessment Tool (IBAT) by NatureAlpha, which aims to help companies and investors identify the impact of their activities on nature. It has garnered support from index provider MSCI, which entered a collaboration with NatureAlpha in February to distribute the tool to its clients. Similarly, during January’s World Economic Forum conference in Davos, the WWF launched its Biodiversity Risk Filter to help companies identify and reduce these risks using 50 data sets from NASA, the IUCN, the World Bank and other sources. Finally, May saw the launch of a new tool by Clarity AI and impact data provider Gist Impact to help investors identify their exposure to companies with a negative impact on biodiversity.

The number of mutual and exchange-traded funds focused on biodiversity has grown substantially over the years, up from just three European-domiciled funds in June 2021 to 19 vehicles available by mid-2023, according to Morningstar Direct, while assets under management (AUM) in such funds tripled to nearly $1trn (£780m) in 2022, and rose again to around €1.4trn (£1.2trn) by June 2023, according to Morningstar Direct. However, in March, Daniel Wild, chief sustainability officer at Swiss private bank J Safra Sarasin, questioned whether biodiversity-focused funds were any different from other climate or ESG funds. Wild argued we simply “do not understand enough about biodiversity compared with, for instance, climate change – we are 10-15 years behind”. Similarly, there is growing scepticism around what constitutes a biodiversity ‘fund’, when loss mitigation and positive nature impact are not easily measured, and no consensus has been met. In June, the UK and France launched a biodiversity credits roadmap to support companies’ contribution to nature recovery – but biodiversity credits are encountering the same credibility issues as carbon credits, with Frédéric Hache, director and co-founder of the Green Finance Observatory, and former investment banker, pointing out they are “plagued with environmental integrity issues” with around two-thirds of projects currently failing.

years behind’

Daniel Wild, chief sustainability officer, J Safra Sarasin

This impetus to improve activity on biodiversity may come from regulatory action, with the Taskforce for Nature-related Disclosures coming into effect in September and touted as potentially ‘revolutionary’. This framework aims to provide investors with the tools to assess and disclose nature-related risks and opportunities. Another seemingly positive step in the UK is the inclusion of nature into the Financial Services and Markets Bill’s regulatory principles on net-zero emissions. However, according to Nitika Agarwal, WWF’s head of finance policy: “To truly mobilise sufficient financing to regenerate nature, companies and financial institutions should be required to develop fully integrated climate and nature-positive transition plans, and the government must use all the levers at its disposal – policy, regulation, strategic public spending – to create the right incentives to leverage private finance into protecting and restoring nature.” Some global asset managers are also making greater commitments to tackling biodiversity risks in their portfolios. Last year, Aviva Investors voted against 83 company directors with inadequate deforestation policies, while Fidelity and Federated Hermes have also been actively engaging with their investee companies on biodiversity. Sonya Likhtman, associate director – engagement EOS at Federated Hermes, says: “Voting policies and approaches to shareholder resolutions can complement engagement and be geared towards accelerating company action on issues related to biodiversity loss, such as deforestation and plastics. “We have seen an increase in these resolutions over the past few years, and they can be powerful tools for focusing boards and management teams on a company’s role in addressing biodiversity loss.”

Click for more on the TNFD initiative

Asset manager action on biodiversity

What selectors should watch out for

Watch our biodiversity explainer video below

Some restrictions on companies that operate in areas of global biodiversity importance

Engage with companies about impacts but no restrictions

Monitor impacts but don’t engage or restrict investment

Don’t consider impacts on important areas for biodiversity

change – we are 10-15 years behind’

for instance, climate

compared with,

enough about diversity

‘[We] do not understand

TNFD explained

The Taskforce on Nature-related Financial Disclosures (TNFD) is a global, voluntary, market-led initiative aiming to develop a framework to allow businesses of all sizes to identify, assess, manage and disclose nature-related dependencies, impacts, risks and opportunities. Consisting of 40 senior executives and representing institutions with more than $20.6trn (£16trn) in assets under management, the Taskforce will publish its recommendations in September 2023.

Click for all biodiversity funds available for sale in Europe

All biodiversity funds available for sale in Europe (as of 18 Jul 2023)

Is any asset justified?

The investment industry has shifted from divestment to dialogue – the challenge is to measure the results of these efforts and report on successes and failures

Engagement has been a controversial topic over the years in the world of ESG investing. This approach involves investing in a company, often an underperformer on ESG metrics, and opening a long-term dialogue to improve its practices. However, since the early days of ESG investing, stalwarts of the space argued against engagement and in favour of divestment from these so-called ‘brown’ companies, on the grounds that capital should not flow towards polluting industries like coal and gas. Over the years though, this narrative has shifted, with the benefits of engagement becoming more accepted by the wider investment community. To date, some $40.5trn has been divested from fossil fuels by 1,593 institutions worldwide (see graphic below), but the majority of these are educational, faith-based and philanthropic institutions. Many asset managers, meanwhile, are choosing the engagement approach.

‘We hope the TNFD will

ENGAGEMENT

In fact, a new trend is emerging of funds that focus specifically on engagement rather than divestment. An example is Redwheel’s UK Climate Engagement Fund, which has a portfolio of polluters, such as Shell and BP, but aims to help them reduce their carbon footprint through engagement. In the June edition of ESG Clarity’s digital magazine, Joss Murphy, junior research analyst at FundCalibre & Chelsea Financial Services, argues that this approach marks the evolution of ESG engagement, one that is just as necessary as investing in top ESG performers. Similarly, in a video interview in May, Jenn-Hui Tan, Fidelity’s global head of stewardship and sustainable investing, tells ESG Clarity that divestment represents a failure of the firm’s engagement. Another development has been the recent rise of collaborative investor engagement campaigns. For example, Newton teamed up with ShareAction in March to call for decarbonisation in the chemicals sector, while the CCLA brought together 10 UK asset managers, including Schroders, Quilter Cheviot and Sarisin & Partners, to protect the UK’s migrant seasonal workers.

However, while engagement is evolving, many more niche areas are seeing few engagement efforts, such as ethnic diversity and biodiversity protection. On the latter, the Point of No Returns 2023 report by ShareAction found that biodiversity is still not well represented in managers’ engagement policies, with the majority of efforts focused on broader climate mitigation initiatives instead. While 82% of asset managers had voting policies on climate, only 38% considered biodiversity, the report revealed.

Institutions divesting

1,593

Approximate value of institutions divesting

$40.51trn

Louisiana Salge, head of sustainability at EQ Investors, hopes that regulators can become the driving force for better engagement and reporting on nature-related risks. She says: “In March, the Taskforce on Nature-Related Financial Disclosures (TNFD) released its fourth and final draft framework consultation to help companies disclose nature-related risks and impacts. The TNFD will unveil its final recommendations in September. We hope the TNFD will establish a global framework that can be integrated into investor decision-making and price in biodiversity risk and opportunity.”

Michael Herskovich, global head of stewardship and proxy voting within BNP Paribas Asset Management’s Sustainability Centre, says: “We always favour engagement over divestment to try to improve a company’s performance or to tackle controversies, although we divest as a last resort, in instances where companies do not respond to engagement and show no signs that they will place greater emphasis on sustainability in the future.”

‘We divest as a last resort,

15.6% Educational institutions

0.3% Other

0.3% Cultural institutions

8.4% For profit corporations

3.9% NGOs

1.1% Healthcare institutions

11.7% Pension funds

11% Government

11.9% Philanthropic foundations

35.8% Faith-based organisations

Percentage of asset managers

A majority of asset managers had climate change and social engagement policies, but less than half reported an engagement policy on biodiversity

Engagement policy, formalised guidelines

Engagement policy, limited detail

No policy

The integration is delegated to portfolio managers

Dedicated thematic policy covering all portfolios

Policy with some specific portfolios and/or sectors that are exempt

Theme is exclusively an investment consideration for funds or mandates labelled ‘ESG’, ‘RI’ or similar

General RI policy that includes the theme, covering all portfolios

Michael Herskovich, global head of stewardship and proxy voting, Sustainability Centre, BNP Paribas Asset Management

Louisiana Salge, head of sustainability, EQ Investors

The evolution of engagement

Watch our engagement explainer video below

Engagement failures

In the UK, the regulatory push for investors to report on their engagement activities is already underway. Most recently, the Financial Conduct Authority (FCA) released a consultation on sustainable fund labelling, which puts engagement “front and centre in a way that the industry has never seen before”, according to Ita McMahon, partner at Castlefield. In a comment piece for ESG Clarity in May, McMahon points out that the scheme’s new ‘sustainable improvers’ category would allow fund managers to invest in any asset, as long as it has the “potential to become more environmentally and/or socially sustainable over time”. The challenge, then, is to measure the results of these engagement efforts and report on the successes and failures. While legislation can help set the precedent for responsible reporting, investors have faced challenges when reporting on more niche areas. An example is the recent collaborative effort by a group of investors, including Aviva and Robeco, to address the biodiversity impacts of the practices employed in livestock production. The coalition came across a lack of the necessary data to assess the impact of companies’ operations and supply chains on water quality, making it impossible to measure the impact of their campaign. As such, while firms are stepping up their engagement efforts, these must encompass a wide variety of ESG risks and opportunities and not only net-zero transition plans. There is a long road ahead for asset managers to ensure that engagement is truly a better choice than divestment.

in instances where

companies do not

respond to engagement

and show no signs they

will place greater

emphasis on

sustainability in the future’

establish a global

framework that can be

integrated into investor

decision-making and

price in biodiversity risk

and opportunity’

Source: Global Fossil Fuels Divestment Commitments Database